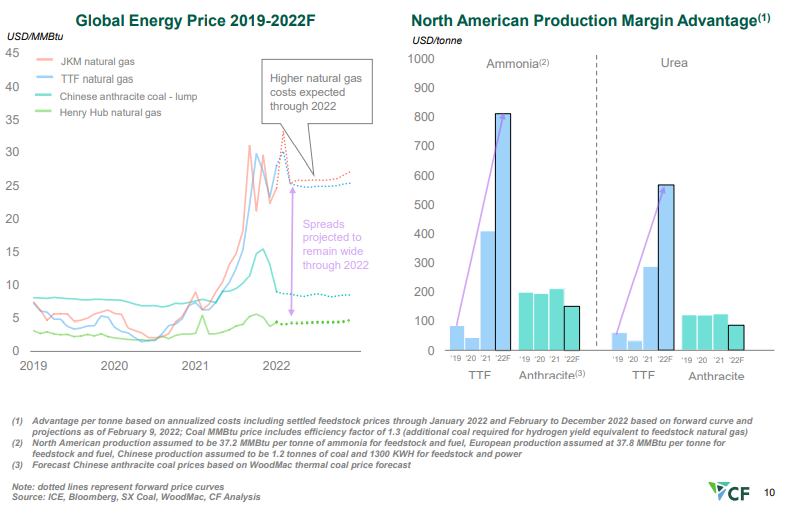

The CF slide below shows very clearly the US competitive edge when it comes to making anything that has a natural gas base, and while we tend to talk mostly about ethylene, ammonia, urea, other ammonia derivatives, and methanol are all seeing significant cost advantages. The Chinese coal-based costs are better than those in Europe and Asia based on natural gas but margins remain well below those in the US. The challenge with the coal-based chemistry in China is that it has substantial CO2 emissions, and the facilities were not designed for carbon capture. As China develops a carbon cap and trade market and as these facilities get included, costs will rise significantly.

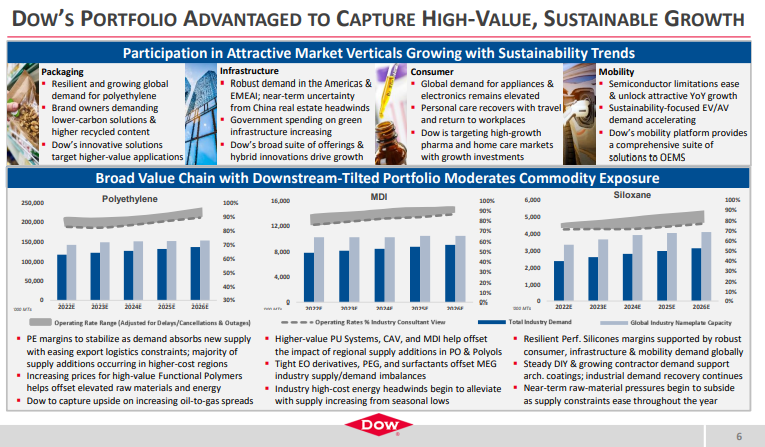

While it might be tempting (and perhaps easier) to focus on the negatives in the Dow earnings release – such as price declines in polyethylene and higher costs in Asia, we think it is much more interesting to focus on the positives. For a while now we have been suggesting that the industry is gearing up for a mega-cycle of profitability, perhaps as early as 2024 – see report – and we see nothing in the current macro environment or in Dow’s release to suggest we might be wrong. Demand growth is very robust across the industry, with consumer spending driving some quite impressive GDP growth numbers in the US in 4Q 2021, as an example. We often see companies suggest improving global operating rates in earnings calls, and while it is mostly hopeful and self-serving, the chart below, from Dow’s report may be conservative. The very high ratio of Asia costs versus US costs in the 2012 to 2014 period (second image below), because of high oil prices, effectively shutdown new naphtha based ethylene investment in Asia for several years and it is what prompted China’s move into coal-based and methanol chemicals (China has almost no ethylene capacity from methanol or coal in 2011, but close to 6 million tons by 2016). As the price of oil rises and the cost curve works against China and the rest of Asia again, the move to more coal is less attractive because of the environmental footprint – coal gasification creates a lot of CO2 emissions and elaborates CCS investment would be needed to justify further expansions, which increases the cost of ethylene production.

In an important, but inevitable, change in tone, it is worth noting that the Borouge ethylene expansion announcement includes the idea that the complex will explore the possibility of a major carbon capture facility that will take much of the CO2 from the existing complex as well as the new plant. We have stated previously that the mood has changed sufficiently such that large industrial investments without a carbon abatement plan will not get approval from stakeholders and this is a prime example of what we expect. Locations with low-cost CCS will see disproportionate investment in our view and Abu Dhabi already has CCS in place as Adnoc is selling blue ammonia already to Japan. As we noted in a recent Sunday Piece, we expect carbon abatement challenges to slow expansions in basic chemicals and, despite this announcement by Borealis, see a market shortage in 2024/25 as a consequence.

The major issue with the higher natural gas prices in Europe (and rising prices globally) is the knock-on inflationary impact it will have on products that have natural gas as a feed, rather than those buying it as a fuel. The fuel buyers will take some of the hit, but will also try to pass on some of the hit, as it is generally a small part of overall product or service costs. The focus has been on ammonia/urea production because of the knock-on effect on food-grade CO2. But other products, such as methanol, would also be impacted, although there is not much methanol capacity in Europe. Higher LNG prices in Asia could encourage more coal-based methanol production, which is precisely what the increased use of LNG was supposed to prevent – replacing a high carbon footprint route with a much lower one. In our view, it is imperative that the attendees of COP26 recognize the need for (cleaner) natural gas and LNG, and enact policies to support it. This inflationary lesson is well-timed.