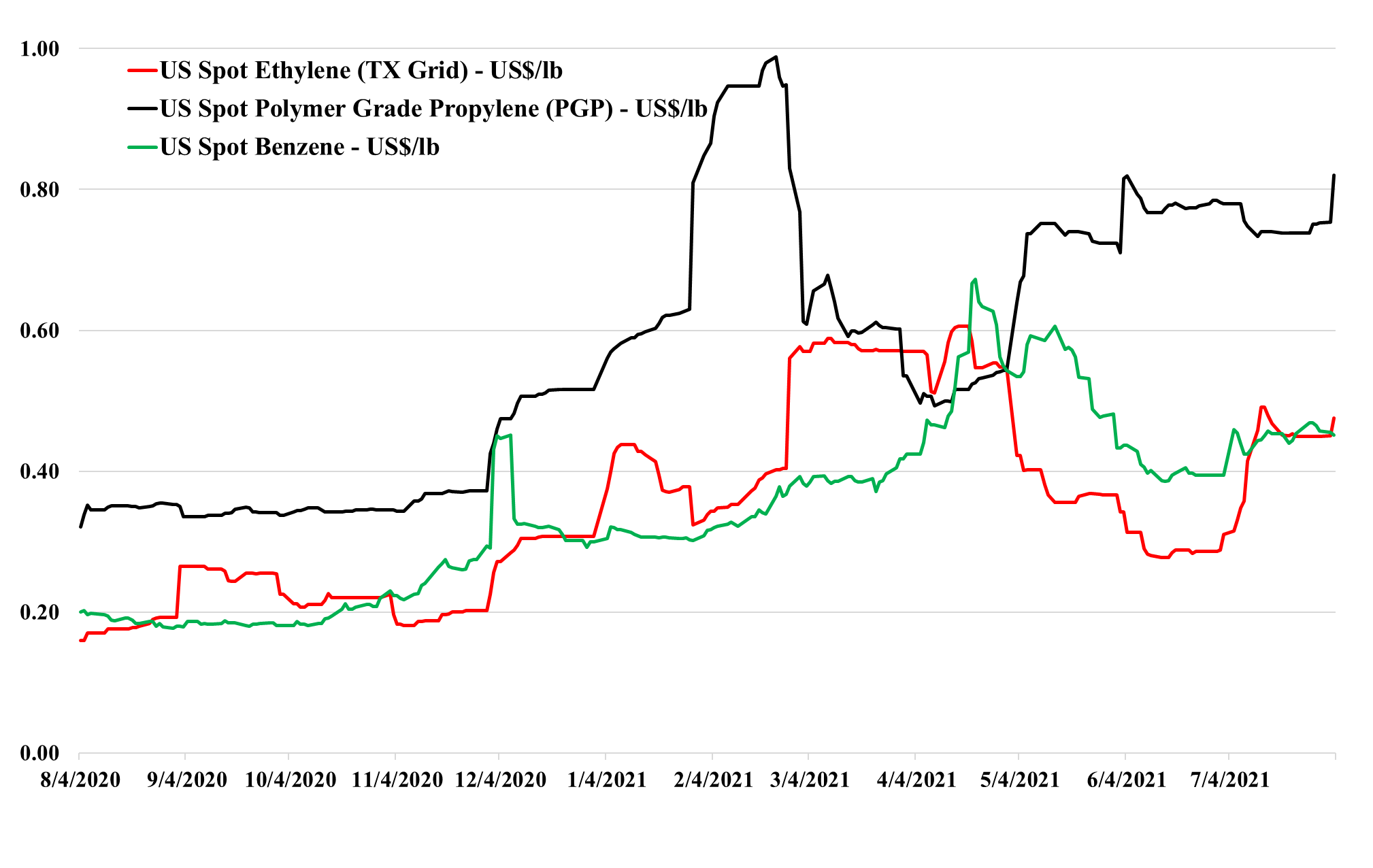

If this commodity cycle has the same drivers as prior cycles, producers like LyondellBasell and others will make comments like “stronger of longer” until prices turn, and if history is any guide, that turn will catch everyone by surprise, and even if it does not, there is no upside for any producer in predicting its end. As with all commodities, markets are tight until they are not, and markets are long until they are not. If you look at the ethylene and propylene price movements in the exhibit below you can see the speed of change that is possible and while the slope may be less severe for polymers in both directions, it can still be abrupt. The worst-case for the US industry would be a step down in demand coincident with the rising natural gas trend. There is no evidence of demand weakness today, but there will not be until it is happening. The extraordinary incremental freight rates shown in Exhibit 1 of today's daily report, make it increasingly unlikely that anyone sitting on surplus polyethylene or polypropylene in Asia can exploit the regional price difference. When demand and sentiment around supply chains turn, we would expect this spot shipping rate to collapse also – but there is no sign of that today.

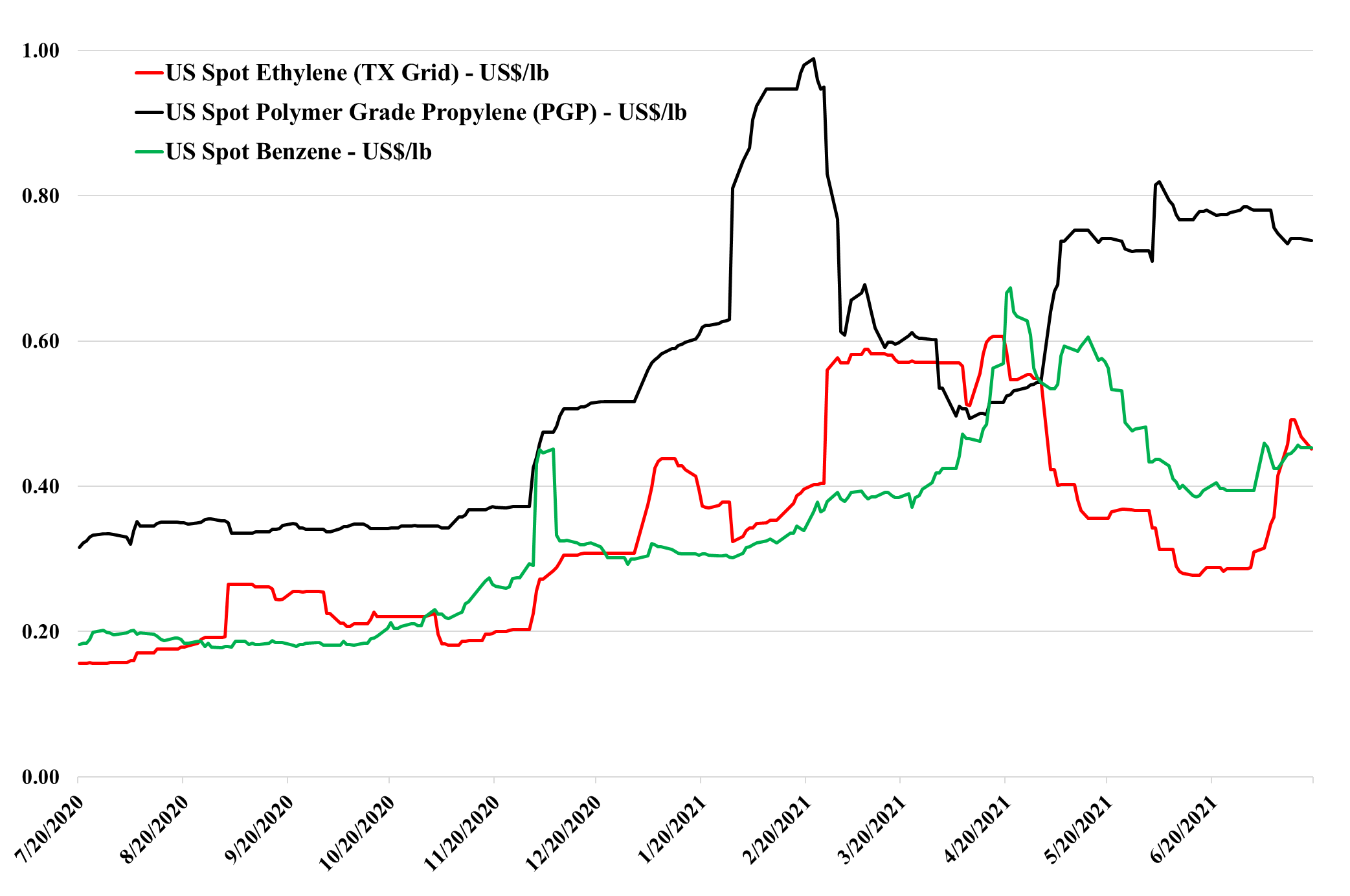

We focus on ethylene price trends today, as we discuss it’s movement and related ethane tightness in today's daily report – more operating ethylene capacity means more ethylene (depressing prices) but it also means more ethane demand, inflating its price. Margins remain robust, even with the feedstock increase and the price decline and it is important to remember that any decline in US ethylene prices would be stopped at a level that allowed increased exports, which would still be well above US costs. With the full ethylene fleet operating in the US, there is a surplus (i.e. more ethylene than there is consuming capacity) so we expect export economics to drive spot pricing under “normal” circumstances. Abnormal production outages over the last year have seen that export surplus come and go a couple of times and the price volatility the Exhibit below shows that.

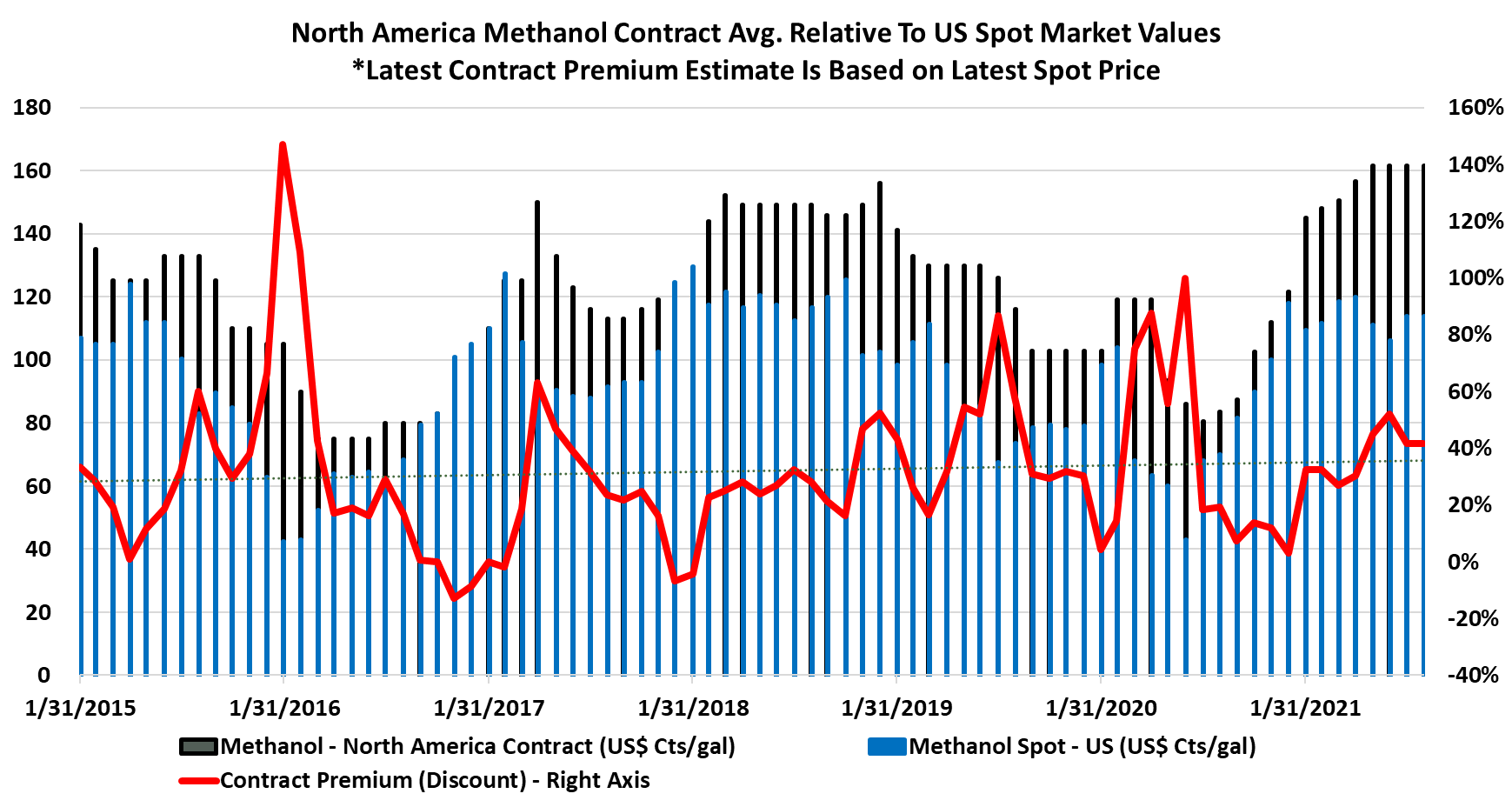

Methanol prices in the US remain very robust and quite profitable for producers, despite weakness in China. The higher natural gas price in the US (see today's daily report) provides some support for methanol pricing, but ultimately coal-based methanol in China will win out if US costs keep rising and this may curtail demand for US methanol at the margin. As with all other chemical and polymer markets today, freight costs are making it difficult to play off some of these apparent regional arbitrages and the US methanol producers would have to be somewhat reckless to upset the balance domestically and give up the margins that they have today. Domestic demand for methanol derivatives is high and the LyondellBasell accident may provide more pricing strength through the acetic acid chain. While the incident will decrease the demand for methanol, LyondellBasell should be able to manage this, and higher pricing in the acetic chain would mean that consumers would have no issue paying current prices. Higher MMA production in the US – implied in the headline below - should keep methanol demand high.

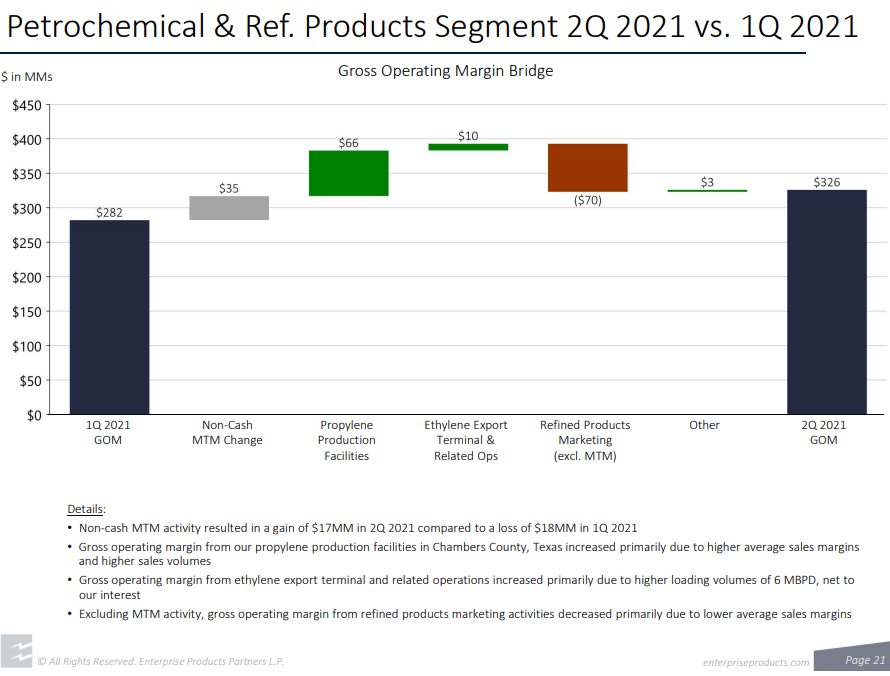

The Enterprise Products propylene numbers are impressive when you considering that its PDH facility was closed for a significant portion of the quarter, and while this likely contributed to tightness in the market, the company could have made even more money in 2Q. The results show the clear tightness in the propylene market in the US and reflect the very strong momentum in propylene derivatives, which is broad-based although we have tended to focus on polypropylene in recent work. See more in today's daily report.

ExxonMobil Chemicals has announced that its Corpus Christi JV project with SABIC is ahead of its original schedule – ExxonMobil is now targeting a start-up in 2H21, ahead of its previously targeted 1H22 expectation. It is unusual for projects in the US to be ready ahead of schedule these days, and start-up delays tend to be the norm. We also take a positive view of this development upon comparison to the Shell Pennsylvania project, which still has a vague 2022 start-up expectation though its construction began before ExxonMobil. One could argue that the remoteness of the location – well away from petrochemical infrastructure has been a constraint for Shell, but the Corpus Christi location is also a greenfield project for ExxonMobil/SABIC. This will be the largest ethylene plant built in the US, though it is likely that the recent 1.5 million ton units (Dow, ExxonMobil, CP Chem) are expandable to 2.0 million tons. Dow is already discussing such a move with a new polyethylene facility at Freeport. It will be interesting to see what impact this ExxonMobil/SABIC facility has on both the USGC ethane market and the polyethylene market – 1.3 million tons of polyethylene is a large increment and SABIC will have half of the capacity and will be a new market entrant with on-shore production. Aramco has ethylene, through Motiva’s purchase of Flint Hills, and SABIC owns half of the Cosmar styrene plant in Louisiana.

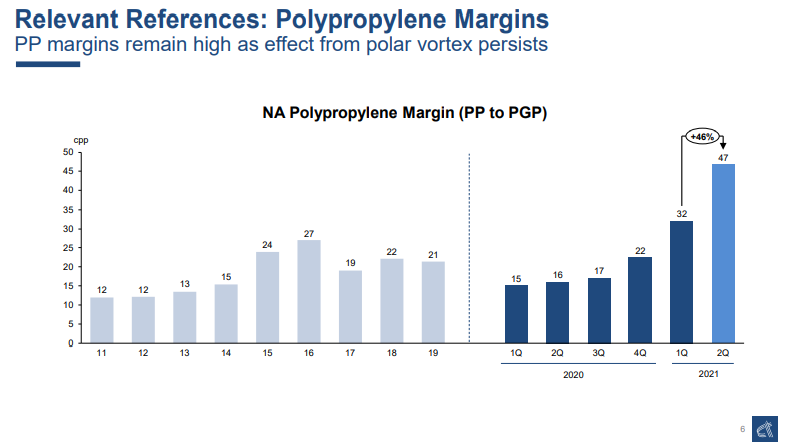

The much higher polypropylene margins in the US come despite very high propylene pricing, and the whole chain did well in the first half of the year. Demand for polypropylene has been significantly stronger than most expected year to date, although production outages have helped the market, and what we had expected to be a surplus in the US in 2021, precipitated by the Braskem start-up has turned out to be production coming online just in time and prices might have been higher still had the Braskem plant not been there. We see some of the demand as cyclical - in response to consumer durables, though there has been lower use in the auto industry because of the production cutbacks. See more in today's daily report.

The Halliburton forecast of an upcycle for oil services likely needs to be put into context, as while activity should rise in the sector with higher oil and gas prices, it is unlikely that we will see a major boom. The uncertainty in the energy market, coupled with ESG pressure and borrowing constraints means that the oil industry will likely focus on its lowest hanging fruit first and may hold off on secondary opportunities completely. The oil service guys will benefit because the more productive shale wells can require longer laterals, deeper wells, and more fracking pressure, but it will likely be quality over volume when it comes to drilling activity, in keeping with what we have seen year to date.

We note the volatility in ethylene in the chart below and point out that ethylene sits in a precarious no-mans-land in the US with pricing neither reflecting costs nor incremental value in use. The downside to generating buying interest in Asia is significant – more than 25% - but an incremental buyer in the US could pay much more than the current price – in many cases to meet export obligations, let alone for domestic sales. We would expect the volatility to continue, with a downside from better production rates and upside from more constraints – demand fluctuations are likely immaterial relative to the impact that supply moves could have. See more in today's daily report.

We talk at length about the weather risks in the US following multiple extreme weather events during the last 12 months, but we forget that other regions are equally susceptible. Not only are there many chemical facilities on the riverways impacted by the floods in Germany but a significant volume of chemical trade takes place by barge on the rivers for both gases and liquids. We do not have an industry impact assessment for this tragedy in Germany, Belgium, and the Netherlands, but on-site flooding, especially any flooding that impacts electrics, can result in extended shutdowns for repairs, as we have seen in the past in the US.

Regional PVC price movements are interesting as the World is trying to find balance. Incremental ethylene and chlorine economics in Asia pushed the local spot prices for EDC so low as to shut out US EDC exports – the net result has been more PVC production in the US and a decline in US spot prices. While it is likely that the Asia incremental pricing will improve as some sellers will be losing money and may need to cut back rates, the US will not enjoy a better export market without the acceptance of much lower netbacks, which will maintain negative pressure on domestic prices. That said, PVC is very levered to economic, construction, and housing investment in Asia and there is likely some pent-up COVID-related demand in the region – the oversupplied market may not last for long. We still see a better medium-term outlook for PVC than for other major polymers. There's more detail and coverage on today's daily report linked here.