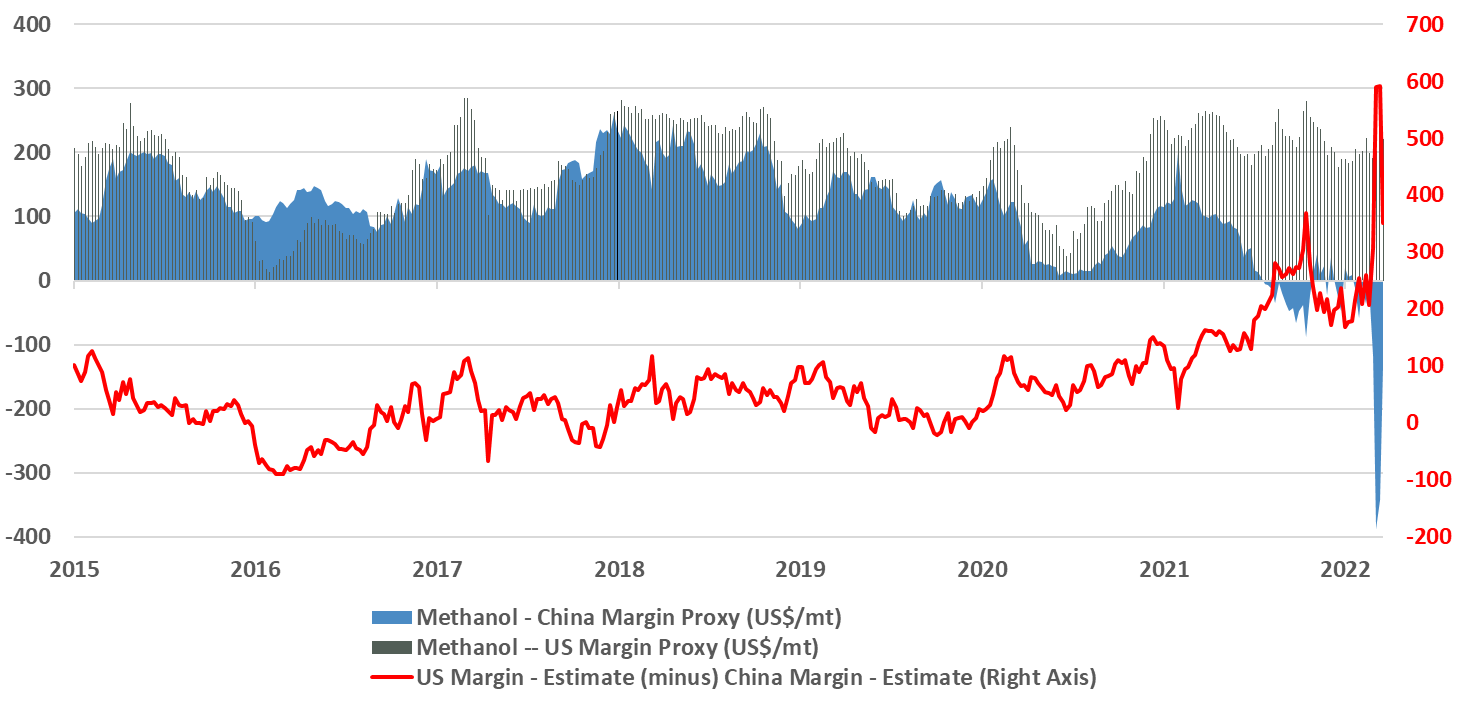

Methanol is one of a few chemicals that is directly impacted by the price of natural gas, and as the chart below shows, the pain in China (and in Europe) is extreme and it is unlikely that any facilities that require imported natural gas – or local gas with prices based on imports – are operating today. The volume and margin opportunities for those companies connected to low priced natural gas – the US, the Middle East, and other niche locations such as Trinidad, are as good as they have ever been and we are a little surprised that Methanex did not push a little harder with US pricing, given that export netbacks are likely surging. Urea and ammonia are in the same boat and prices are much higher, but the US is a net importer and international prices are directly impacting the US price.

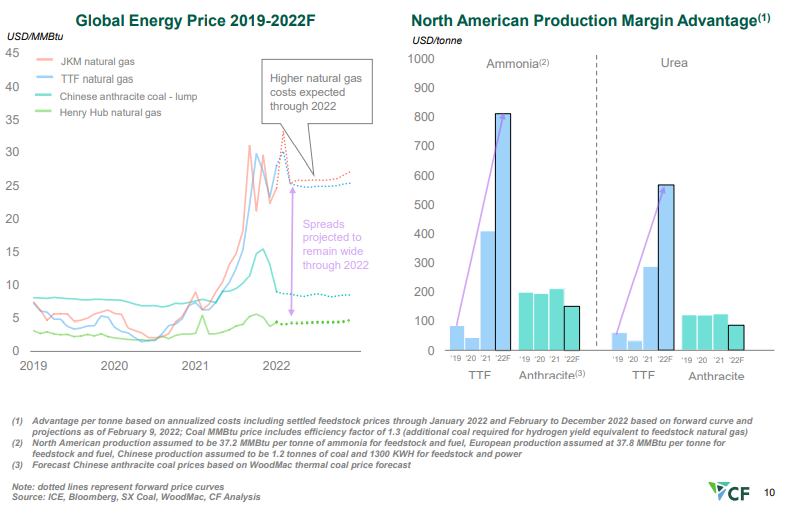

The CF slide below shows very clearly the US competitive edge when it comes to making anything that has a natural gas base, and while we tend to talk mostly about ethylene, ammonia, urea, other ammonia derivatives, and methanol are all seeing significant cost advantages. The Chinese coal-based costs are better than those in Europe and Asia based on natural gas but margins remain well below those in the US. The challenge with the coal-based chemistry in China is that it has substantial CO2 emissions, and the facilities were not designed for carbon capture. As China develops a carbon cap and trade market and as these facilities get included, costs will rise significantly.