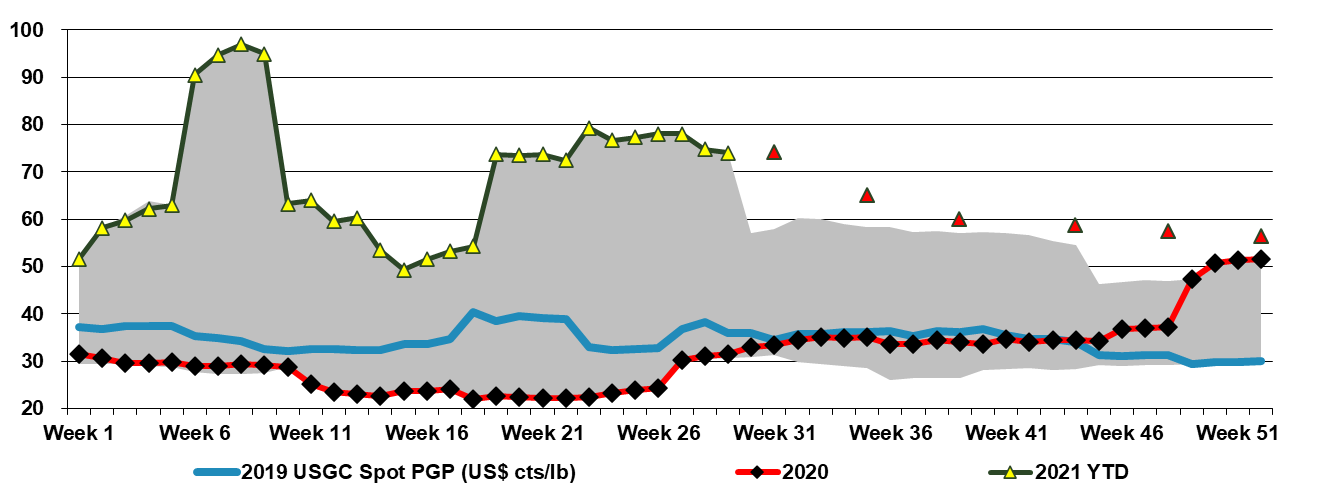

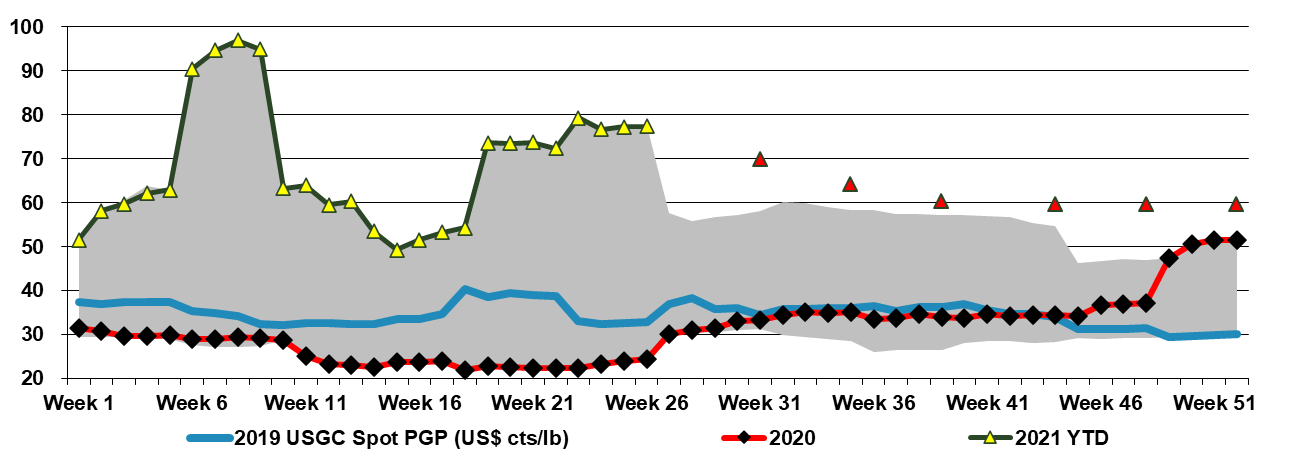

Polymer grade propylene in the US is weakening, albeit slowly, but remains very high versus history, versus ethylene and incremental costs of production. Propylene has the same volatile dynamic that ethylene has today in that if short, consumers can pay a lot more, and if long the price was a long way down to reach any cost hurdle. Just like ethylene we expect the market to show meaningful volatility in 3Q 2021 unless we get a storm effect in the US that impacts production more than demand. The futures market for propane and propylene expects propylene to fall relative to propane and barring weather events this is probably a reasonable view. See more in today's daily report.

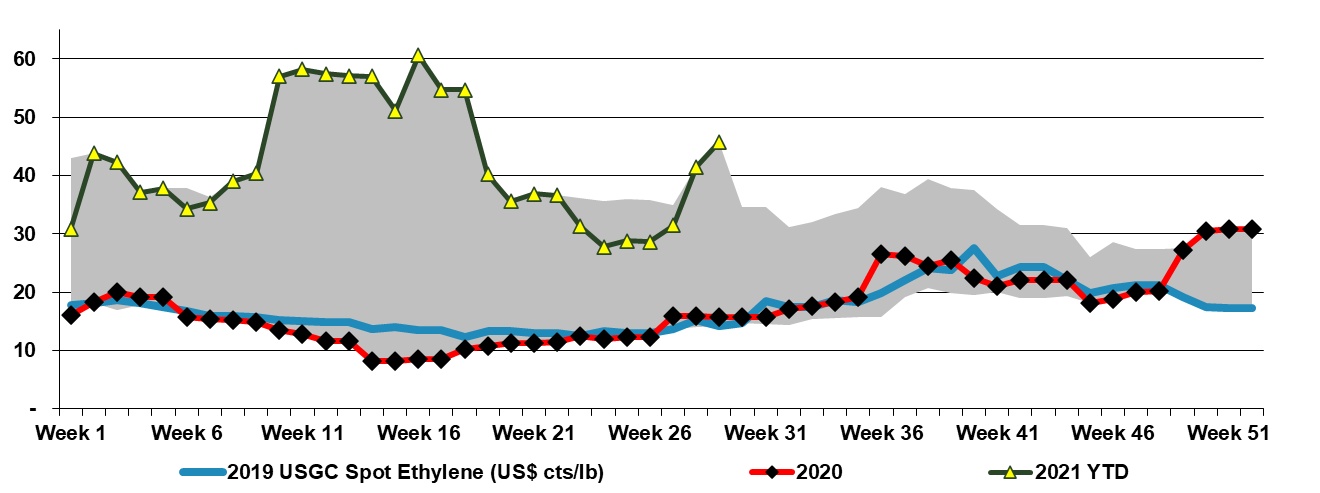

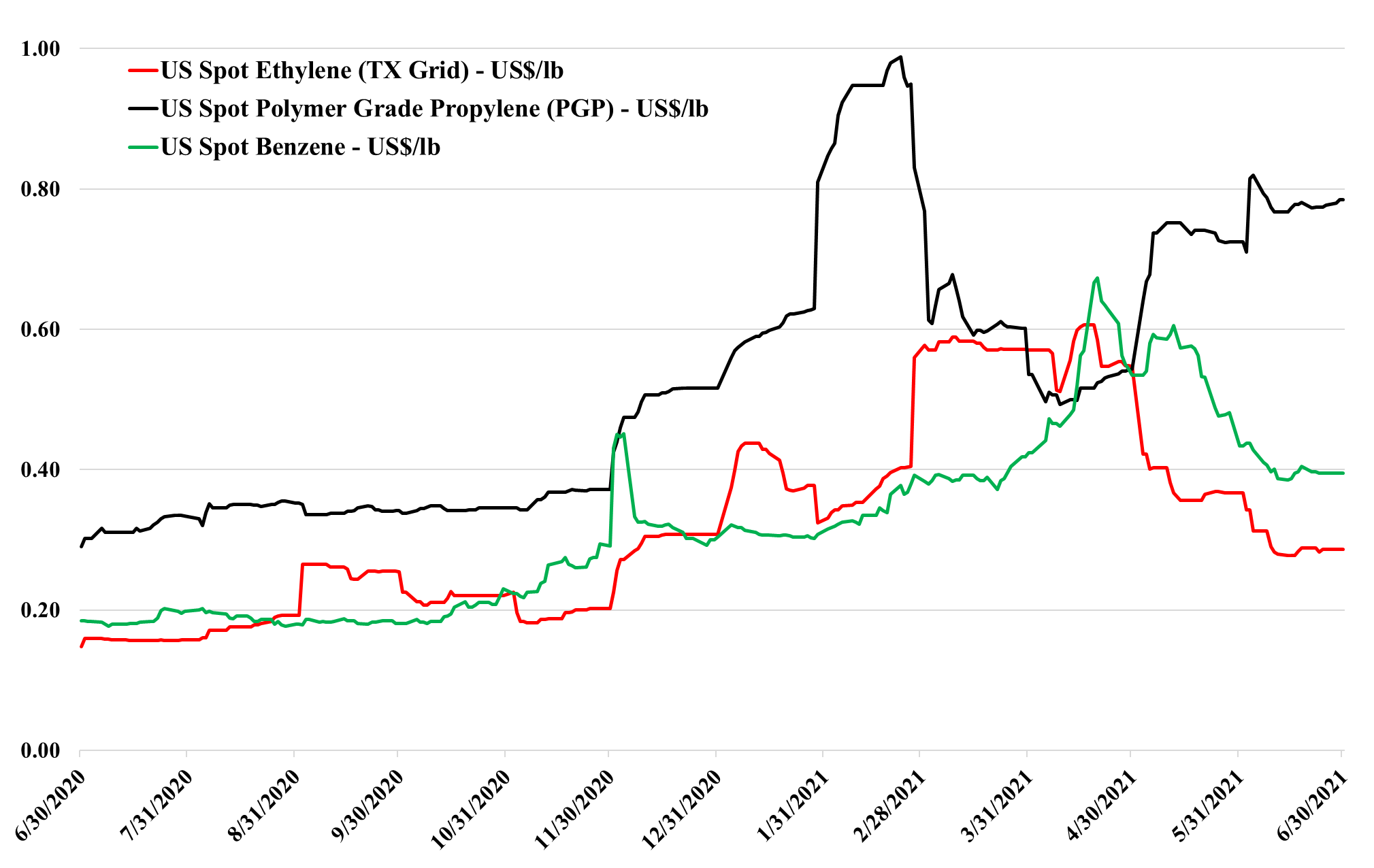

Spot prices for ethylene have surged in the US in the last week (chart below) – especially for delivery to Louisiana, where Westlake has a production outage. The price increase has completely removed the brief export arbitrage to Asia that lasted for a few weeks in late May and early June (Exhibit 5 in today's daily report). As we discussed on Sunday, ethylene is in a very wide no-mans-land in the US as it is not in sufficient surplus to drive pricing down to costs, and would likely be supported well above US costs and more by Asia costs in the current market, but if the market becomes short, buyers can pay a lot more for it as derivative prices are so high. If a PVC producer, such as Westlake, is buying, they can afford to pay significant premiums given that ethylene is less than 50% of the PVC molecule.

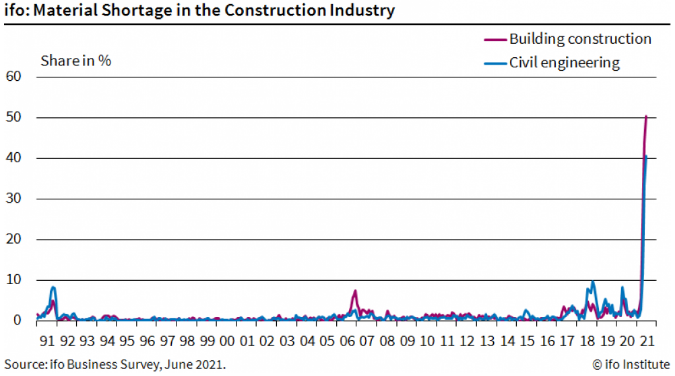

The German materials shortage chart below is certainly eye-catching. There is nothing even remotely close in 30 years of history. We see this as further confirmation that we should continue to expect high shipping rates and congested ports until surveys like this show significantly better results and it is also further supportive of inflation. While it is extremely difficult to forecast from here, we would use the pendulum or spring metaphor – the further you pull either in one direction, the further they swing or spring back. The current dislocation is so extreme that everyone in the chain is likely acting instinctively and working to find greater supply and greater supply security. At some point, both end-demand and demand to fill inventories will normalize – either back to trend or back to a higher trend, but the inventory build piece will end and we will either get a gradual retreat in the scary data – such as the spike in the chart below – or we will see an equally quick collapse, at which point pricing will likely take a hit down the chain, with basic chemicals particularly vulnerable because the world has been adding substantial new capacity over the last several years in the US and China. More investment may be needed to keep up with higher trend demand in many intermediate or end-products that consume base chemicals and this could keep pricing supported, but basic chemicals and polymers look especially vulnerable to a reversal in the supply chain build we have seen for the last 9 months. For more see today's daily report.

The US ethylene market strengthened slightly in early July, most likely because of supply disruptions as it is hard to see how domestic demand could improve from here. There is not much room to increase prices further if the export market is the balancing mechanism through July and August, as prices remain depressed in Asia and any arbitrage would close quickly if prices in the US moved any higher. Despite the rising NGL prices discussed in today's daily report and on Sunday, the US has plenty of margin left in ethylene, and prices could go lower if that is necessary to move additional volume. While we talk in the opening paragraph about increased inventories of finished goods in anticipation of the year-end holiday season and continued supply constraints, and how this is leading to a shortage of warehouse space, we suspect that everyone upstream of the finished good suppliers is also looking at adding or maintaining a larger inventory cushion than they have in recent years. We still believe that it is a tough call today as to whether you should sell surplus ethylene or store it as we head into hurricane season in the US.

We think the India styrene plan is ill-advised. The styrene market has had a brief moment in the sun over the last couple of years, but we believe that it has another leg down ahead, based on the recycling complications of polystyrene versus other packaging polymers. New capacity in China and likely weaker demand in the US and Europe should push the global market into oversupply for a prolonged period (if not permanently). This is bad news for styrene (or polystyrene) producers but very good news for the non-integrated producers of styrene derivatives targeting the durables markets – such as Kraton.

The higher ethane prices and the sharp increase in 2Q is likely offering some support for ethylene, but the more likely leveling factor of the last week or so has been the Nova outage and any lost production at Westlake, which will have a direct impact on export availability. Until ethylene spot prices in the US approach costs, which are around 10 cents per pound based on ethane feed, the more important driver of pricing will be whether or not there is a surplus and if there is what price is needed to generate export demand. The US ethylene surplus is equivalent to a couple of large plants and consequently, the market can swing from short to long depending on who is operating and is very vulnerable to weather-related closures, although these often take down ethylene derivative plants as well, creating shortages of the derivatives. Polyethylene can afford to pay more than y twice the current price of ethylene, while the ethylene export market needs a further step down from here. Consequently, the range of potential volatility in 3Q is very high – we underestimated the weather impact last year, as did everyone else and it would be a tough call today for a producer with a surplus as to whether to push it into the export market or hold on to it. See more in today's Daily Report.

The LG Chem announcement may be a hollow victory for a while, and we would use the analogy of being the “best-looking horse in a glue factory”, given the weakness in the Asia ethylene and derivative markets right now. In this case, being the biggest means you lose the most in a down-cycle (see chart below and more on today's daily report). The significant capacity adds in China have collided with lower than anticipated demand growth, and driven prices down to costs (or below in the case of polyethylene in China). However, one thing we have learned over the last few decades is that you should never underestimate China’s ability to grow its way out of oversupply, and to assume that the surplus in Asia is here for the long-term is probably wrong. However, it could last a year or so and this is very unfortunate for LG Chem as making a loss in your first year of operation is very hard to come back from when looking at the project on a DCF basis.

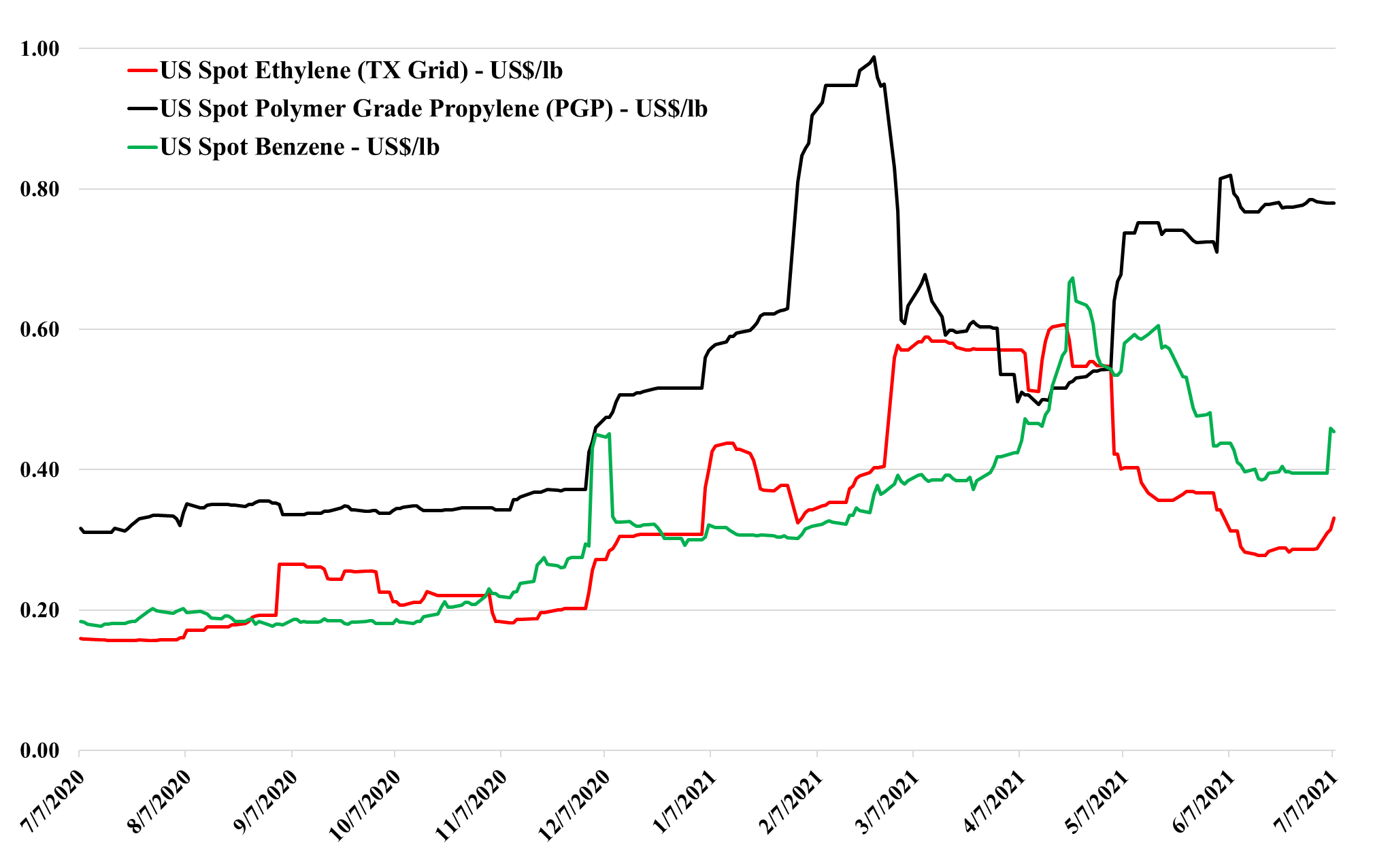

Source: Bloomberg, C-MACC Analysis, June 2021

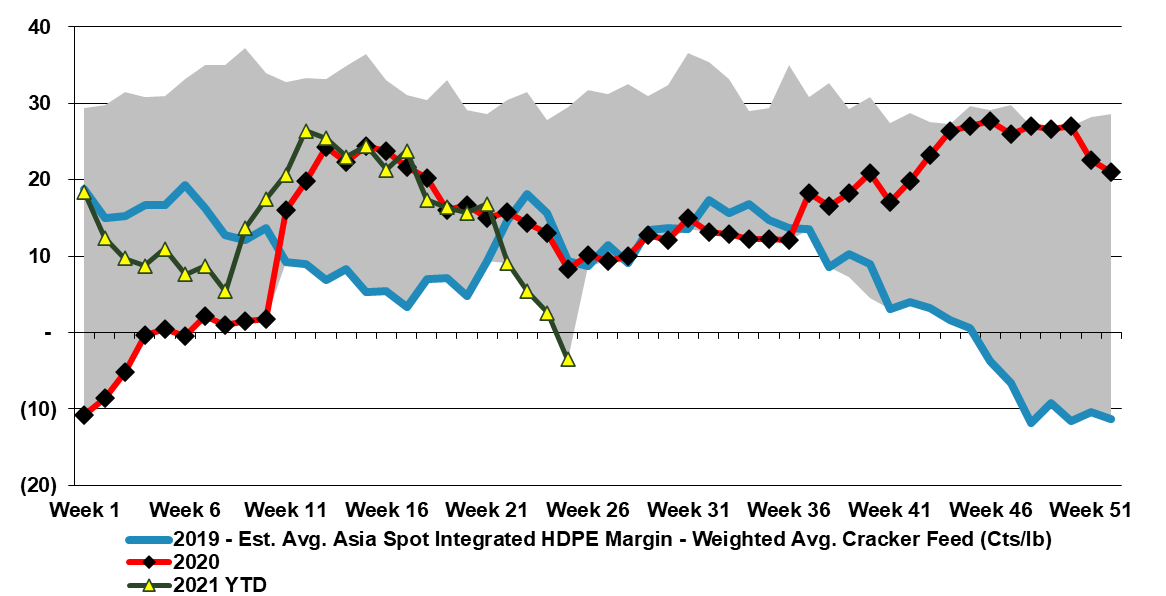

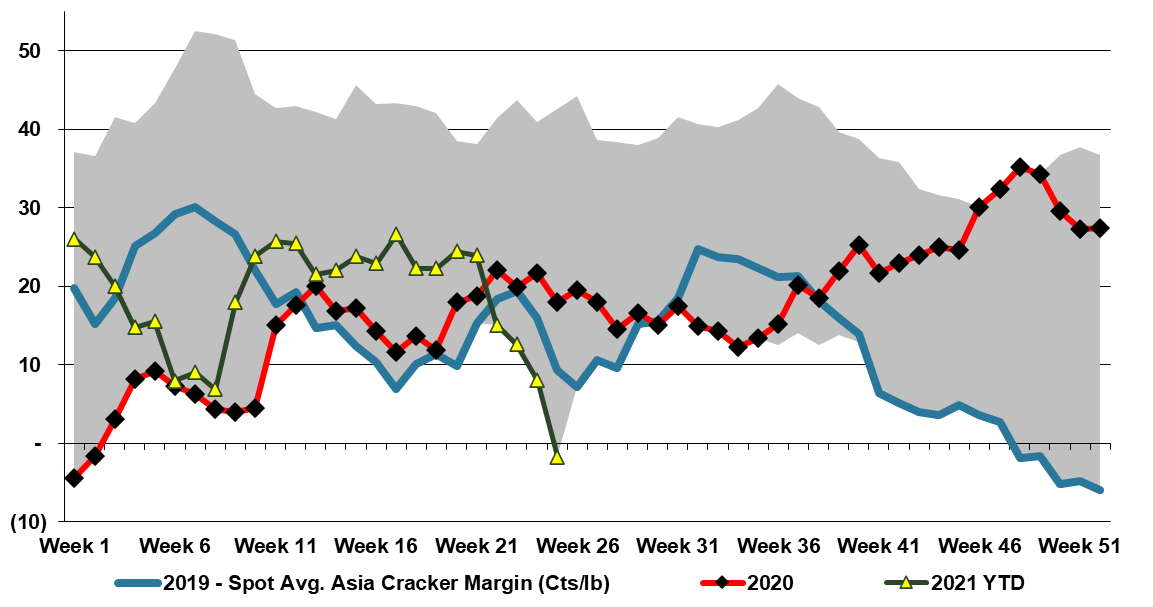

The charts below focus on ethylene and the significant decline in Asia prices, now to levels that suggest negative cash margins. While we may see some cutbacks in production, especially if ethylene from the US can be secured at prices that are even lower than we see in Asia today, most producers will run until they cannot cover variable costs, and given that some of the imbalance, in China especially, might be short term in nature, it is unlikely that we will see any drastic production decisions yet. While the capacity additions in China have been extreme, demand is subdued domestically as consumer spending has not returned to its pre-pandemic trend and the shipping and port problems are hindering export demand.

The Baystar polyethylene start-up date is consistent with the guidance that the company has been providing for a while, but it still leaves the venture with an ethylene surplus until that time and while the ethylene has been placed, according to the company, the ethylene that it has displaced will likely keep some downward pressure on US ethylene pricing until the polymer plant starts up (all things being equal). Even when the polymer plant starts, the US is expected to have a net ethylene surplus and we would expect exports to continue and prices to reflect levels to make the exports possible.

See today's daily for more on this, but while the freight rate moves are more than likely going to correct to a degree at some point, their continual escalation has multiple implications for the chemical and plastic industry as they are most impactful on cheap imports from Asia targeting low-cost furniture, appliances, toys, and household goods where the base cost of the product is low and the move from $3,000 to $10,000 per container wipes out any advantage of manufacturing offshore.