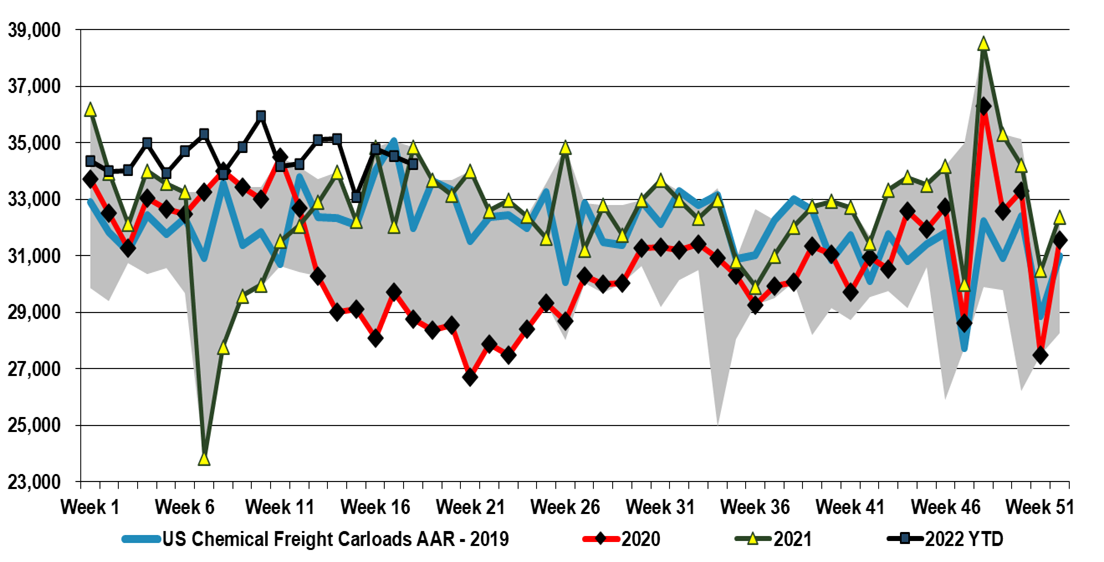

The US chemical rail volumes should be considered in the context of some of the slowing demand that has been indicated by companies downstream of chemicals, and we see this as further evidence for possible inventory build through the chain. Earlier in the year these builds would have been justified by supply chain issues that have plagued all segments of retail and manufacturing for close to two years, but today we should be at or above inventory comfort levels. We are calling for weakness in demand and some margin erosion in US chemicals and polymers in 2H 2022, before a strong rebound as early as 2024, but if buyers of polymers and chemicals and their customers look to reduce inventories more quickly, the landscape could change quickly. While this is possible, with the threat of higher energy prices very real, we would be surprised in anyone was interesting in dramatically lowering inventories today.

Part of our confidence/concern that prices can continue to rise in the chemical space in general stems from what seems to be very strong demand – again confirmed in earnings reports overnight, as well as in the rail data from today's daily report, as well as inventory data that suggest we are below recent ratios to shipment trends. The inventory piece is the great unknown here because the supply chain shocks of the last 20 months will have reset expectations around “safe” levels of inventory and it is hard to judge whether the new “comfort” normal will be back to the trend in the chart or 50% higher! If the new comfort level is materially higher than in the past, demand growth will remain strong and price momentum could continue through 2022. Our expectations for a mega-cycle in basic chemicals and polymers – targeting late 2023 and 2024 could be dragged forward because of higher apparent demand the time to buy the equities could be now, on that basis.

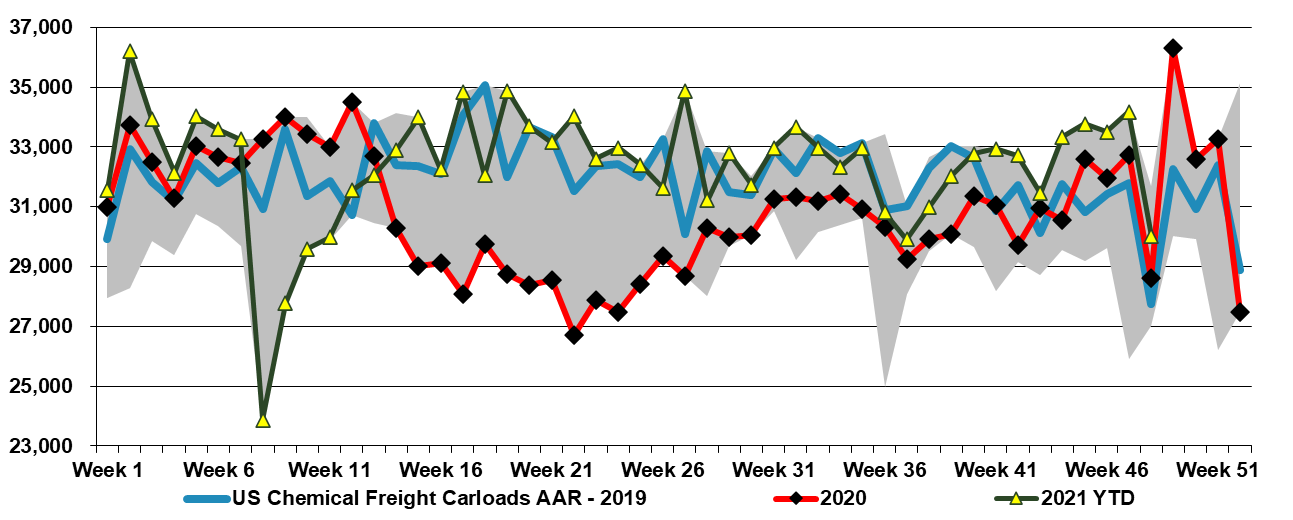

The decline in US and global chemical pricing this week (as discussed in today's daily) is a function of oversupply in the US and lower costs in the rest of the world. The US has had an incentive to produce everything for most of the year and has had essentially full capacity to do so since the beginning of the 4th quarter. This will have collided with seasonally weaker incremental demand in December and the recent abrupt drop in oil and gas prices to swing momentum very much in favor of buyers. Polymer prices have to date been more stubborn in the US, but we expect continued weakness here also through the end of the year.