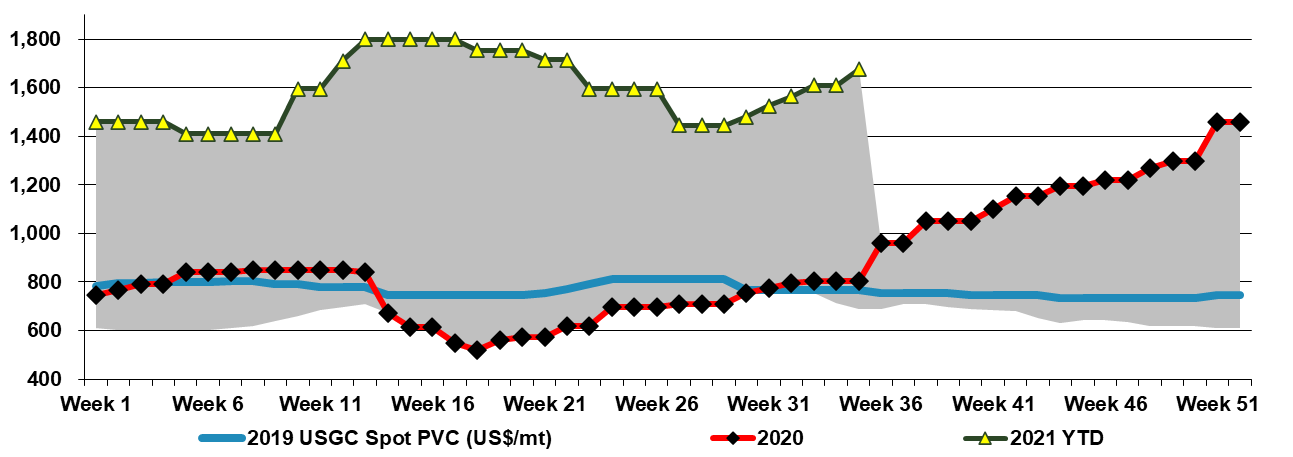

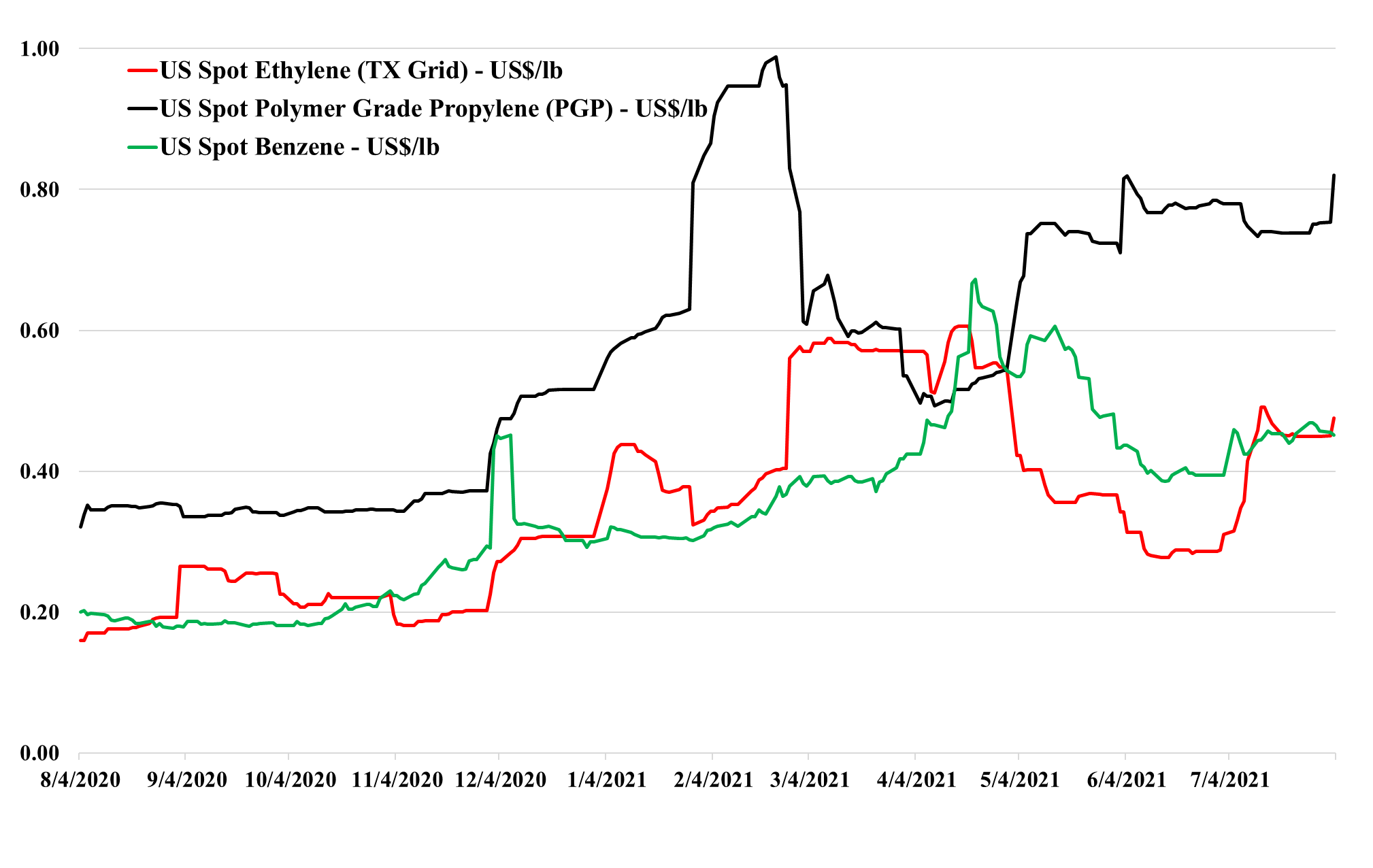

It is increasingly likely that Hurricane Ida will add another leg of strength to US chemical pricing more broadly, with a host of prolonged production outage news and force majeure notices, giving momentum to some price increase announcements for September, some of which looked very speculative at the time they were made. Buyers will have an eye on continued pockets of supply chain disruption, strong demand in general, particularly for those levered to holiday spending, and the not insignificant fact that we still have almost three months of hurricane season to go! Note that two of the more disruptive storms of 2020 hit in October. We talk specifically about PVC in today's daily - See price chart below.

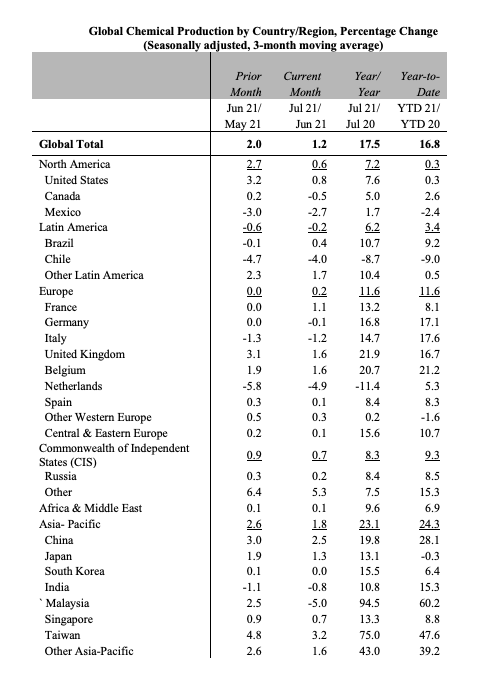

The advanced nature of the ExxonMobil/SABIC project, which we have discussed previously, is another cause for concern around US polyethylene market strength for a couple of reasons. First, it is only the first wave, with Baystar and Shell hot on the heels in 1H 2020. Second, it will add another ethylene seller in the US – SABIC – and this may be enough to cause some ripples. If you look at this in the context of the Asia production growth data provided by the ACC (below) there should be a significant cause for concern around the global balance for many products. Some of the specific Asia country growth, year on year and year to date, is driven by COVID-related shutdowns in 2020 – Taiwan and Malaysia for example – but the bulk of the China growth, which is more significant in absolute volume terms is from new capacity. China’s ability to sell surpluses internationally is hindered by the current logistic problems, but these will not last, and we should also factor in where the material will go that had been imported into China. The global polyethylene market could look very different in 2022, although all eyes will be focused on Hurricane Ida for the next week. See more in today's daily report.

Is this the beginning of the end? The linked report that US traders are struggling to find export homes for incremental HDPE should not be a surprise given the significant price difference between the US domestic price and prices in other markets – Exhibit 1 in today's daily report. HDPE is the more fungible polyethylene, with both LLDPE and LDPE much more grade and application-specific. It is often the first polyethylene grade to spike in a shortage and fall when there is a surplus.

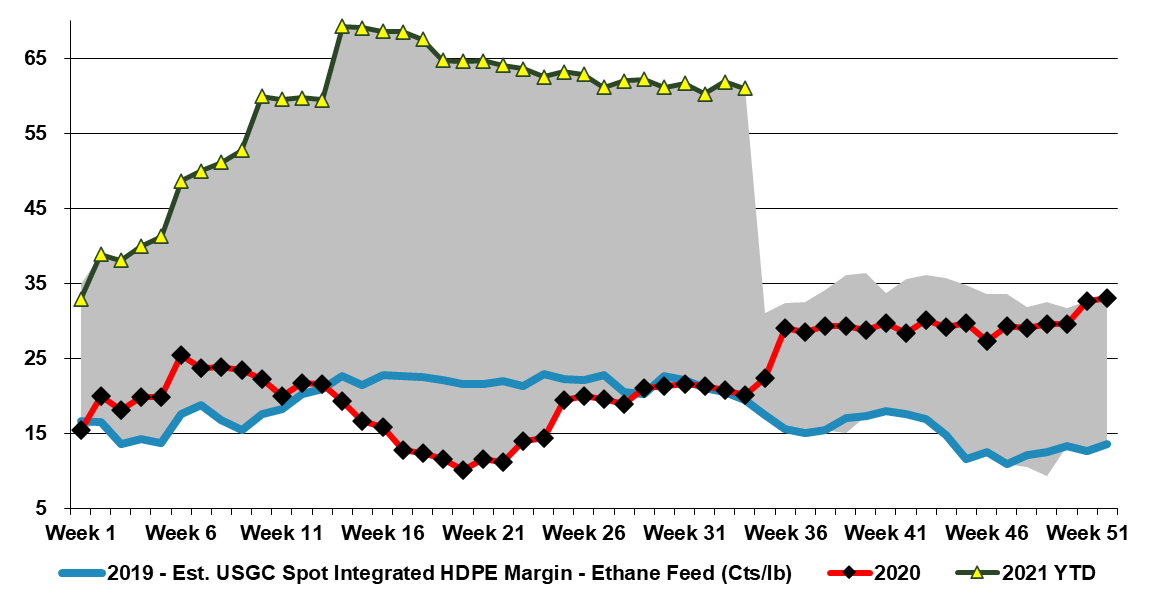

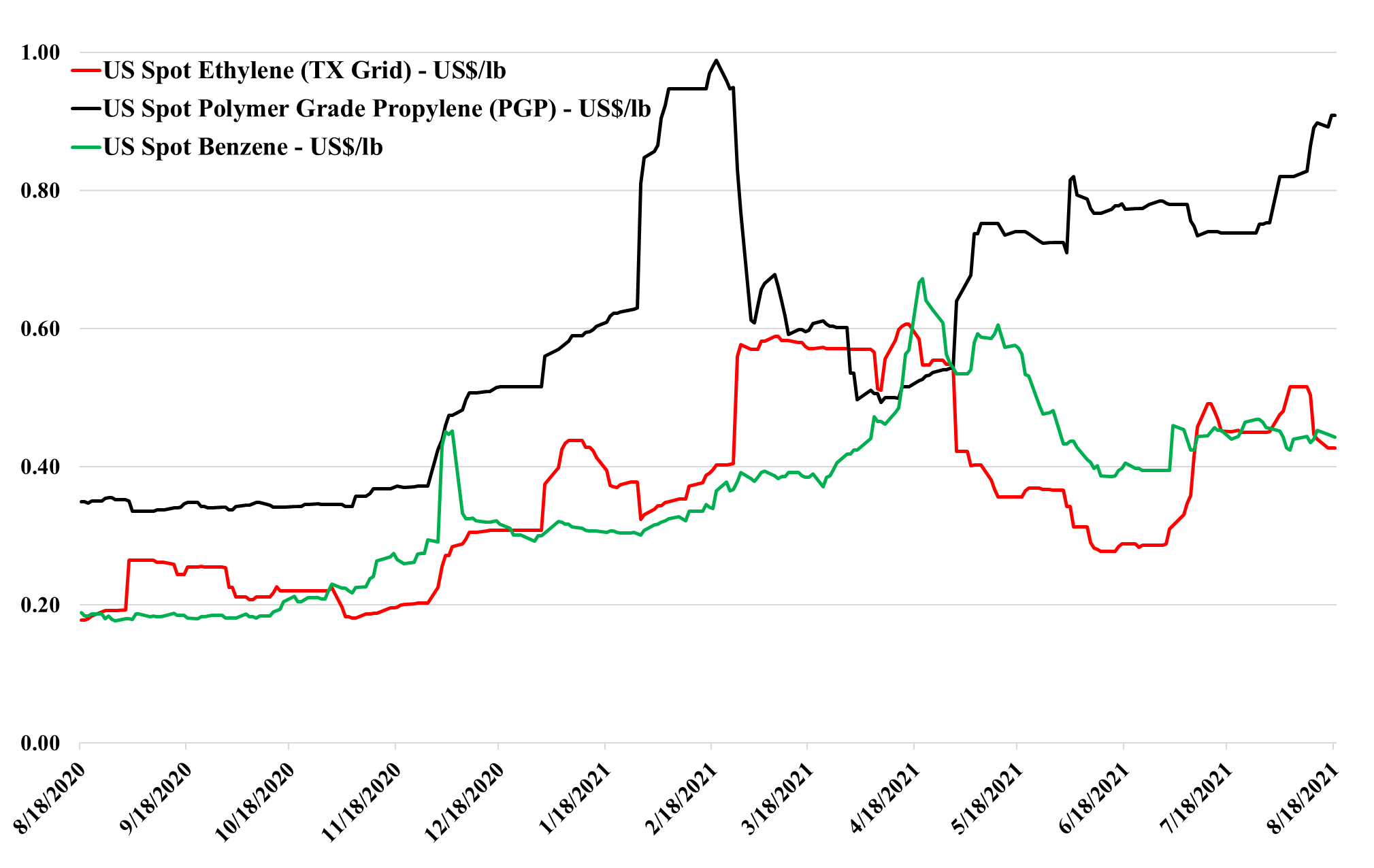

Before the wave on new ethylene capacity came online in the US there were several low-cost expansion projects all of which added the ability to crack ethane and some of which brought constraints around feedstock flexibility. Consequently, it is less clear than it used to be just how much US ethylene capacity can flex to exploit the very attractive light naphtha economics today. Very conservatively, we would estimate that 5-6 million tons of capacity can flex easily and about the same again with some planning and some logistic adjustments. Among the public companies, both Dow and LyondellBasell are well placed, and likely have at least 1 million tons each of flexible capacity – in both cases, there is a need for propylene and LyondellBasell has significant butadiene/C4s capacity. For context, at current prices, both companies are likely looking at an additional ethylene margin benefit in the US of $2.5-3.0 million per week for as long as this opportunity exists. This would be 0.3 cents per share per week for Dow and 0.7 cents per share per week for LyondellBasell – a rounding error in current earning but more free cash regardless. The chart below shows the unprecedented benefit in the US and see our daily report for more.

Propylene prices are rising again in the US, in part because of the propane price increase discussed in today's daily, but also because of reduced availability from other sources. These higher prices maintain upward pressure on propylene derivative pricing and we have to question how markets will adapt to much higher propylene and derivative pricing than ethylene and derivatives. There are several areas of potential overlap, where ethylene derivatives could take share from propylene derivatives and if the price deltas remain high and users become convinced that this could be the norm, it is reasonable to expect that propylene demand growth slows incrementally and ethylene demand growth benefits. In the immediate term, some quick switches could happen, but just as propylene demand marched ahead in the 1990s and 2000s because investments were made to use propylene derivatives instead of ethylene derivatives, we could begin to see investment to reverse the process. This was an incremental process for propylene over decades and we would not expect to see anything less incremental in the other direction, but ultimately this could be good for the more focused US ethylene and derivative markets if it accelerates growth in onshore demand and decreases the reliance on exports.

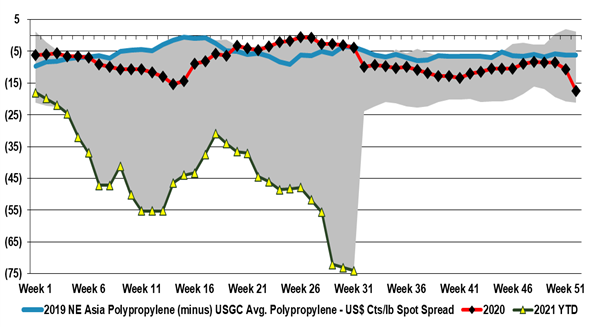

The ICIS polypropylene analysis in the linked headline is interesting in that it shows the vulnerability of the traditional exporters of polypropylene to China if China goes ahead with the longer-term capacity announcements that local producers have made to date. The analysis suggests that this development will move China moves from deficit to surplus in PP.. Where the analysis may be wrong in our view is that the current high price of propane, low ethylene margins, and low local polypropylene margins could put portions of the planned capacity on hold, and while it may come eventually, the phasing of additions may be different. Current economics make any ethylene (and associated propylene) investments hard to justify and the same with PDH. In the past, we have seen China pull back investments when economics have not worked – most notably in the early part of the last decade when oil prices were very high. At that time China moved to projects based on coal, and while that may re-emerge, local oversupply, in general, will slow things down in our view, and pushing back towards coal may not fit with whatever carbon emission targets China will set ahead of the COP26 meeting.

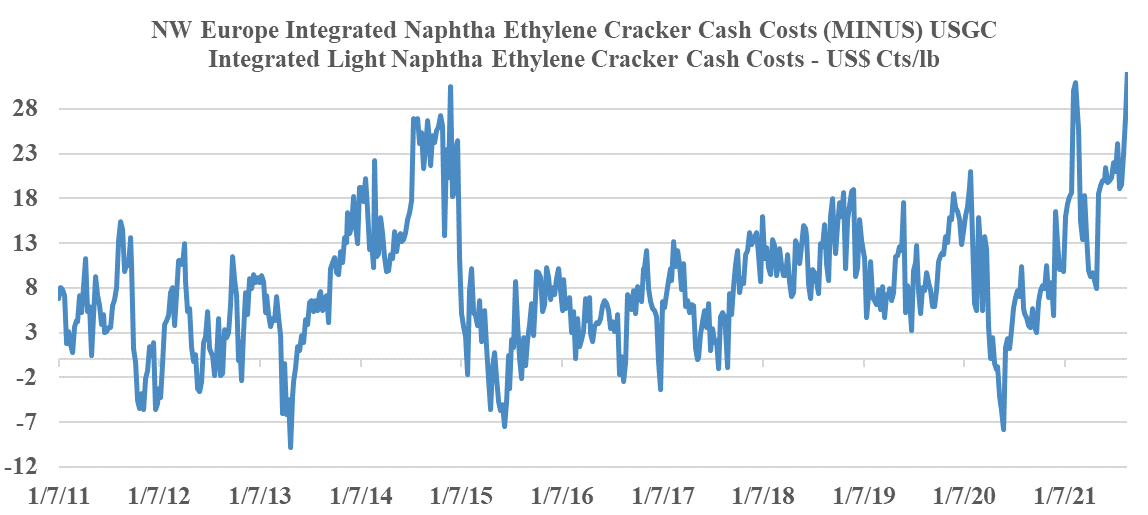

If this commodity cycle has the same drivers as prior cycles, producers like LyondellBasell and others will make comments like “stronger of longer” until prices turn, and if history is any guide, that turn will catch everyone by surprise, and even if it does not, there is no upside for any producer in predicting its end. As with all commodities, markets are tight until they are not, and markets are long until they are not. If you look at the ethylene and propylene price movements in the exhibit below you can see the speed of change that is possible and while the slope may be less severe for polymers in both directions, it can still be abrupt. The worst-case for the US industry would be a step down in demand coincident with the rising natural gas trend. There is no evidence of demand weakness today, but there will not be until it is happening. The extraordinary incremental freight rates shown in Exhibit 1 of today's daily report, make it increasingly unlikely that anyone sitting on surplus polyethylene or polypropylene in Asia can exploit the regional price difference. When demand and sentiment around supply chains turn, we would expect this spot shipping rate to collapse also – but there is no sign of that today.

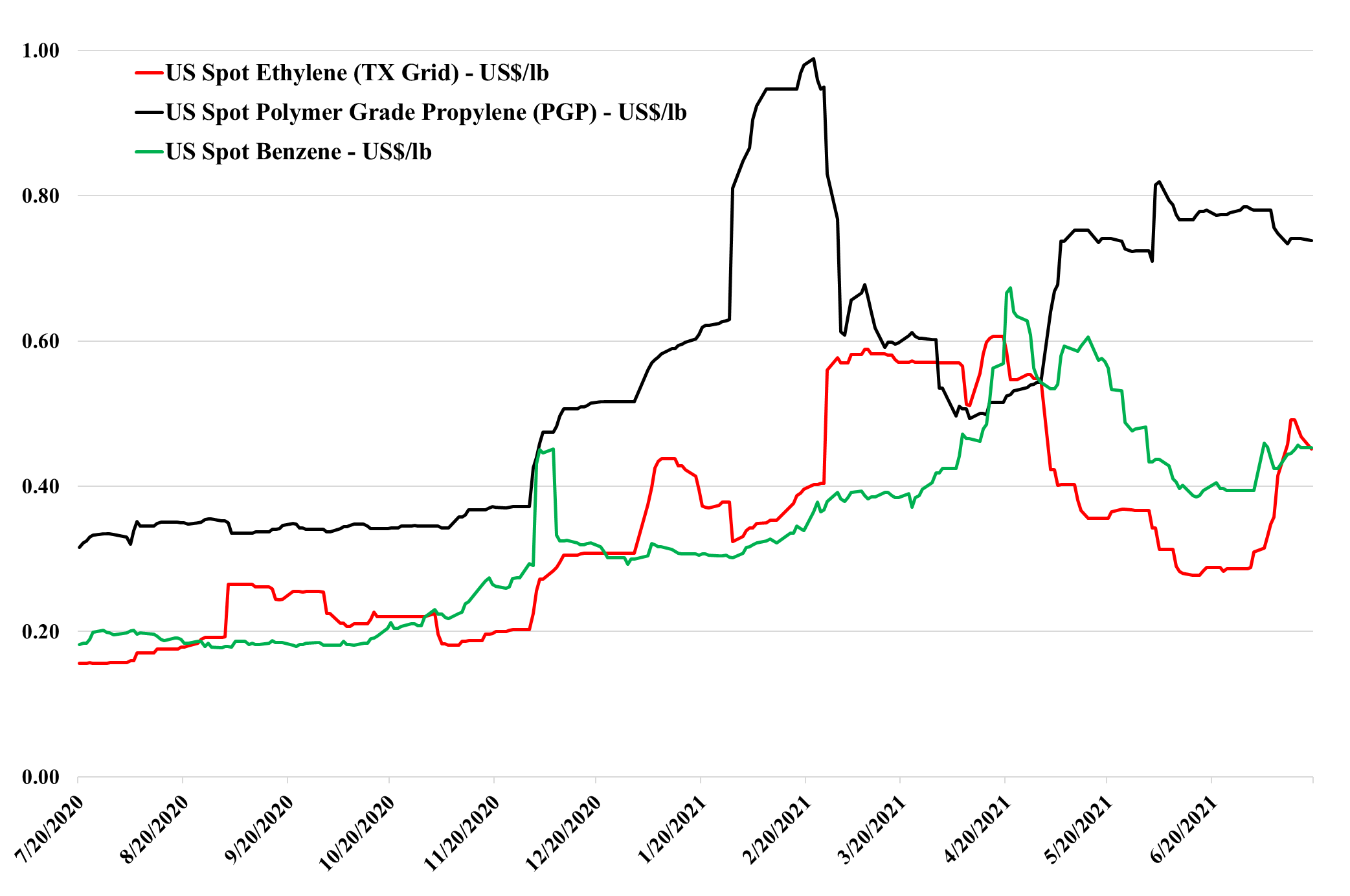

We focus on ethylene price trends today, as we discuss it’s movement and related ethane tightness in today's daily report – more operating ethylene capacity means more ethylene (depressing prices) but it also means more ethane demand, inflating its price. Margins remain robust, even with the feedstock increase and the price decline and it is important to remember that any decline in US ethylene prices would be stopped at a level that allowed increased exports, which would still be well above US costs. With the full ethylene fleet operating in the US, there is a surplus (i.e. more ethylene than there is consuming capacity) so we expect export economics to drive spot pricing under “normal” circumstances. Abnormal production outages over the last year have seen that export surplus come and go a couple of times and the price volatility the Exhibit below shows that.

ExxonMobil Chemicals has announced that its Corpus Christi JV project with SABIC is ahead of its original schedule – ExxonMobil is now targeting a start-up in 2H21, ahead of its previously targeted 1H22 expectation. It is unusual for projects in the US to be ready ahead of schedule these days, and start-up delays tend to be the norm. We also take a positive view of this development upon comparison to the Shell Pennsylvania project, which still has a vague 2022 start-up expectation though its construction began before ExxonMobil. One could argue that the remoteness of the location – well away from petrochemical infrastructure has been a constraint for Shell, but the Corpus Christi location is also a greenfield project for ExxonMobil/SABIC. This will be the largest ethylene plant built in the US, though it is likely that the recent 1.5 million ton units (Dow, ExxonMobil, CP Chem) are expandable to 2.0 million tons. Dow is already discussing such a move with a new polyethylene facility at Freeport. It will be interesting to see what impact this ExxonMobil/SABIC facility has on both the USGC ethane market and the polyethylene market – 1.3 million tons of polyethylene is a large increment and SABIC will have half of the capacity and will be a new market entrant with on-shore production. Aramco has ethylene, through Motiva’s purchase of Flint Hills, and SABIC owns half of the Cosmar styrene plant in Louisiana.

We note the volatility in ethylene in the chart below and point out that ethylene sits in a precarious no-mans-land in the US with pricing neither reflecting costs nor incremental value in use. The downside to generating buying interest in Asia is significant – more than 25% - but an incremental buyer in the US could pay much more than the current price – in many cases to meet export obligations, let alone for domestic sales. We would expect the volatility to continue, with a downside from better production rates and upside from more constraints – demand fluctuations are likely immaterial relative to the impact that supply moves could have. See more in today's daily report.