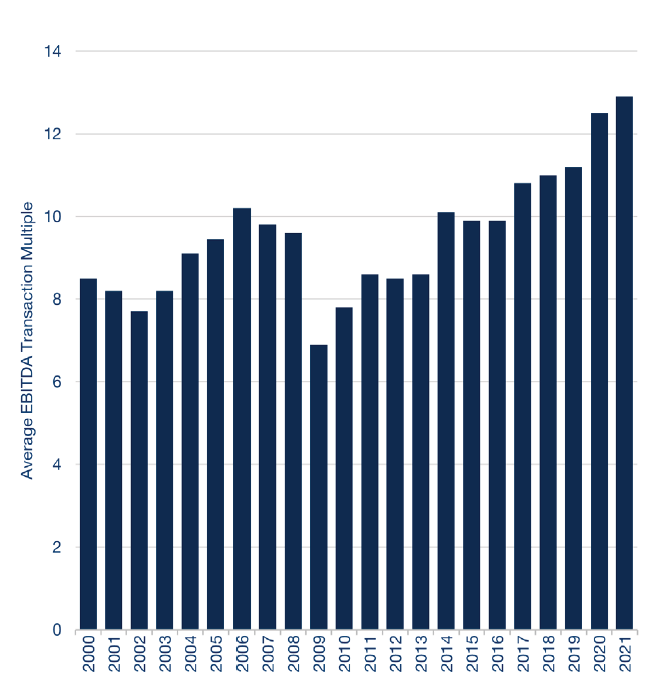

Our Sunday Thematic research a week ago (see linked report) discussed slowing growth investment in the traditional commodity chemical industry and suggested that ESG and climate pressures might slow investment even further. Yesterday, our Sunday Thematic made the argument that some of those dollars will target strategic M&A. We have recently seen an uptick in global chemicals sector M&A, and we find few items suggesting activity levels will slow in the near-to-medium term. In part, we think strategic M&A will be easier to get Board approval for than “new build” capacity additions, and it can be viewed as better use than holding cash or complementary to dividends and buybacks. Also, ESG and climate concerns could spur M&A activity, as companies look to separate bad emission assets from good ones – especially if the market values them very differently.

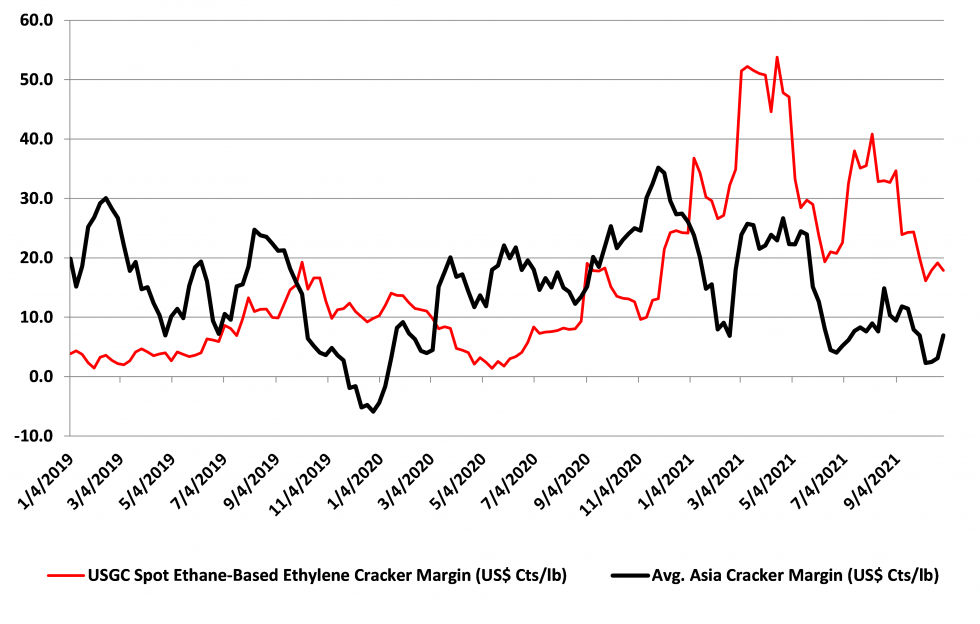

Clearly, as a direct consequence of our shortage theme this week, ExxonMobil announces a large new complex in China is through FID. This may be the company rushing something ahead before tighter restrictions are imposed or it may be an indication that with a 2060 net-zero pledge China is going to let things slide for a while. We would not be surprised to see ExxonMobil face some bad PR around this project if there is not some emission abatement plan with it. The facility will give ExxonMobil some further integration – effectively consuming equity hydrocarbons – but, if the company is setting itself up for criticism for investing in jurisdictions with lower emissions standards, this could backfire. It is also a very counter-cyclical investment given the poor profitability seen in the region right now (chart below) and as we discussed in our Sunday Piece - Waiting For The Big One – Is A Chemical Mega-Cycle Ahead?.

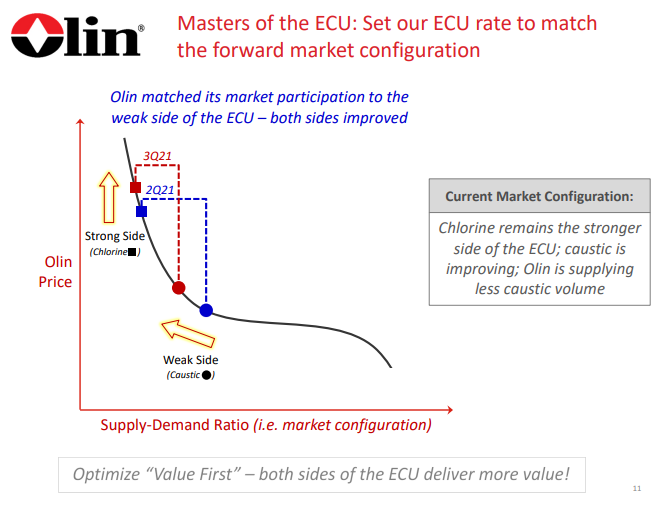

We will expand on the Olin results and some of the benefits and potential pitfalls of the revised strategy in our Sunday piece as we can draw some comparisons (some good and some bad) from other corporate examples over time. For now, it is working and few would have predicted a $50+ stock for Olin a year ago. Some market fundamentals are working in Olin’s favor, but much of the success is coming from a more radical approach to customer engagement and avoidance of customers generating minimal returns, regardless of what that means for production. So far this is a great first act from the new leadership of Scott Sutton – we will talk about what a second act may need to look like on Sunday.

Our latest Sunday Thematic report, "Damned if you Dow and Damned if you Down’t. Hard to win", centers around Dow's announced development of a new net-zero carbon emissions site in Alberta, Canada. It discusses company-specific and sector ramifications for Dow's strategic move to produce low-cost low carbon polyethylene in Canada while also expanding capacity.

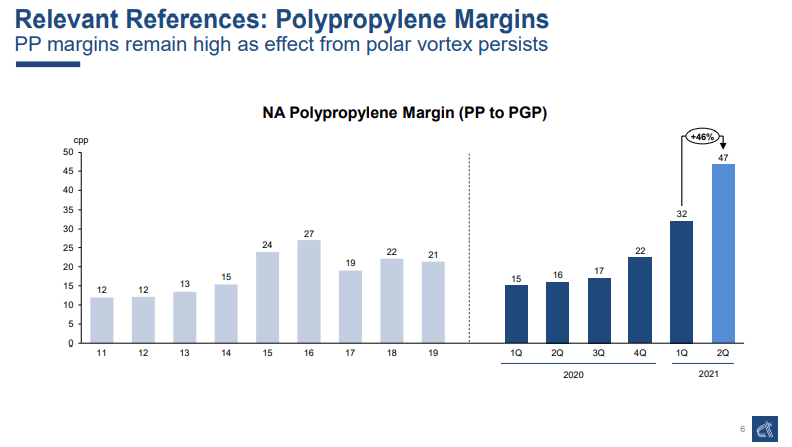

The much higher polypropylene margins in the US come despite very high propylene pricing, and the whole chain did well in the first half of the year. Demand for polypropylene has been significantly stronger than most expected year to date, although production outages have helped the market, and what we had expected to be a surplus in the US in 2021, precipitated by the Braskem start-up has turned out to be production coming online just in time and prices might have been higher still had the Braskem plant not been there. We see some of the demand as cyclical - in response to consumer durables, though there has been lower use in the auto industry because of the production cutbacks. See more in today's daily report.