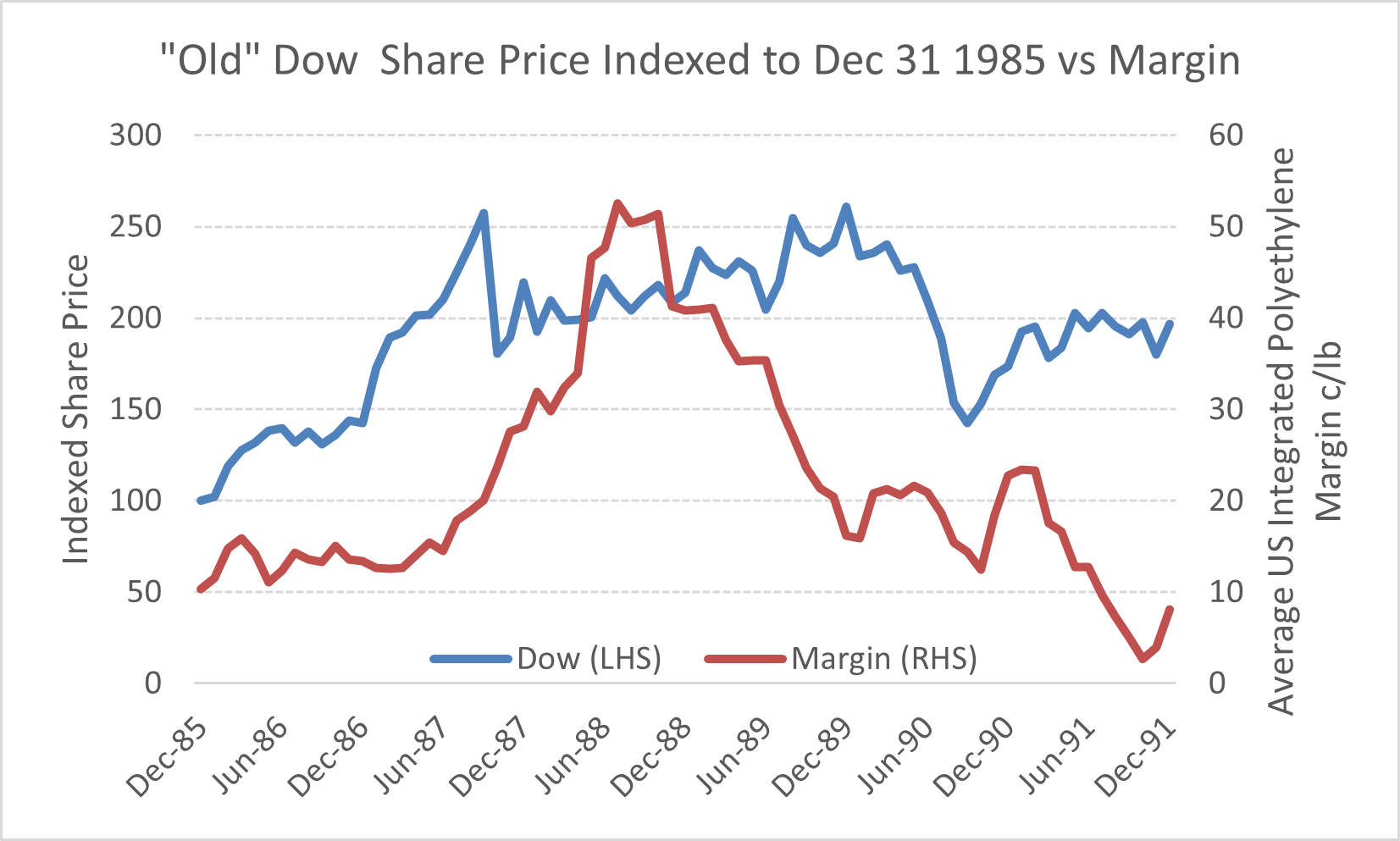

In yesterday's Sunday thematic and weekly recap report titled "Waiting For The Big One – Is A Chemical Mega-Cycle Ahead?", we referenced the global shortage of basic chemicals and polymers in the late 80's. We think this could repeat because of limited capital spending to grow basic chemical capacity due to cost and long-term demand uncertainties and this could cause a mid-decade global profit mega-cycle. Emission abatement initiatives and concerns with feedstock prices/availability will work against the justification of capacity expansions in every global region. Demand growth mitigation from plastic bans, renewables, and increased like-for-like recycling is unlikely to impact materially pre-2026/27.

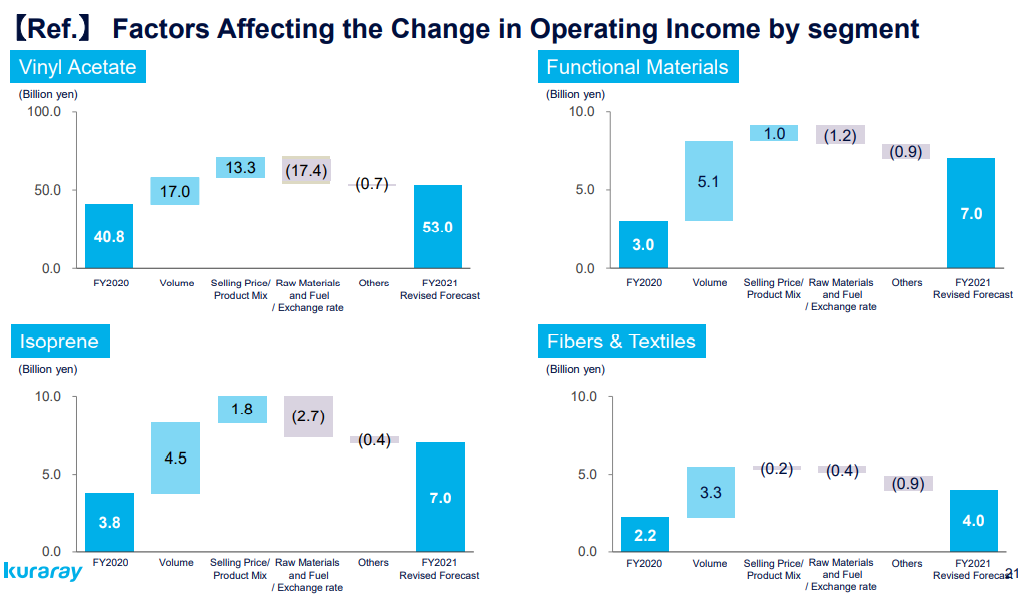

The 2Q volume driver of Kuraray’s earnings recovery was substantial, partly because end-market demand is strong and because this more mid-stream and specialty portfolio has significant operating leverage, much more than you would see from the commodity producers. We find this as a notable downstream sector trend to keep in mind. As seen below, increased selling prices are an important driver of Kuraray full-year profit growth expectations, but the volume piece is the most critical component, in our view. As discussed in our daily report today available in LINK, we continue to see volatile but elevated basic chemical prices.

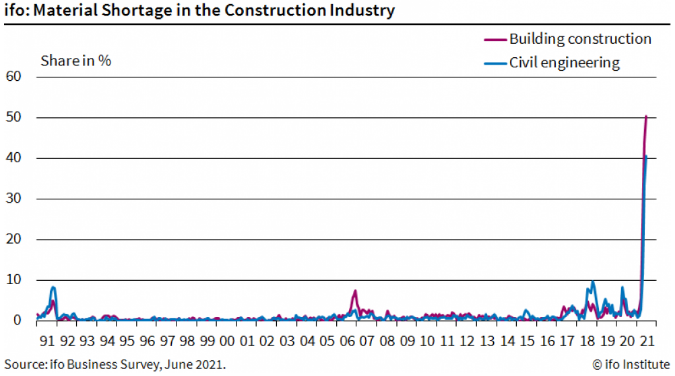

The German materials shortage chart below is certainly eye-catching. There is nothing even remotely close in 30 years of history. We see this as further confirmation that we should continue to expect high shipping rates and congested ports until surveys like this show significantly better results and it is also further supportive of inflation. While it is extremely difficult to forecast from here, we would use the pendulum or spring metaphor – the further you pull either in one direction, the further they swing or spring back. The current dislocation is so extreme that everyone in the chain is likely acting instinctively and working to find greater supply and greater supply security. At some point, both end-demand and demand to fill inventories will normalize – either back to trend or back to a higher trend, but the inventory build piece will end and we will either get a gradual retreat in the scary data – such as the spike in the chart below – or we will see an equally quick collapse, at which point pricing will likely take a hit down the chain, with basic chemicals particularly vulnerable because the world has been adding substantial new capacity over the last several years in the US and China. More investment may be needed to keep up with higher trend demand in many intermediate or end-products that consume base chemicals and this could keep pricing supported, but basic chemicals and polymers look especially vulnerable to a reversal in the supply chain build we have seen for the last 9 months. For more see today's daily report.

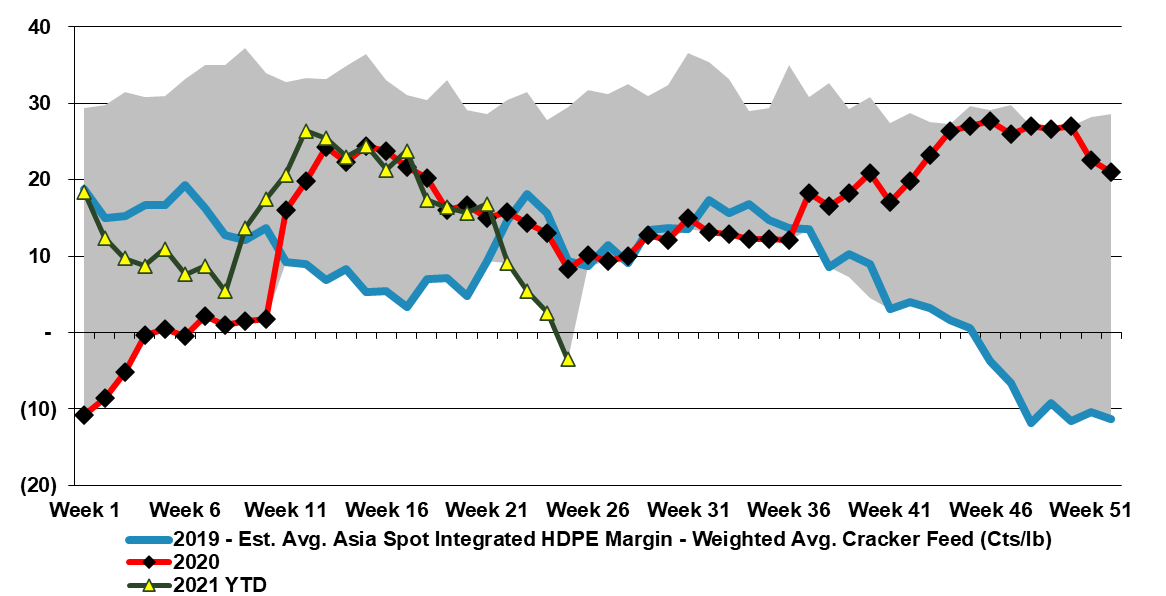

The LG Chem announcement may be a hollow victory for a while, and we would use the analogy of being the “best-looking horse in a glue factory”, given the weakness in the Asia ethylene and derivative markets right now. In this case, being the biggest means you lose the most in a down-cycle (see chart below and more on today's daily report). The significant capacity adds in China have collided with lower than anticipated demand growth, and driven prices down to costs (or below in the case of polyethylene in China). However, one thing we have learned over the last few decades is that you should never underestimate China’s ability to grow its way out of oversupply, and to assume that the surplus in Asia is here for the long-term is probably wrong. However, it could last a year or so and this is very unfortunate for LG Chem as making a loss in your first year of operation is very hard to come back from when looking at the project on a DCF basis.

Source: Bloomberg, C-MACC Analysis, June 2021