We see BASF taking a major risk by reaffirming its 2022 outlook today, as the uncertainty factors, especially in Europe, are rising. This week’s inflation and economic growth data in Europe, suggest an economy that is lowing quickly and the confidence levels in Europe are much lower, as we have discussed already this week. BASF and others will likely continue to push prices, but if consumer spending continues to slow, volumes will disappoint and at some point, there will be pushback on both volumes and pricing. Separately, as we mentioned above, we could see another leg up in energy prices as we approach next winter in Europe, especially if there is no resolution to the Ukraine conflict, which seems likely.

The linked China polyethylene headline highlights a possible risk for US producers, as we link much of what is happening in China to logistic challenges. China has high production costs in a high oil environment, which is driving some of the cutbacks, but a portion is likely driven by an inability to move product and a huge disincentive to build inventory at break-even or negative margins. If the current shipping challenges in China roll over more aggressively into the rest of the world and container and vessel availability fall again, the US may face more challenges exporting polymers. As warehouse space fills, especially on the Gulf Coast, we may see some need to cut back rates, even if all of the material in storage currently has an agreed home and an agreed price. The US can afford to build inventory, as production costs still remain attractive relative to international prices, but if the supply chain is full there could be nowhere to put more material. One of Union Pacific's issues highlighted last week was too much inventory in rail cars, snarling up the system.

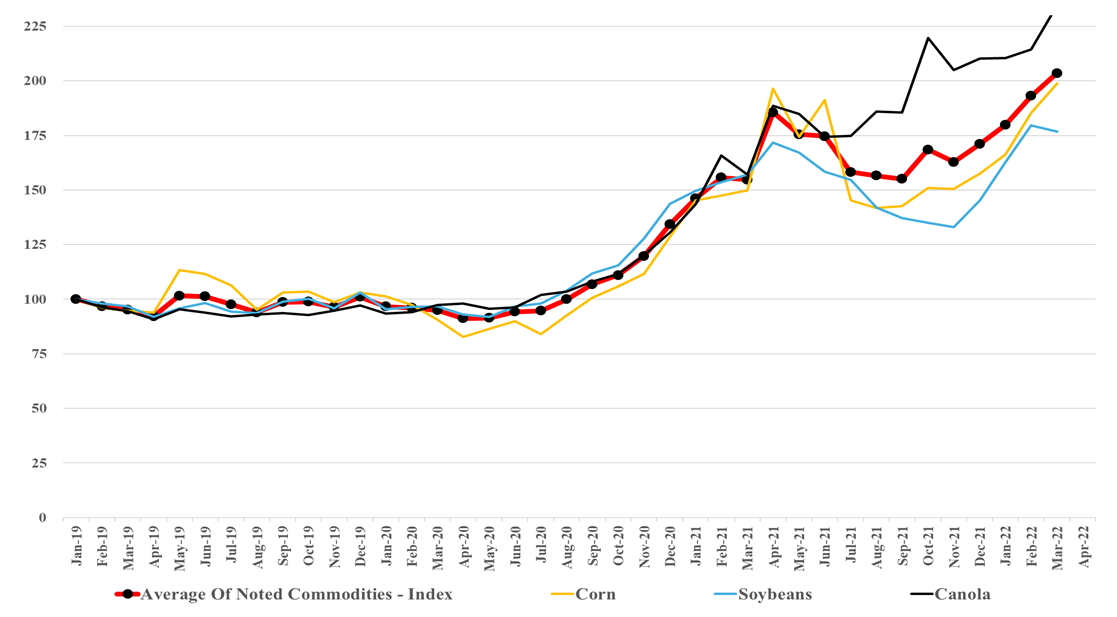

In our ESG and Climate report tomorrow, we are focusing on renewable materials and fuels, emphasizing counting carbon and the importance of verification and auditing. However, one of the side issues concerning renewables is their impact on food prices if they bid crops away from the food chain. The chart of the day from our daily chemical reactions report shows that corn prices are above their historical correlation with crude oil, but it also indicates a correlation and fuel markets can pay more for corn and other crop-based fuels when oil prices are high. The issue with exhibit below is that we already have inflated crop prices with minimal incremental demand for the fuel markets today. Prices are rising on strong global demand growth for food – supply chain issues that existed before the Ukraine crisis and – the supply challenges that are a direct consequence of the Ukraine crisis. This is before any significant investment in renewable fuels or materials. As governments implement policies to encourage renewable fuels – especially SAF – they need to consider what policies and incentives might be required in addition to price, encourage meaningful changes to the acres planted around the world, and help productivity where it is low.

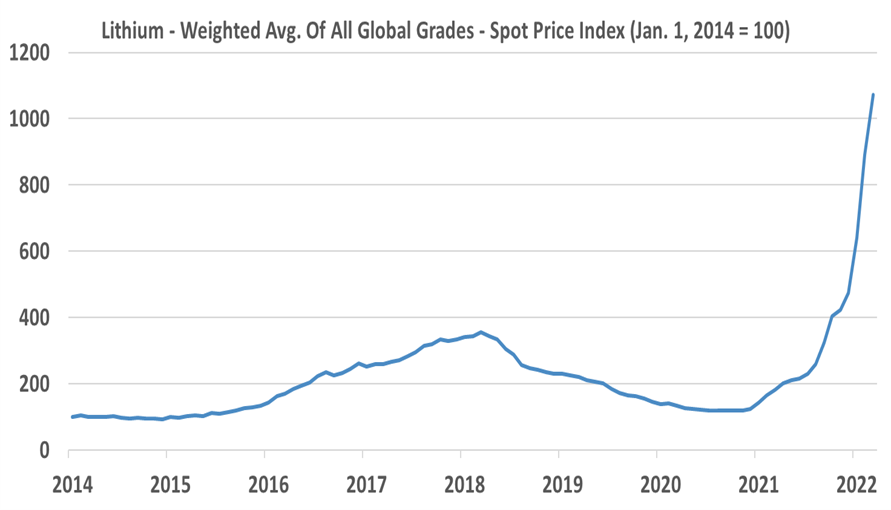

Lithium prices keep rising. We refer back to some work we did on the subject several months ago, where we predicted that lithium was likely to be a cyclical commodity - eventually. Right now we see demand for new EVs, demand to fill the supply chain for new EVs, and demand to fill the supply chain for new battery factories – and consequently, demand is likely overstated relative to the number of EVs leaving production lines. In lithium’s favor, EVs are surprising on the upside in production and sales, but this will add to the need to fill supply chains. We do not see the lithium bubble bursting soon, but we do not see enough barriers to entry for lithium to protect the product from overbuilding. There are many dilute lithium sources, and high prices could allow for some high-cost options to move up the learning curve and become future low-cost options.

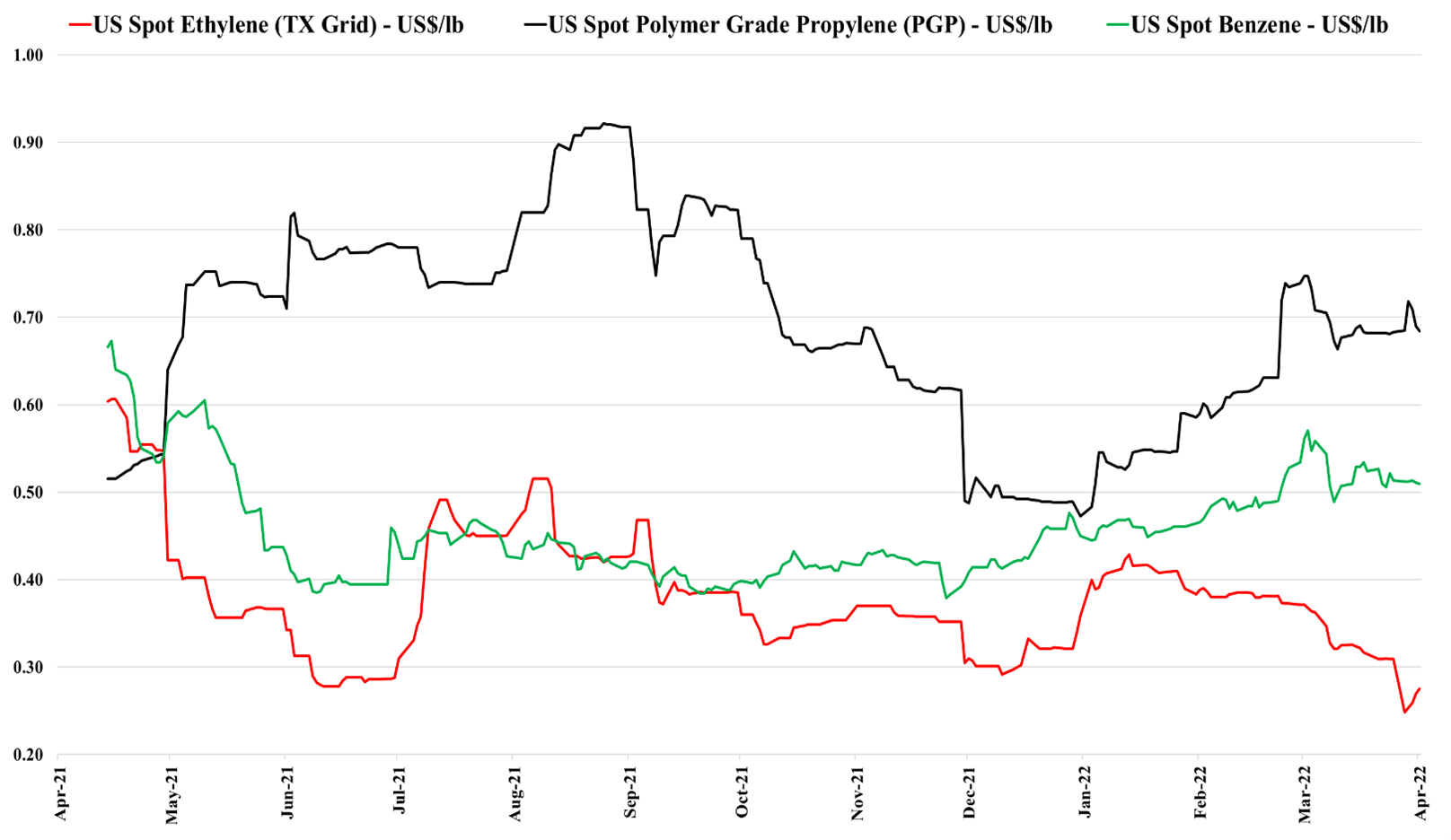

US ethylene prices have bounced off a low this week largely, in our view on the steep rise in natural gas and ethane. The drop in ethylene prices over the last couple of weeks signals an imbalance whereby production is more than enough to satisfy domestic demand and export demand. Export demand is limited by terminal capacity, and we have seen some domestic demand issues for polyethylene, not because of demand weakness, but because of export logistic bottlenecks, that are resulting in product (with homes to go to) backing up in the US ports. Given the timing of this build-up, we may see some higher end-quarter working capital from some of the chemical companies with sizeable export footprints for 1Q 2022. The sharp increase in US natural gas prices and the catch up that ethane has made to natural gas, should keep some upward pressure on spot ethylene prices if gas prices remain high. Propylene remains very supported by high propane prices.

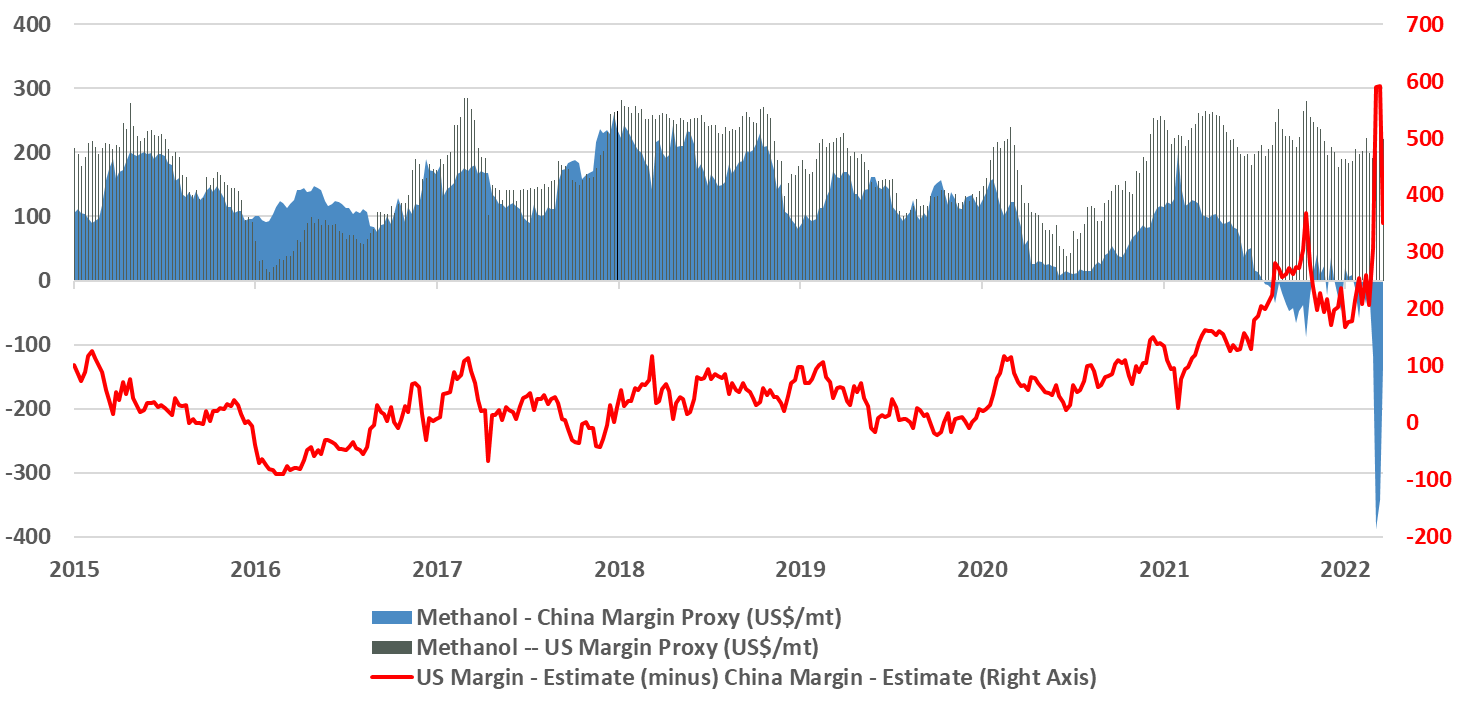

Methanol is one of a few chemicals that is directly impacted by the price of natural gas, and as the chart below shows, the pain in China (and in Europe) is extreme and it is unlikely that any facilities that require imported natural gas – or local gas with prices based on imports – are operating today. The volume and margin opportunities for those companies connected to low priced natural gas – the US, the Middle East, and other niche locations such as Trinidad, are as good as they have ever been and we are a little surprised that Methanex did not push a little harder with US pricing, given that export netbacks are likely surging. Urea and ammonia are in the same boat and prices are much higher, but the US is a net importer and international prices are directly impacting the US price.

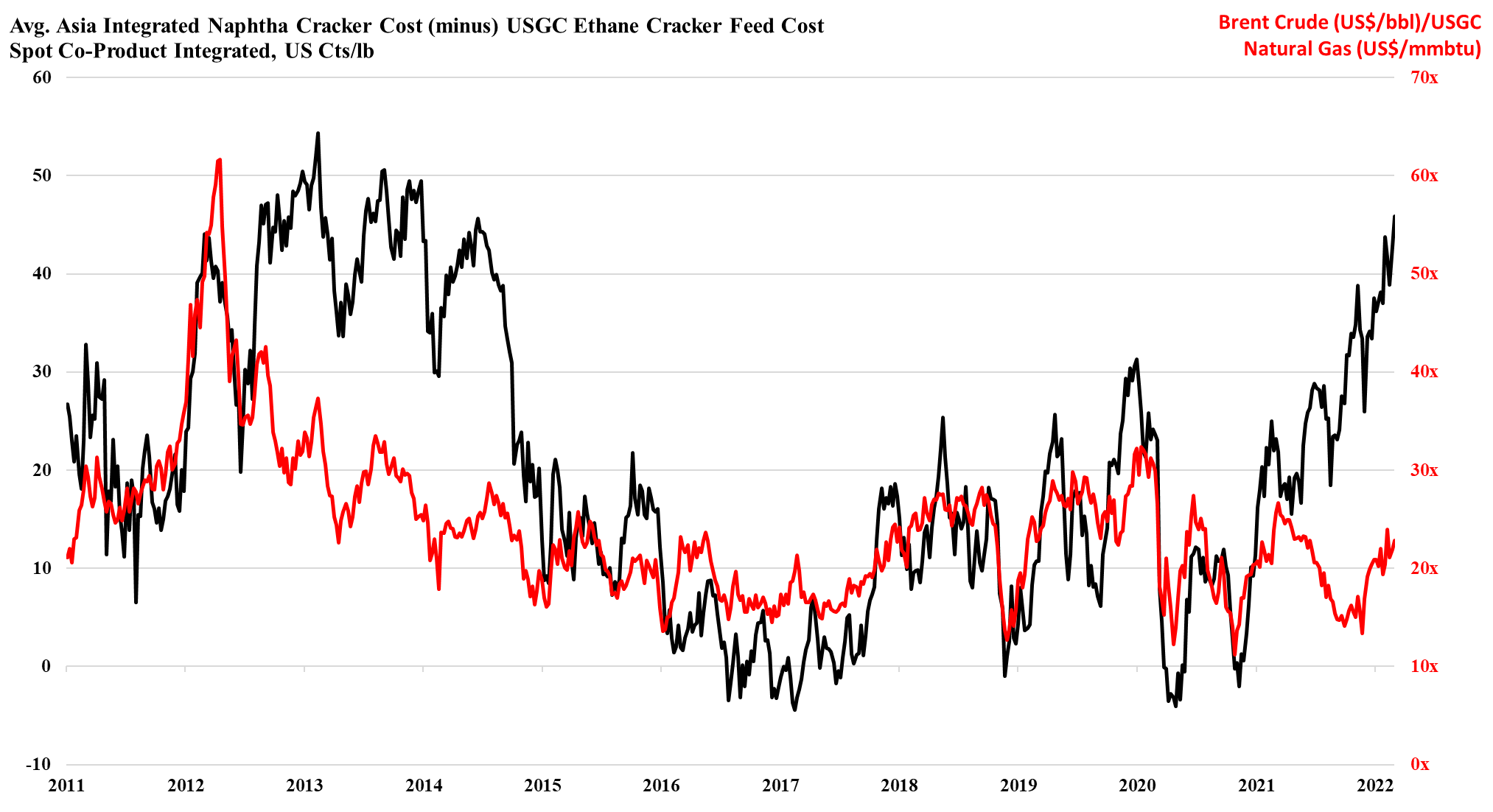

As the ratio of pricing between Brent crude and US natural gas rises, the US ethylene cost advantage is spiking, and as long as the US is producing enough natural gas to feed domestic demand and allow the LNG facilities to run at capacity, the advantage can remain. This gives the US a significant cost advantage and assuming that there is spare capacity the US industry can step up and support Europe if needed. However, it is not clear that there is much spare capacity, either in the production units or in the logistics to get the product to ports or across the Atlantic. There is a surplus of liquid and gas carriers today, but the container problems are global and the inflation and supply chain issues that we seem to be stuck with are likely to keep containers tied up in excess inventory that consumers will want to keep building as a cushion for a less certain supply outlook. The shipping issues are only part of the problem for Asia, as even with better opportunities to export, the region is seeing escalating production costs because of the movement in crude oil and naphtha pricing. We are in an unusual position where strong demand in the US is keeping domestic prices higher than in Asia, despite costs in the US that are low enough, especially for polyethylene to move material to Asia at costs well below the cost of manufacture in Asia. This dynamic can last for a lot longer in our view as long as oil prices remain elevated versus US natural gas. An abrupt turn will occur if US natural gas production falls below domestic demand and LNG demand – this would cause a spike in US natural gas prices. For more see today's daily report.

The Huntsman activist defense presentation highlighted below does a very good job of explaining why Starboard is focused on a set of concerns that the company has already addressed and while we would generally not comment on something like this, we agree with Huntsman’s assessment that the proposed Board changes bring nothing to the table. Where the Starboard activity may help is improving Huntsman’s communications, as while the company has done a good job, in our view, of repositioning, it has done a less good job, until now, of communicating what the changes mean. The presentation linked below does a much better job than anything we have seen from the company in the past. To be fairer to Huntsman, the chemical industry has always had trouble communicating strategy shifts and portfolio transformations to stakeholders and there have been several instances of good stories not turning into good businesses – Eastman had some false starts in the past but has not been alone with these problems. It often takes some time for investors to believe in a new business model and this is where good corporate communications strategies can help. This presentation is a good start for Huntsman.

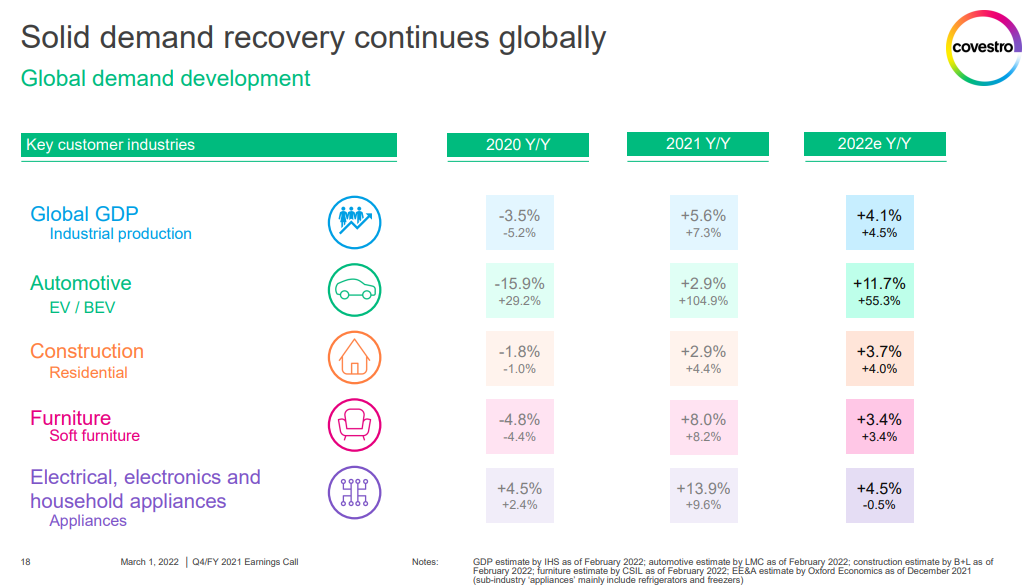

More confirmation from Covestro that global demand growth is strong, supporting reports that we have seen from most companies over the last few weeks. Some have struggled with raw material cost squeezes and either late attempts to raise prices or pricing lags in contract agreements, but almost all have pointed to very strong demand outside of auto OEM. We have questioned how much of this strong demand is inflation-driven, but it is very hard to tell as the last time we had significant inflation we did not have such an interwoven global supply chain as we have today, and consequently, it is harder to assess how much pre-buying may be going on, not because of fear of higher prices but because of fear of supply. Note that we have at least two European automakers (VW and Renault) shutting down facilities this week because they cannot key parts from Ukraine. This adds to the already problematic path for parts from China as well as the semiconductor shortage. If everyone is looking for a little bit more it would explain the very high 1Q 2022 demand that all are talking about and it likely means that inflationary pressures will continue as chemical and polymer makers try to make more, against a backdrop of higher raw materials and find it easier to increase their prices because their customers are as concerned about availability as they are prices.

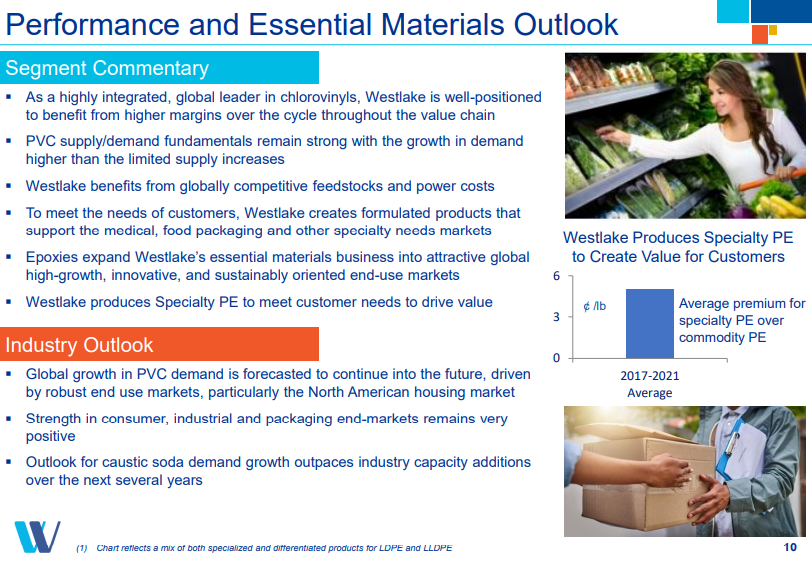

Westlake Chemical began today at a 52 week high on the back of very strong earnings but has retreated with the market. Westlake has been one of our favorite ideas since founding C-MACC in part because we believe in the diversification strategy into building products and in part because the PVC market has not seen the same level of overinvestment as polyolefins globally over the last 3 years. Westlake’s view of the housing and construction market aligns with ours and by breaking out this segment of the business Westlake should see some valuation benefit from the more stable earnings that this segment should provide. Note that the focused building products companies trade at significantly higher multiples than chemicals. We expect Westlake to get earnings and multiple boosts from here.