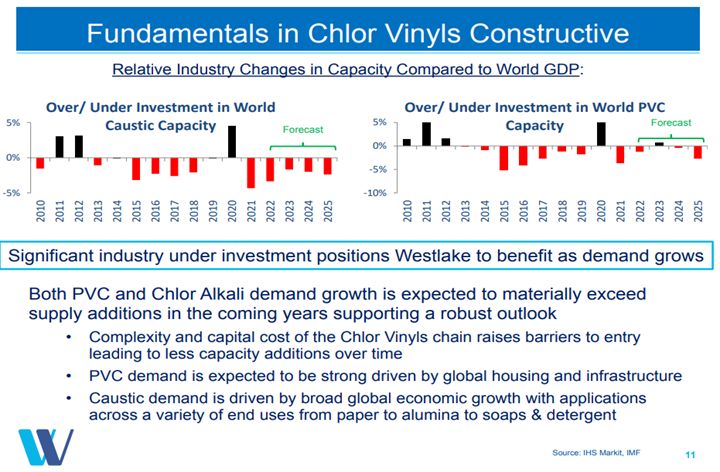

The margin weakness in PVC, as shown in Exhibit 1 from today's daily report, suggests that the market might be weakening, but higher prices would suggest that it is not. The integrated margin weakness is mostly the result of rising costs, and the US PVC market may be strong enough to allow producers to pass on these costs fully over time. We still see PVC as the least risky way to play the US polymers market as infrastructure and manufacturing investments should keep demand strong even if we see a decline in consumer durable related spending. The Westlake chart below highlights one of the primary drivers behind our mega-cycle view – no new capacity. The supply shortfalls that are implied in the chart will be mirrored in other basic chemicals in our view but PVC is likely the most acute example – creating what could be a prolonged period of strong margins for the industry.

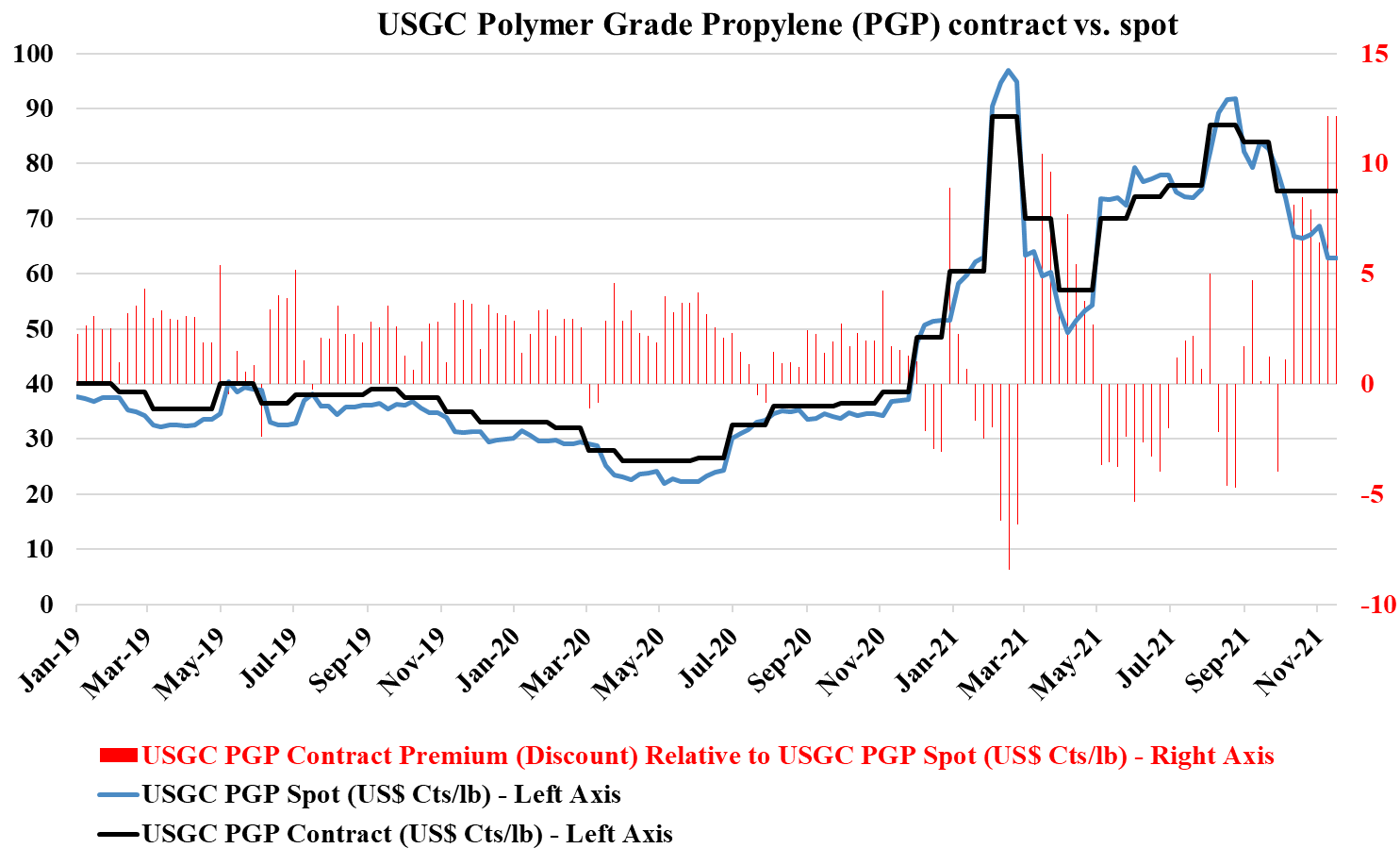

As we have been suggesting for some time, there are pockets of real strength in chemicals; identifying them is the hard part. It is not enough to have pricing strength in a market where raw material prices are volatile daily and we have seen plenty of examples of companies with very strong end demand dynamics missing earnings because of a cost squeeze. We continue to highlight the competitive strength in the US in basic chemicals because of the decoupled and relatively low natural gas price and this is likely a large piece of the Dow earnings strength – strong polyethylene demand against a backdrop of relatively stable and lower costs. While polypropylene (Braskem) remains extremely profitable in the US, it has seen more sequential weakness than polyethylene – as we show in Exhibit 1 of today's daily report. That said, both polyethylene and polypropylene margins in the US are significantly higher than was likely expected this year and certainly what has been reflected in stock valuations, even with the commodity chemicals rally. Dow is also seeing the benefit of a very strong silicones market – something that was covered in detail in Wacker’s release earlier this month.

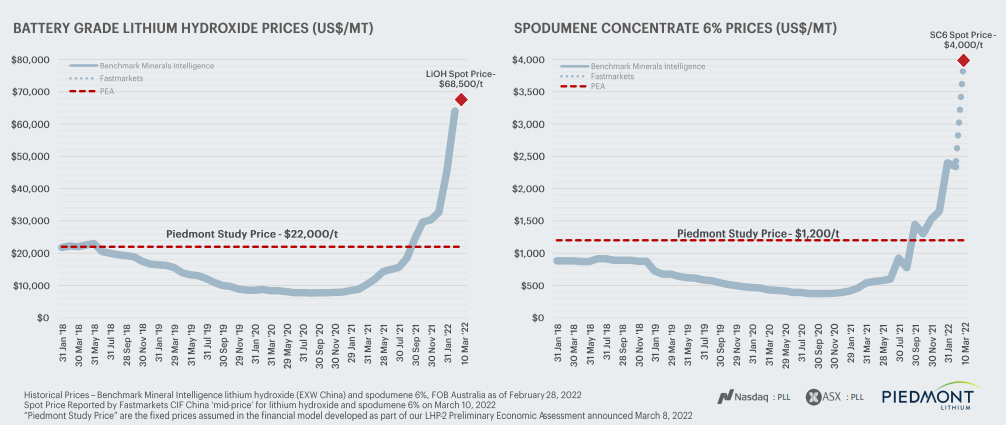

Could what we are seeing in metals happen in chemicals and polymers? Over the last few weeks, we have seen already high metals pricing spike even further, both because of production shortfalls and because of expectation of higher demand, especially in the renewables space, as conventional energy prices have spiked. We show a lithium example below, but note that after chaotic nickel trading last week and a halt to trading, the market has made some attempts to reopen this morning with renewed problems.

As noted in Exhibit 1 from today's daily report, the jump in oil prices has plunged the European polyethylene producers into the red and pushed Asian polyethylene producers further into the red. This will inevitably result in price increases as basic chemical and polymer producers will shut down at negative margins, and these price rises offer an opportunity for the US, Middle East, and select other producers.

With the rapid jump in international natural gas and oil prices, we would see very concerted efforts to raise basic chemicals and polymer prices in Europe and Asia and will have a positive knock-on effect for the US. In our weekly catalyst report on Monday, we showed that ethylene producers outside the US were all losing money, especially in Europe and Asia. Some European demand will already be lower, because of curtailed product exports to Russia and Ukraine, but producers will want to cover costs at a very minimum and consequently, will be trying to match price increases with cost increases and if possible do a bit better than that. All of this will create a greater margin umbrella for the US, and US exporters selling directly into international markets will see export margins step up and may see incremental opportunities to export more, assuming that the freight rates are not too onerous for incremental containers.

We are seeing pockets of real demand strength in some areas of chemicals, such as building products, and this is allowing producers to push through price increases to reflect higher costs and most likely add some margin. In other areas where the fundamentals might not be quite as supportive, we are still seeing attempts to pass on higher costs. Sika has supported what we have heard from many over the last few weeks, which is that the building products chain remains tight, as demand is strong, capacity is running hard and logistic issues continue to cause problems in some cases from a raw materials perspective and in others from getting finished products to market. Where there is limited ability to increase supply, those selling into the building products space are likely to make more money as they should have strong pricing power – in the US chemical space, we would favor Westlake as a potential big winner from this trend, but Huntsman should also be on the list.

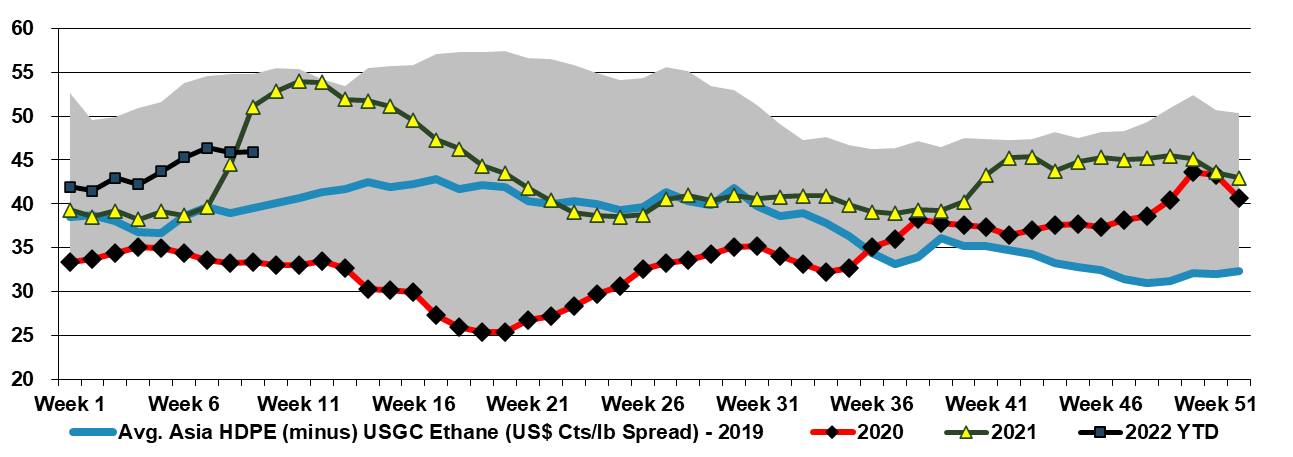

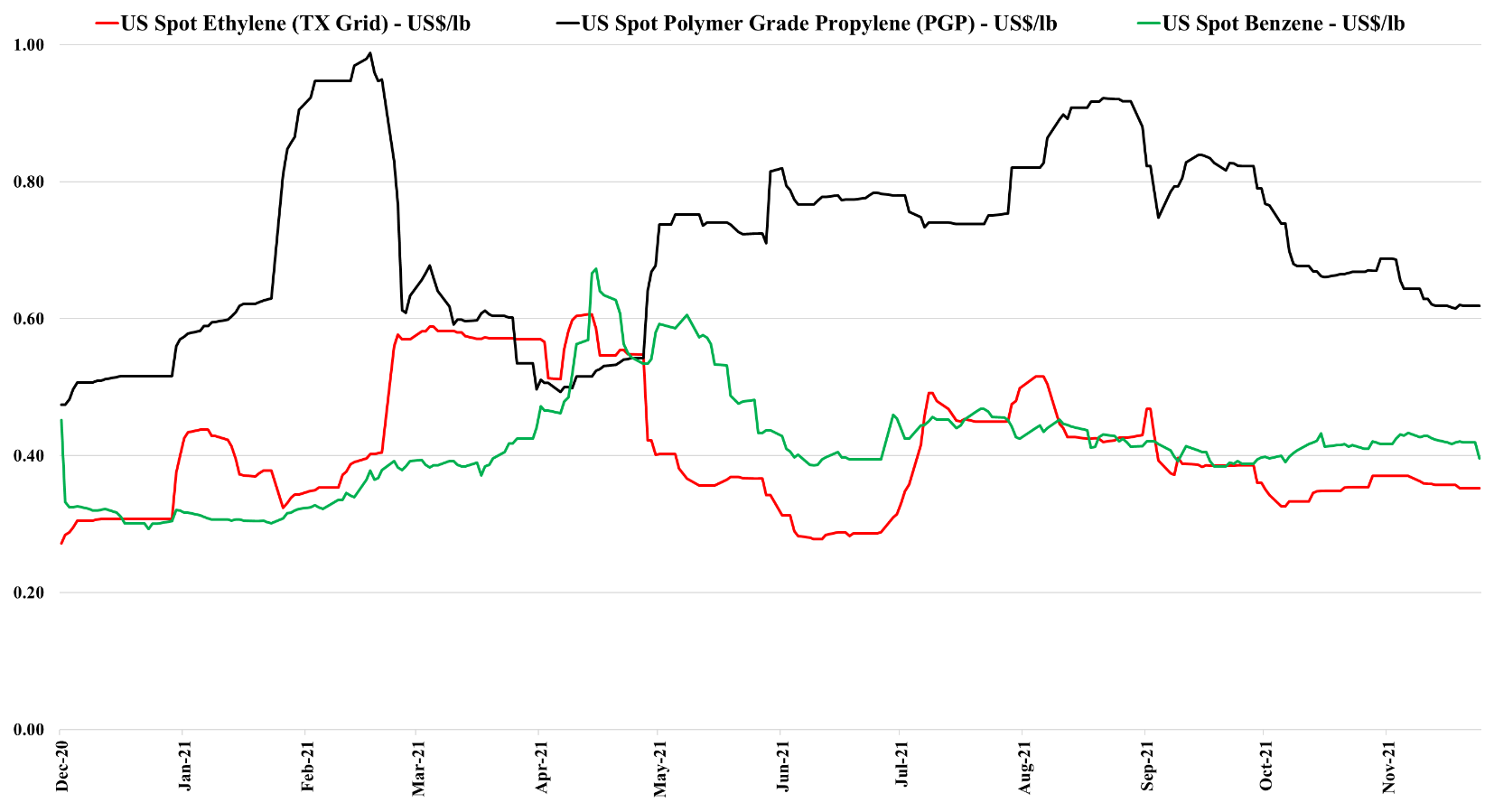

Following on from the Enterprise comments covered in our daily report, the company is more likely to acquire something in chemicals than build it in our view, especially if a move into ethylene or polymers is on the table. Today, building capacity will come with all sorts of emission-related restrictions most likely, and many of the new build announcements we have seen since COP26 have come with a carbon plan (Dow, Air Product, and Borouge). While it is not obvious today that any Gulf Coast ethylene capacity is up for sale, we would imagine that most companies are reviewing strategy and evaluating whether they have assets of entire businesses that may have a better owner. This would be especially true if a basic chemical business is holding back the valuation of a more interesting core. In the recent past, we have talked about the relative value arbitrage open to LyondellBasell from separating its compounding, licensing, and recycling business from the core. Maybe the core would fit well with Enterprise? As the chart below shows, there is money in buying ethylene for export, but there is more money in the US in making ethylene, as discussed in our daily report.

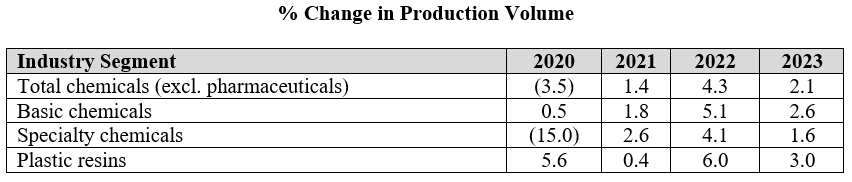

The ACC forecasts below leave us a little confused as the implication for specialty chemicals is that production declines in the US by an average of 2.0% per annum from 2019 to 2023. Given the demand that we are seeing for US manufacturing, as covered in our most recent Sunday Report, we would expect demand for all inputs to rise and it is unlikely that the gap would be filled by a swing in net imports. The lower demand from the Auto industry in 2020 and 2021 and broader manufacturing shutdowns in 2020 explains the 2020 and 2021 numbers to a degree, but it is not clear why there would not be a rebound as auto rates increase. We would also expect to see a stronger rebound in polymer production in 2022, assuming weather events are less impactful than in 2021, given substantial new capacity for polyethylene from ExxonMobil/SABIC, BayStar, and Shell.

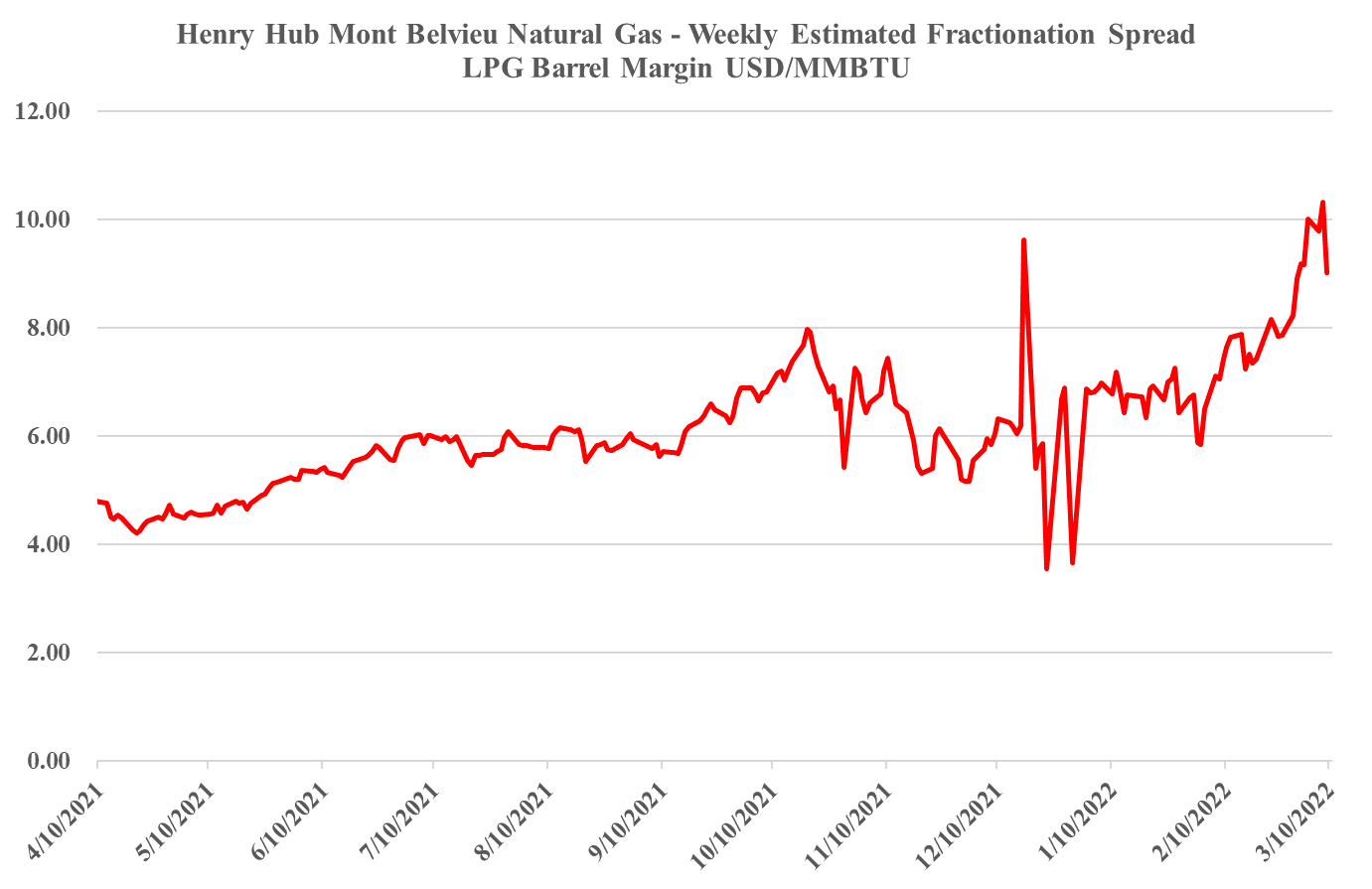

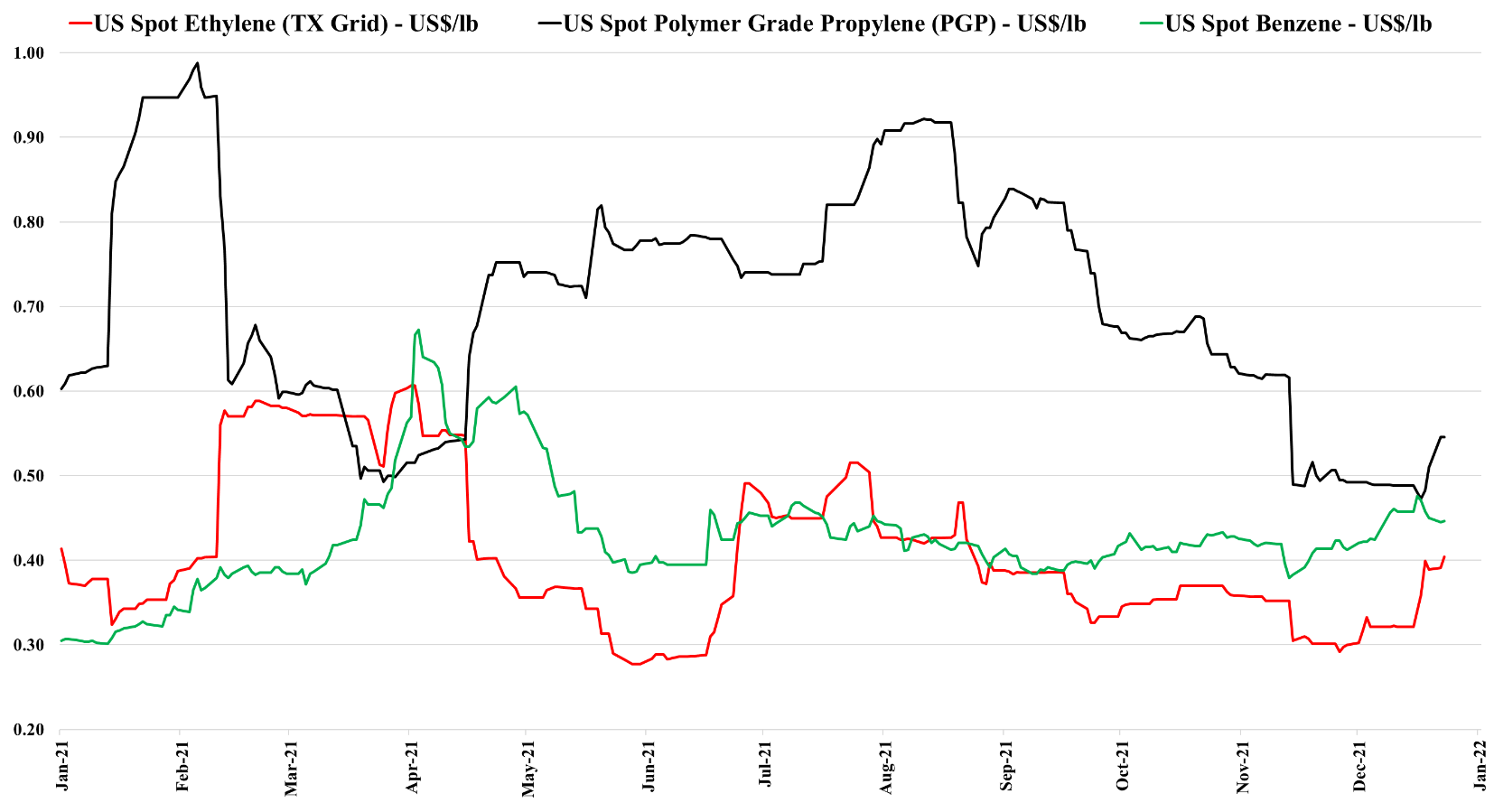

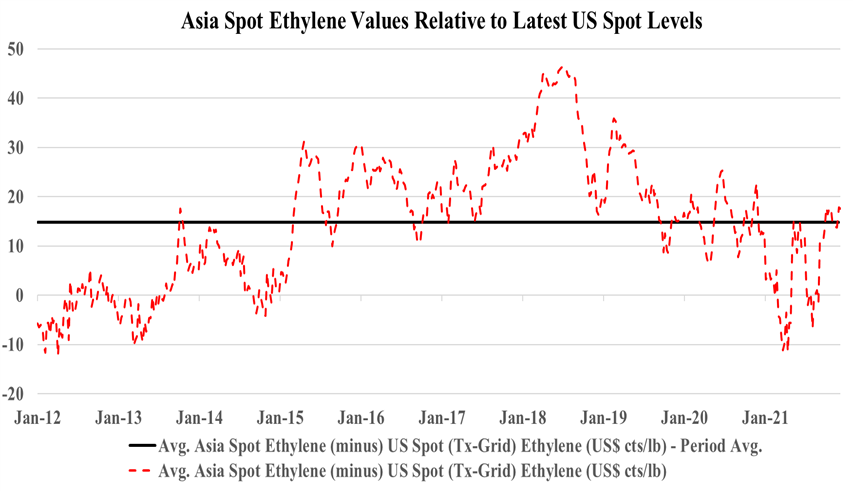

The drop in US benzene pricing is likely a function of lower crude oil pricing and the overall impact this is having on oil product values. As the US has moved to much lighter ethylene feedstocks, the proportion of benzene that is coming from refining is overwhelming and alternative values for benzene or reformate in the gasoline pool are a strong driver of US and international pricing. Lower naphtha pricing for ethylene units outside the US will also hurt benzene values. By contrast, the stronger natural gas market – through the end of last week - supported ethane pricing in the US and we saw a step up in propane pricing – which have provided support for ethylene and propylene – also note that the analysis we published yesterday in the weekly catalyst suggests that the US can export ethylene to Asia at current prices – delivering ethylene into the region below current local costs. This should keep a floor under US ethylene pricing although any further decline in crude oil prices relative to US natural gas and NGLs will close this arbitrage.

In an important, but inevitable, change in tone, it is worth noting that the Borouge ethylene expansion announcement includes the idea that the complex will explore the possibility of a major carbon capture facility that will take much of the CO2 from the existing complex as well as the new plant. We have stated previously that the mood has changed sufficiently such that large industrial investments without a carbon abatement plan will not get approval from stakeholders and this is a prime example of what we expect. Locations with low-cost CCS will see disproportionate investment in our view and Abu Dhabi already has CCS in place as Adnoc is selling blue ammonia already to Japan. As we noted in a recent Sunday Piece, we expect carbon abatement challenges to slow expansions in basic chemicals and, despite this announcement by Borealis, see a market shortage in 2024/25 as a consequence.