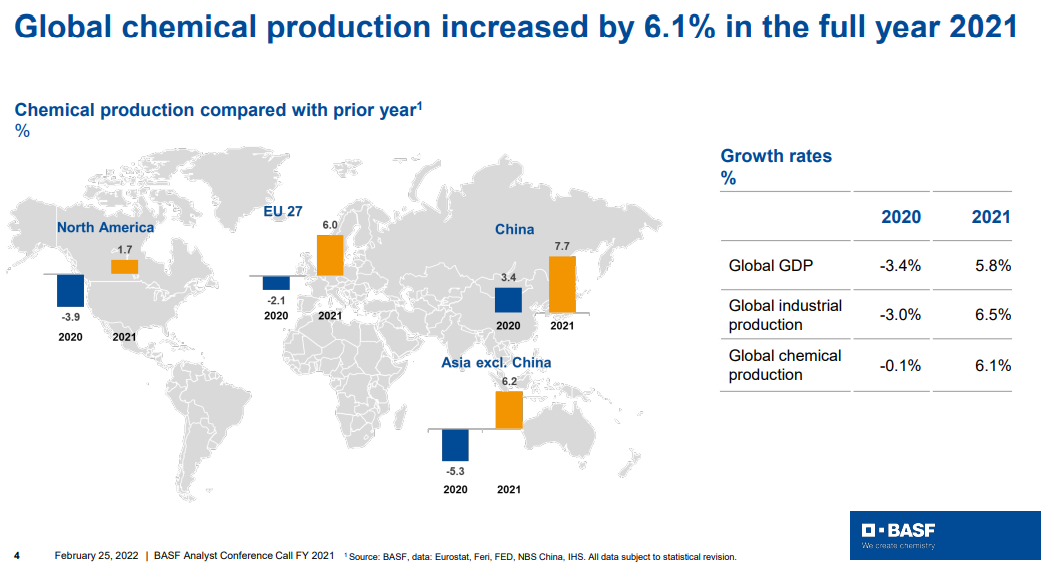

Fear of shortages is the one factor that is most supportive in terms of helping to push through pricing and the events in Europe and their associated impact on energy prices should be all the support that the chemical and polymer industry needs to push pricing through that will cover cost inflation. Buyers of raw materials and intermediate products will naturally look to buy a little more than they need in the near term, both to ensure that they get something ad to try to build a bigger inventory cushion. This will have the effect of pushing apparent demand higher, making the pricing initiatives easier. Few will push back on pricing if their primary concern is availability. Looking at the BASF results summarized in the chart below, demand is already very robust and this will lead to higher utilization rates and higher volumes for chemical producers as well as high pricing. The commodity producers are likely more interesting here as they can move prices much more quickly than the specialty companies who might see margins squeezed over the next couple of months. None of this is good for inflation. See more in today's daily report.

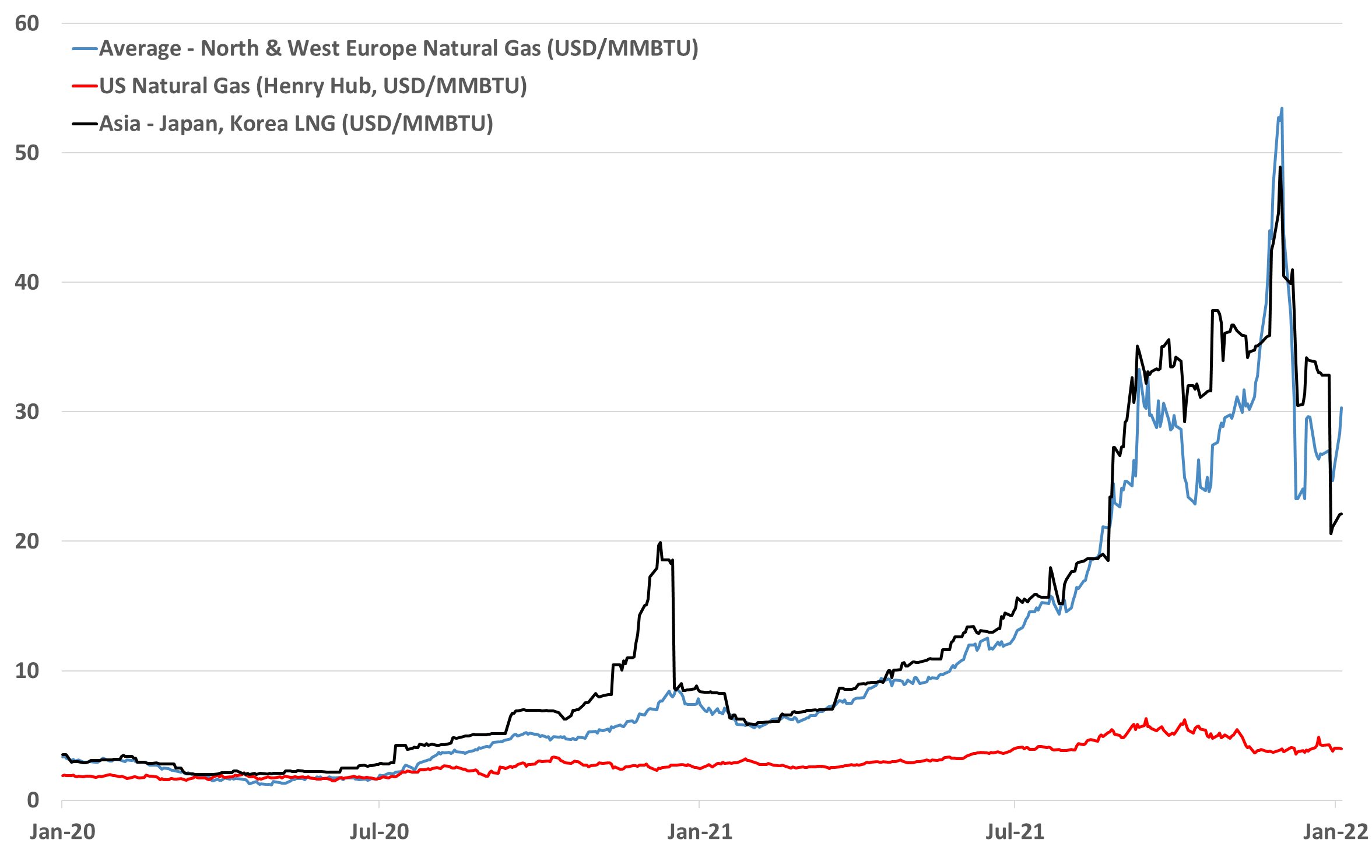

It is likely a difficult day for the European chemical industry as all of the fuel prices that they depend on are rising quickly, which will force many difficult decisions over the coming days. There are a couple of factors to consider – what happens to costs and margins if energy prices remain inflated, and what happens if energy availability becomes an issue and plant closures are necessary. In a world that is already reeling from inflationary pressure that we have not seen in four decades, there is at least an acceptance that prices can move higher, but the energy-dependent European industrial and materials companies will need to move prices quickly and meaningfully to absorb their higher costs. If natural gas supplies from Russia are halted, Europe is likely going to need to allocate supplies, as there is no easy fix given an LNG system that is already at capacity. Industry will likely take the hit to ensure power for heating and cooling. This will drive product shortages in Europe, especially for chemicals, which will likely make it easier to get the pricing necessary to cover costs.

Westlake Chemical began today at a 52 week high on the back of very strong earnings but has retreated with the market. Westlake has been one of our favorite ideas since founding C-MACC in part because we believe in the diversification strategy into building products and in part because the PVC market has not seen the same level of overinvestment as polyolefins globally over the last 3 years. Westlake’s view of the housing and construction market aligns with ours and by breaking out this segment of the business Westlake should see some valuation benefit from the more stable earnings that this segment should provide. Note that the focused building products companies trade at significantly higher multiples than chemicals. We expect Westlake to get earnings and multiple boosts from here.

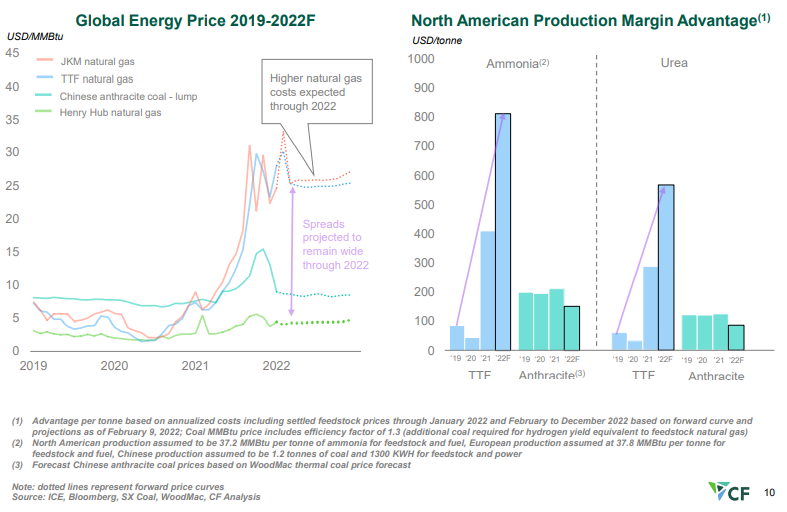

The CF slide below shows very clearly the US competitive edge when it comes to making anything that has a natural gas base, and while we tend to talk mostly about ethylene, ammonia, urea, other ammonia derivatives, and methanol are all seeing significant cost advantages. The Chinese coal-based costs are better than those in Europe and Asia based on natural gas but margins remain well below those in the US. The challenge with the coal-based chemistry in China is that it has substantial CO2 emissions, and the facilities were not designed for carbon capture. As China develops a carbon cap and trade market and as these facilities get included, costs will rise significantly.

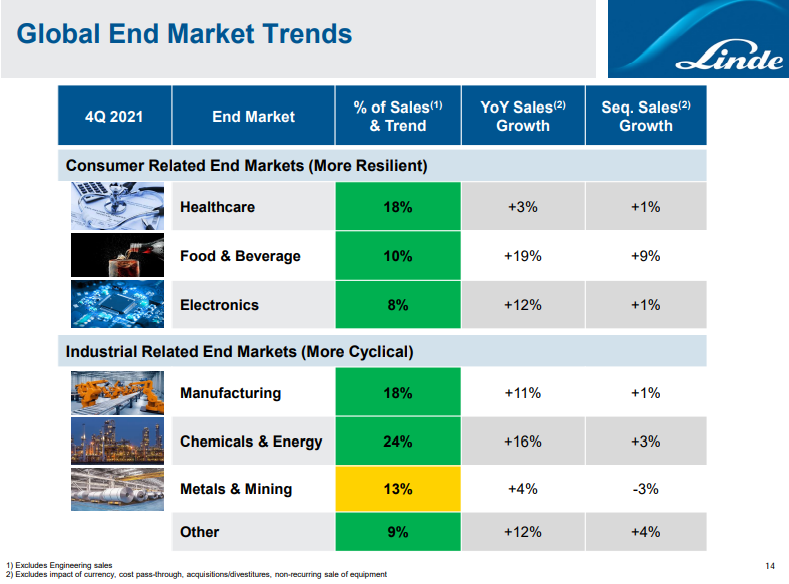

While the Linde results were very strong and surprised to the upside, we also want to focus on what messages they send about the broader economy. As recently as 10 years ago all of the industrial gas companies' results provided a reasonable barometer on the state of the industrial and other parts of the global economy. Industrial gases are an enabling raw material or process gas for so many industries that their direct use is generally a function of operating rates for the industry that they serve. Over the last 10 years, Air Products has deviated from the traditional model, with some very large investments targeting specific projects in Asia and the Middle East and their results are a less useful measure of overall economic activity. While both Air Liquide and Linde continue to reflect the broad economic backdrop well, both could be dragged into large projects around hydrogen over the coming years, and depending on how they choose to report earnings, we could lose the tangential “information” in their reported results. For now, the Linde results are very supportive of the broader industrial-economic strength that is being reflected in earnings and guidance across many industries, including chemicals and refining. The company has added comparisons with 2019 to show how much underlying growth has happened over the two years. While inflation and interest rate increases could slow things down, the Linde numbers confirm that we have a very positive demand backdrop today, and the company’s guidance would suggest that they think it can continue.

There are a couple of related topics in the charts below from today's daily report, as any conflict with Russia would almost inevitably impact European energy supply, raising prices for natural gas and pulling on as much LNG as possible. That said, we suspect that part of the recent run-up in prices has likely been to build a cushion of inventory, as much as that is possible with limited storage relative to demand.

The theme of our Sunday report (to be found here) will be inflation this week and the signs that we are seeing across multiple industries which suggest it could be more problematic and worsen in 2022. One of the focuses is energy and how the pressures to be seen as good citizens is lowering investment in oil and natural gas production, while the world is not far enough advanced on energy transition to be able to substitute for the missing hydrocarbons. We would agree with many of the recent comments from some segments of congress, which is that the answer is not to curtail exports of LNG and crude, as by doing so we will starve the rest of the world of hydrocarbons and create worse shortages than Europe and China are seeing today. The better solution would be to support “clean” US production of the lowest emission fuels possible – especially for natural gas. As we have noted in prior research, with a global solutions hat on, the relatively low costs of natural gas F&D costs in the US, when combined with what we expect to be relatively low costs of emission abatement in the US, should drive more investment in the US, creating jobs and export income.

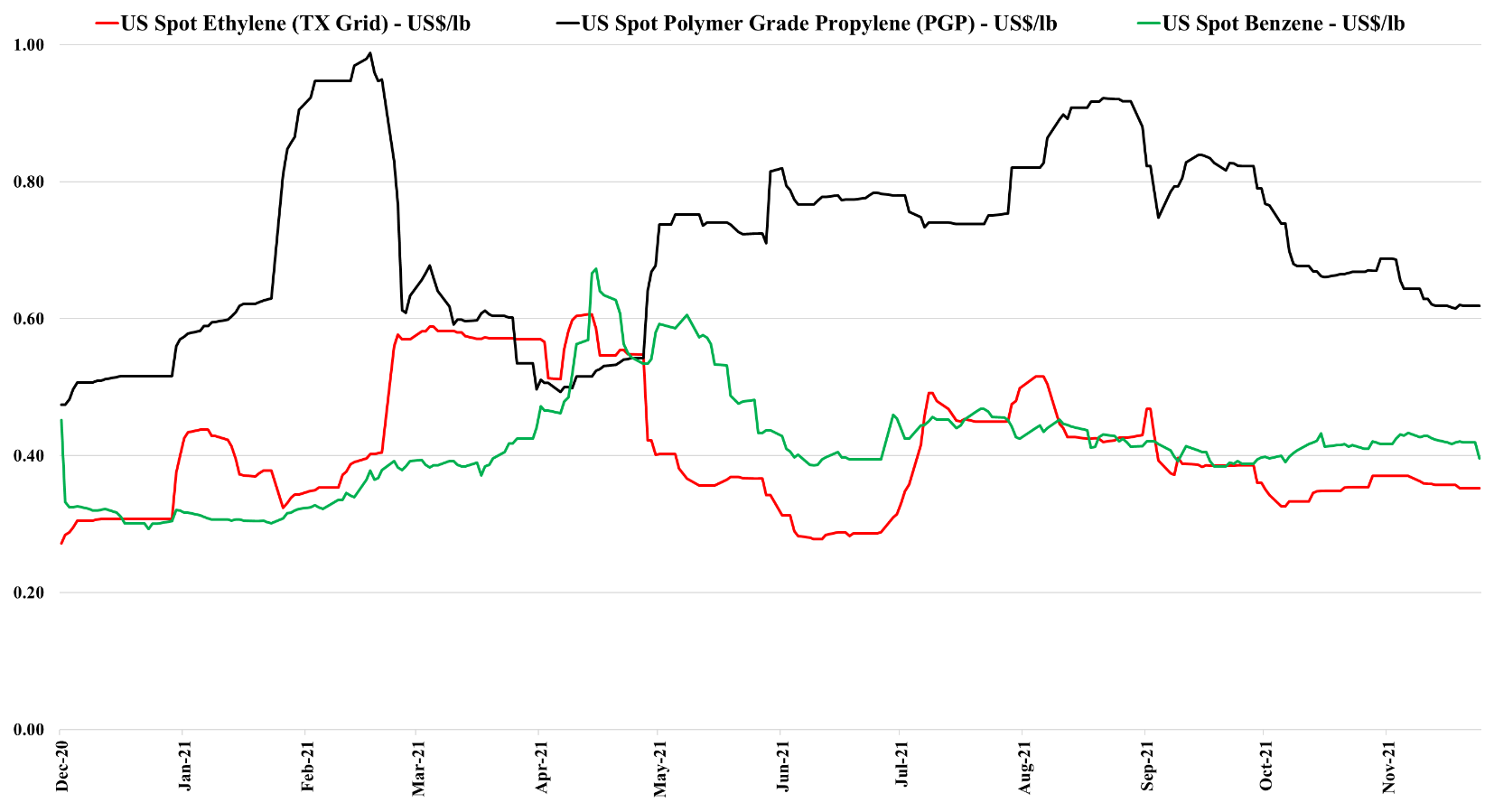

The decline in US and global chemical pricing this week (as discussed in today's daily) is a function of oversupply in the US and lower costs in the rest of the world. The US has had an incentive to produce everything for most of the year and has had essentially full capacity to do so since the beginning of the 4th quarter. This will have collided with seasonally weaker incremental demand in December and the recent abrupt drop in oil and gas prices to swing momentum very much in favor of buyers. Polymer prices have to date been more stubborn in the US, but we expect continued weakness here also through the end of the year.

The drop in US benzene pricing is likely a function of lower crude oil pricing and the overall impact this is having on oil product values. As the US has moved to much lighter ethylene feedstocks, the proportion of benzene that is coming from refining is overwhelming and alternative values for benzene or reformate in the gasoline pool are a strong driver of US and international pricing. Lower naphtha pricing for ethylene units outside the US will also hurt benzene values. By contrast, the stronger natural gas market – through the end of last week - supported ethane pricing in the US and we saw a step up in propane pricing – which have provided support for ethylene and propylene – also note that the analysis we published yesterday in the weekly catalyst suggests that the US can export ethylene to Asia at current prices – delivering ethylene into the region below current local costs. This should keep a floor under US ethylene pricing although any further decline in crude oil prices relative to US natural gas and NGLs will close this arbitrage.

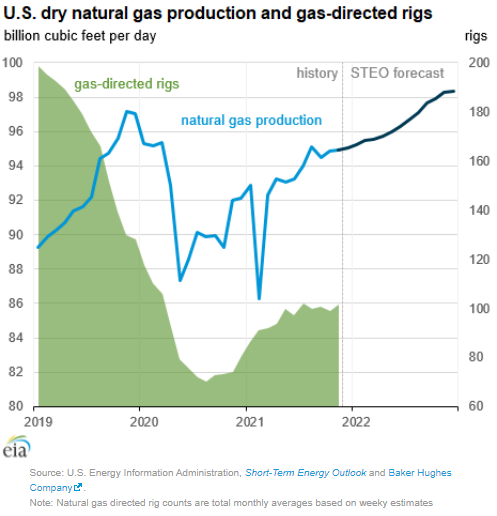

We should probably link the message in the exhibit below with the write-ups in both today's daily report and today's ESG and Climate report. The drop in E&P spending relative to cash flows and the shortage signals that are evident from the current oil and natural gas prices is likely to bump into rising hydrocarbon demand for the next several years, while the rate of renewable investment tires to catch up with energy growth before it can focus on energy substitution as meaningfully as the climate agenda would like. We also cannot look at the chart below and say that it does not matter because oil is less important in energy transition than natural gas. The oil-based investments in the Permian and Eagleford plays, in particular, have significant volumes of associated gas, and much of the natural gas supply growth in the US has come from these oil-centric investments. As they slow down, natural gas supply and NGL supply will be impacted, and while we are seeing increased rig counts in the natural gas biased regions, such as the Marcellus, the potential declines from the other fields will be hard to make up for.