More earnings releases and more discussions of disruptions and higher costs! One thing that is clear from all the reports we have followed, whether from basic chemical companies or those downstream, is that no one has any expectation that the supply disruptions and inflationary drivers are going to end soon. In our Sunday Thematic, we talked about the possibility of demand remaining robust and possibly absorbing new supply in 2022 because of further inventory builds. The idea is that holding more working capital, while possibly less efficient financially, may be more prudent from a business continuity perspective, especially given the reputational risk of failing to fulfill customer orders. While there is appropriate concern that interest rates could rise significantly, lending rates are so low that the cost of holding more inventory would be immaterial for many companies. For many products in the chemical chains and across materials more broadly, global oversupply, where it exists, is not high, and a further upward swing in inventories in 2022 could easily keep tight markets tight and swing some more balanced markets to shortages.

Part of our confidence/concern that prices can continue to rise in the chemical space in general stems from what seems to be very strong demand – again confirmed in earnings reports overnight, as well as in the rail data from today's daily report, as well as inventory data that suggest we are below recent ratios to shipment trends. The inventory piece is the great unknown here because the supply chain shocks of the last 20 months will have reset expectations around “safe” levels of inventory and it is hard to judge whether the new “comfort” normal will be back to the trend in the chart or 50% higher! If the new comfort level is materially higher than in the past, demand growth will remain strong and price momentum could continue through 2022. Our expectations for a mega-cycle in basic chemicals and polymers – targeting late 2023 and 2024 could be dragged forward because of higher apparent demand the time to buy the equities could be now, on that basis.

With the linked Ashland release, we see another example of a downstream chemical maker struggling with higher input costs and general logistic constraints, and an inability to push through pricing quickly enough to avoid a margin squeeze. The opaqueness that Ashland discusses concerning some of the planning metrics for the near-term is impacting forecasts and estimates for many more companies than just Ashland but given the costs and the supply chain challenges, all are encouraged to push through pricing aggressively, and this suggests that we are far from done with the materials inflationary pressures that we have discussed at length in prior reports and the higher costs of some of these specialty chemicals will start to impact customer margins through 2022. Almost all the earnings reports that we see discuss strong end-market demand and whether this is final customer pull-through or a need to address chain inventory or both, it should support further price initiatives. For more on our inflation views see Inflation (Especially Energy Costs) – Biggest 2022 Wildcard.

Another Lesson From The Past: Costs Will Matter

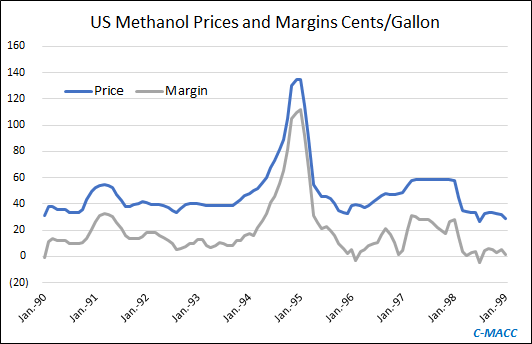

High prices are spurring behavioral changes throughout the supply chain. Per our analysis, it is causing buyers to look for alternatives and ways to use less material and increasing interest in new production, often without much thought about relative cost. In Exhibit 1 (from yesterday's report), we show the methanol peak of the mid-90s. This development resulted from supply shortages rather than high costs. It encouraged multiple projects to receive serious consideration – including methanol from wood chips – where costs looked good at the time but not on a historical basis, and as the chart shows, not on a forward basis. Most ideas never got past the planning stage. With sustainability driving a significant share of the growth investment decisions, we think several “renewable” ideas could encourage investment that rely on price premiums to keep returns attractive. While this setting might look supported today, it will likely look less tenable if traditional commodity prices retreat into a commodity trough or lower-cost competitive materials emerge.

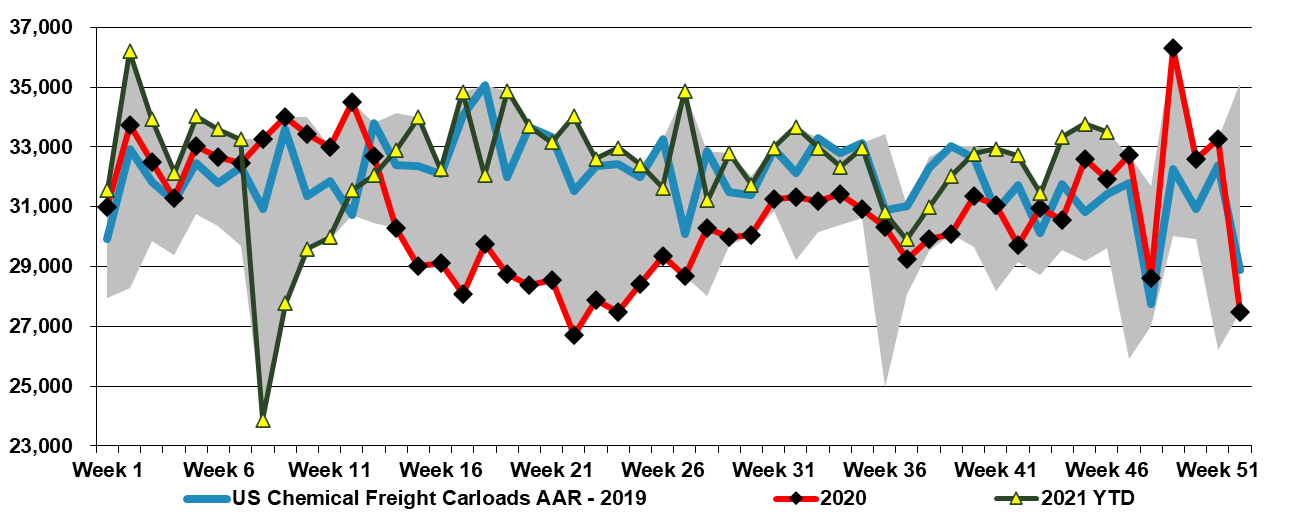

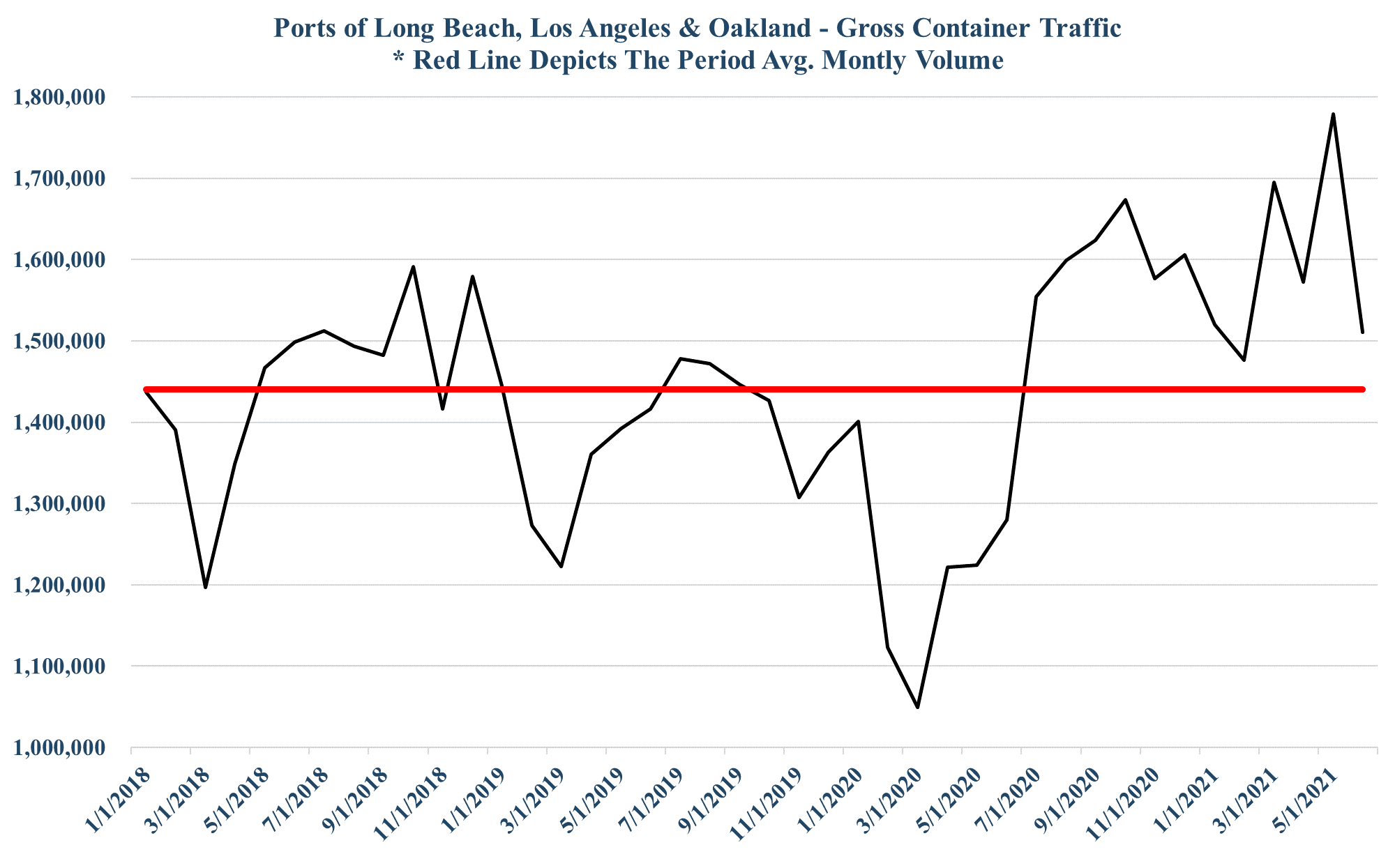

US rail data for chemicals remain at the 5-year highs and have been there for almost 2 months. This is working its way into the supply chain and we are seeing weakness in US polymer prices across the board, except for PVC. US spot polymer prices are in a bit of a “no man's land” right now as they would need to drop significantly to find incremental demand offshore, given US premiums to the rest of the world. We believe that most of the volume leaving the US is doing so within company-specific businesses – ExxonMobil supplying ExxonMobil customers, Dow supplying Dow customers, etc, and consequently, these shipments do not show up in the spot market.

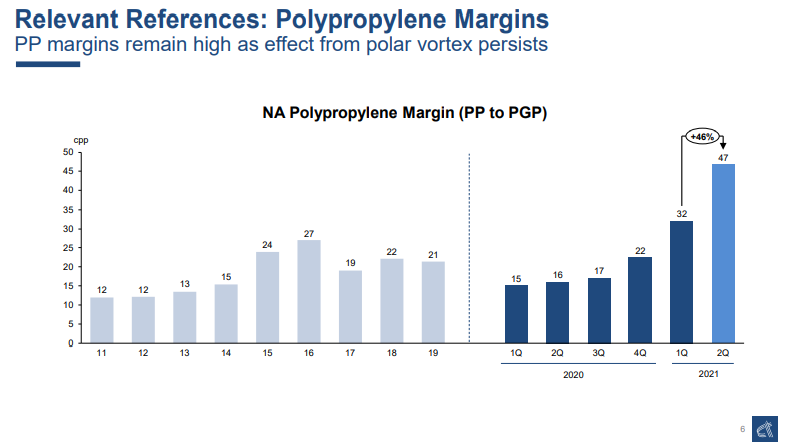

The much higher polypropylene margins in the US come despite very high propylene pricing, and the whole chain did well in the first half of the year. Demand for polypropylene has been significantly stronger than most expected year to date, although production outages have helped the market, and what we had expected to be a surplus in the US in 2021, precipitated by the Braskem start-up has turned out to be production coming online just in time and prices might have been higher still had the Braskem plant not been there. We see some of the demand as cyclical - in response to consumer durables, though there has been lower use in the auto industry because of the production cutbacks. See more in today's daily report.

We talk at length about the weather risks in the US following multiple extreme weather events during the last 12 months, but we forget that other regions are equally susceptible. Not only are there many chemical facilities on the riverways impacted by the floods in Germany but a significant volume of chemical trade takes place by barge on the rivers for both gases and liquids. We do not have an industry impact assessment for this tragedy in Germany, Belgium, and the Netherlands, but on-site flooding, especially any flooding that impacts electrics, can result in extended shutdowns for repairs, as we have seen in the past in the US.

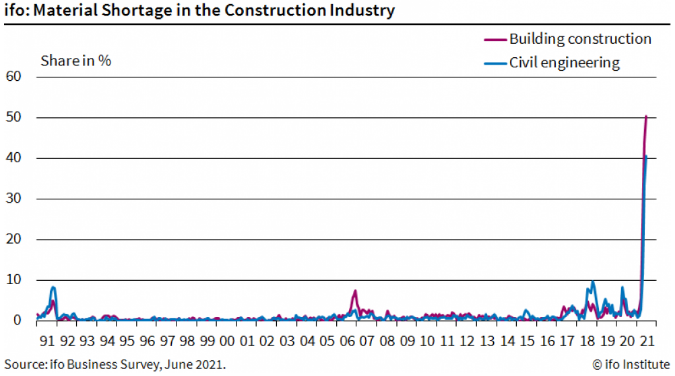

The German materials shortage chart below is certainly eye-catching. There is nothing even remotely close in 30 years of history. We see this as further confirmation that we should continue to expect high shipping rates and congested ports until surveys like this show significantly better results and it is also further supportive of inflation. While it is extremely difficult to forecast from here, we would use the pendulum or spring metaphor – the further you pull either in one direction, the further they swing or spring back. The current dislocation is so extreme that everyone in the chain is likely acting instinctively and working to find greater supply and greater supply security. At some point, both end-demand and demand to fill inventories will normalize – either back to trend or back to a higher trend, but the inventory build piece will end and we will either get a gradual retreat in the scary data – such as the spike in the chart below – or we will see an equally quick collapse, at which point pricing will likely take a hit down the chain, with basic chemicals particularly vulnerable because the world has been adding substantial new capacity over the last several years in the US and China. More investment may be needed to keep up with higher trend demand in many intermediate or end-products that consume base chemicals and this could keep pricing supported, but basic chemicals and polymers look especially vulnerable to a reversal in the supply chain build we have seen for the last 9 months. For more see today's daily report.