The Halliburton forecast of an upcycle for oil services likely needs to be put into context, as while activity should rise in the sector with higher oil and gas prices, it is unlikely that we will see a major boom. The uncertainty in the energy market, coupled with ESG pressure and borrowing constraints means that the oil industry will likely focus on its lowest hanging fruit first and may hold off on secondary opportunities completely. The oil service guys will benefit because the more productive shale wells can require longer laterals, deeper wells, and more fracking pressure, but it will likely be quality over volume when it comes to drilling activity, in keeping with what we have seen year to date.

Recent Posts

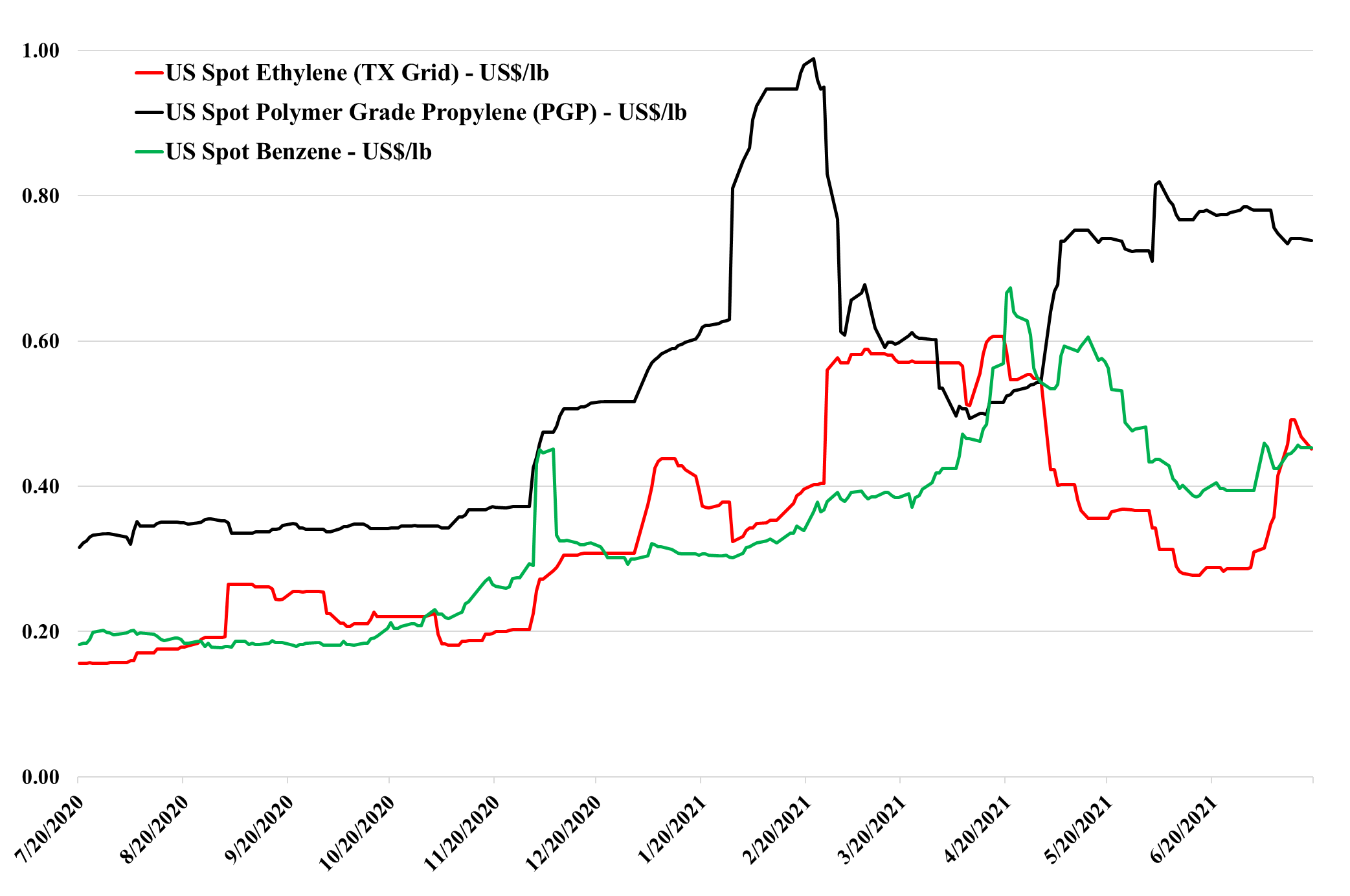

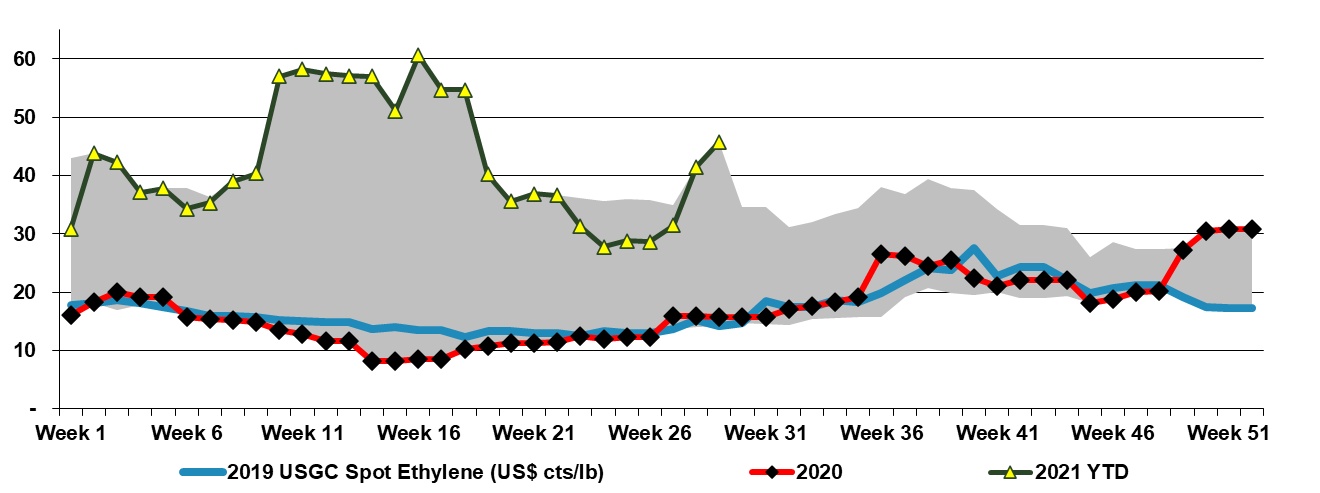

We note the volatility in ethylene in the chart below and point out that ethylene sits in a precarious no-mans-land in the US with pricing neither reflecting costs nor incremental value in use. The downside to generating buying interest in Asia is significant – more than 25% - but an incremental buyer in the US could pay much more than the current price – in many cases to meet export obligations, let alone for domestic sales. We would expect the volatility to continue, with a downside from better production rates and upside from more constraints – demand fluctuations are likely immaterial relative to the impact that supply moves could have. See more in today's daily report.

We talk at length about the weather risks in the US following multiple extreme weather events during the last 12 months, but we forget that other regions are equally susceptible. Not only are there many chemical facilities on the riverways impacted by the floods in Germany but a significant volume of chemical trade takes place by barge on the rivers for both gases and liquids. We do not have an industry impact assessment for this tragedy in Germany, Belgium, and the Netherlands, but on-site flooding, especially any flooding that impacts electrics, can result in extended shutdowns for repairs, as we have seen in the past in the US.

Regional PVC price movements are interesting as the World is trying to find balance. Incremental ethylene and chlorine economics in Asia pushed the local spot prices for EDC so low as to shut out US EDC exports – the net result has been more PVC production in the US and a decline in US spot prices. While it is likely that the Asia incremental pricing will improve as some sellers will be losing money and may need to cut back rates, the US will not enjoy a better export market without the acceptance of much lower netbacks, which will maintain negative pressure on domestic prices. That said, PVC is very levered to economic, construction, and housing investment in Asia and there is likely some pent-up COVID-related demand in the region – the oversupplied market may not last for long. We still see a better medium-term outlook for PVC than for other major polymers. There's more detail and coverage on today's daily report linked here.

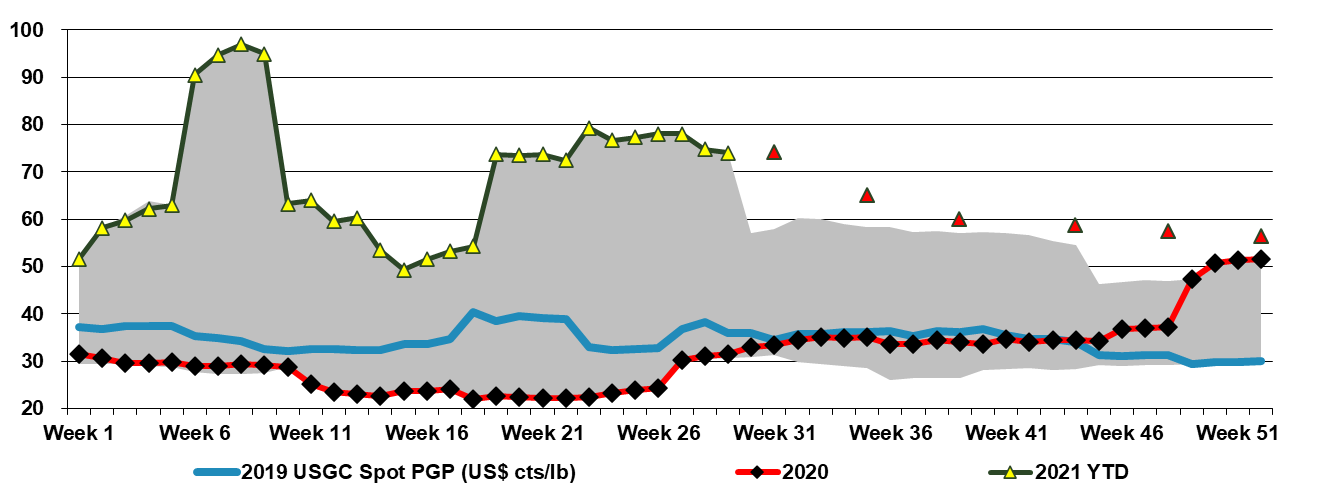

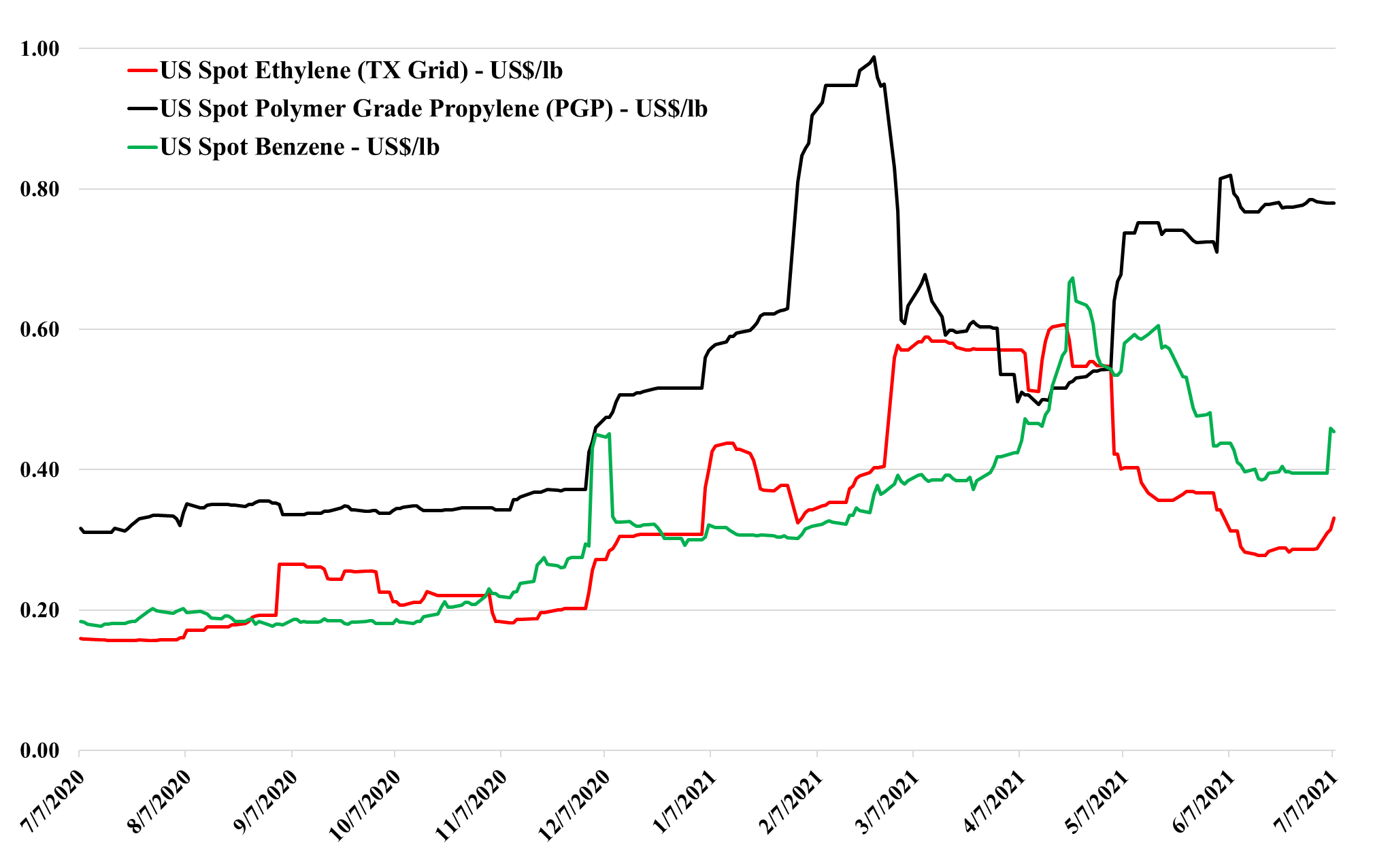

Polymer grade propylene in the US is weakening, albeit slowly, but remains very high versus history, versus ethylene and incremental costs of production. Propylene has the same volatile dynamic that ethylene has today in that if short, consumers can pay a lot more, and if long the price was a long way down to reach any cost hurdle. Just like ethylene we expect the market to show meaningful volatility in 3Q 2021 unless we get a storm effect in the US that impacts production more than demand. The futures market for propane and propylene expects propylene to fall relative to propane and barring weather events this is probably a reasonable view. See more in today's daily report.

Spot prices for ethylene have surged in the US in the last week (chart below) – especially for delivery to Louisiana, where Westlake has a production outage. The price increase has completely removed the brief export arbitrage to Asia that lasted for a few weeks in late May and early June (Exhibit 5 in today's daily report). As we discussed on Sunday, ethylene is in a very wide no-mans-land in the US as it is not in sufficient surplus to drive pricing down to costs, and would likely be supported well above US costs and more by Asia costs in the current market, but if the market becomes short, buyers can pay a lot more for it as derivative prices are so high. If a PVC producer, such as Westlake, is buying, they can afford to pay significant premiums given that ethylene is less than 50% of the PVC molecule.

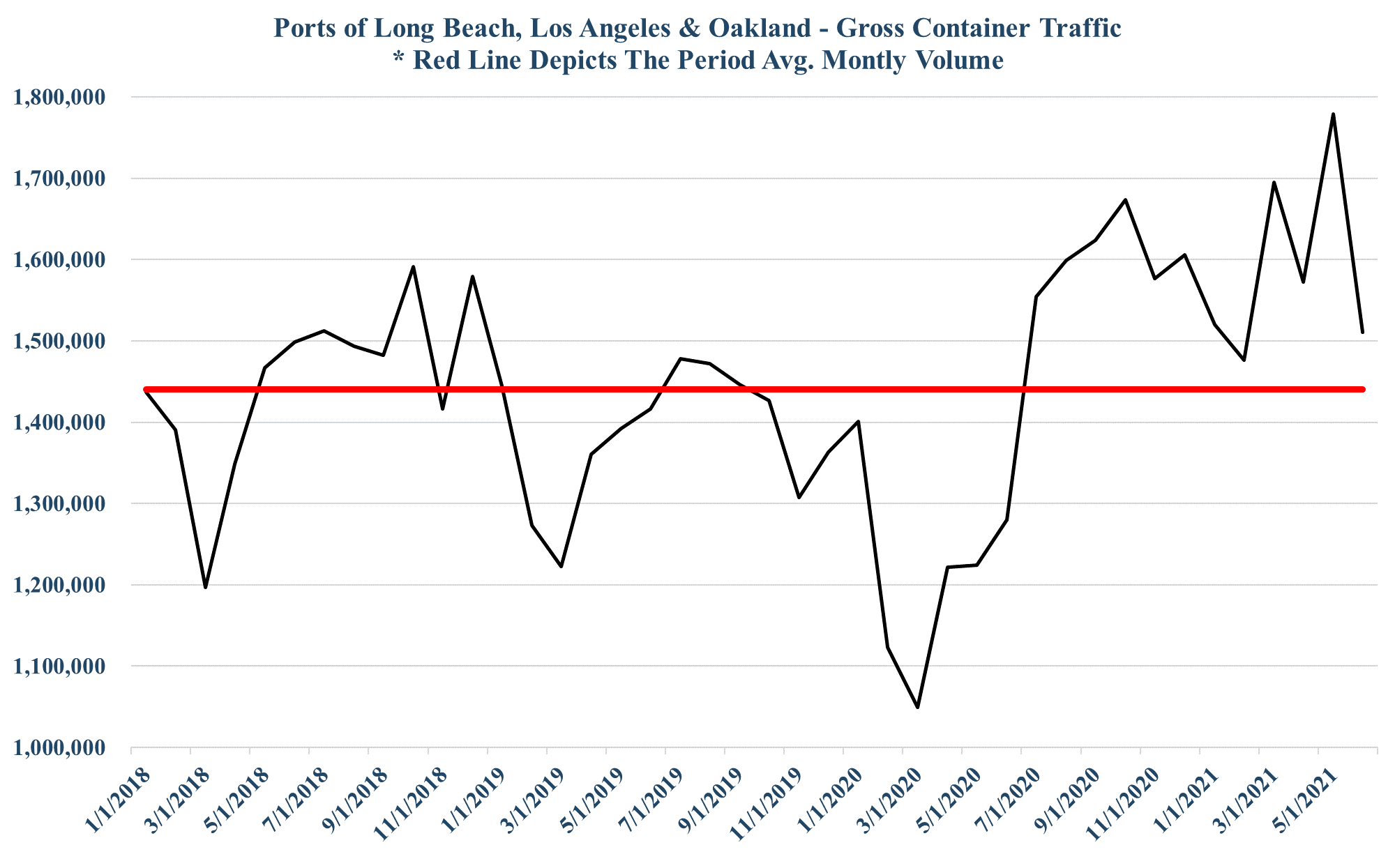

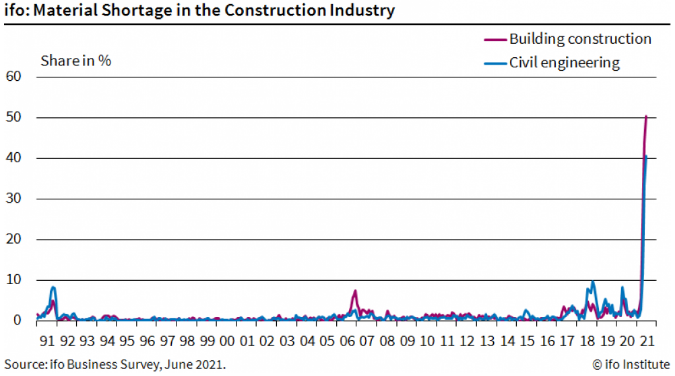

The German materials shortage chart below is certainly eye-catching. There is nothing even remotely close in 30 years of history. We see this as further confirmation that we should continue to expect high shipping rates and congested ports until surveys like this show significantly better results and it is also further supportive of inflation. While it is extremely difficult to forecast from here, we would use the pendulum or spring metaphor – the further you pull either in one direction, the further they swing or spring back. The current dislocation is so extreme that everyone in the chain is likely acting instinctively and working to find greater supply and greater supply security. At some point, both end-demand and demand to fill inventories will normalize – either back to trend or back to a higher trend, but the inventory build piece will end and we will either get a gradual retreat in the scary data – such as the spike in the chart below – or we will see an equally quick collapse, at which point pricing will likely take a hit down the chain, with basic chemicals particularly vulnerable because the world has been adding substantial new capacity over the last several years in the US and China. More investment may be needed to keep up with higher trend demand in many intermediate or end-products that consume base chemicals and this could keep pricing supported, but basic chemicals and polymers look especially vulnerable to a reversal in the supply chain build we have seen for the last 9 months. For more see today's daily report.

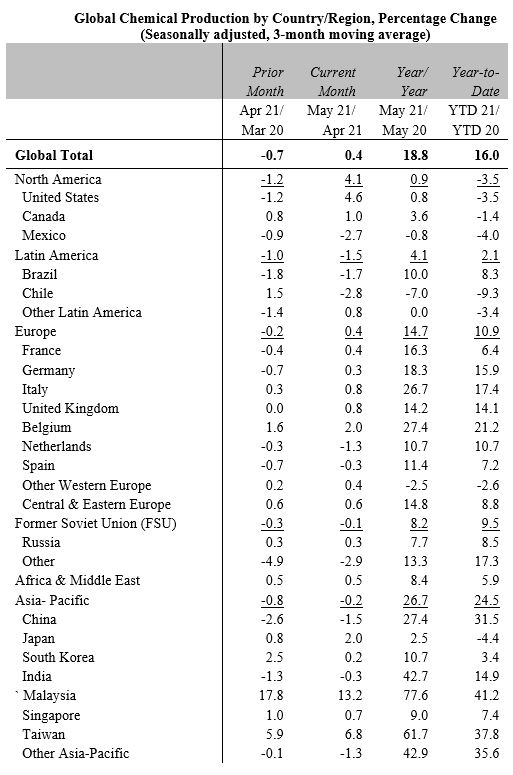

The ACC May production data shows the very strong year on year production growth globally, with the US gains more muted than the rest of the world as the COVID production impact in May of 2020 was less severe in the US than in many other parts of the world, and the China growth has been further assisted by significant capacity additions since this time last year. It is interesting to note that on a year to date basis the US is still down year-on-year, which is the lingering impact of the winter storm on production and it reflects that there is not much space capacity in the US, given both the strong demand and the export economic advantage of lower feedstock costs. Despite the collapse in prices in Asia – very well reflected in Exhibit 1 in today's daily report – the US has enough margin to continue its derivative and ethylene exports.

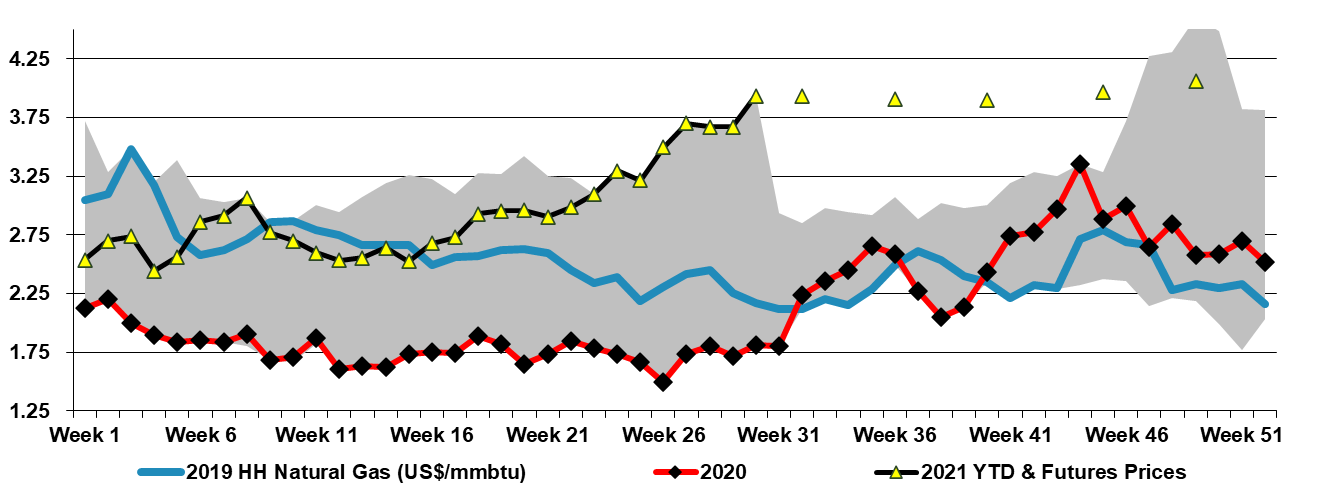

The US ethylene market strengthened slightly in early July, most likely because of supply disruptions as it is hard to see how domestic demand could improve from here. There is not much room to increase prices further if the export market is the balancing mechanism through July and August, as prices remain depressed in Asia and any arbitrage would close quickly if prices in the US moved any higher. Despite the rising NGL prices discussed in today's daily report and on Sunday, the US has plenty of margin left in ethylene, and prices could go lower if that is necessary to move additional volume. While we talk in the opening paragraph about increased inventories of finished goods in anticipation of the year-end holiday season and continued supply constraints, and how this is leading to a shortage of warehouse space, we suspect that everyone upstream of the finished good suppliers is also looking at adding or maintaining a larger inventory cushion than they have in recent years. We still believe that it is a tough call today as to whether you should sell surplus ethylene or store it as we head into hurricane season in the US.

We think the India styrene plan is ill-advised. The styrene market has had a brief moment in the sun over the last couple of years, but we believe that it has another leg down ahead, based on the recycling complications of polystyrene versus other packaging polymers. New capacity in China and likely weaker demand in the US and Europe should push the global market into oversupply for a prolonged period (if not permanently). This is bad news for styrene (or polystyrene) producers but very good news for the non-integrated producers of styrene derivatives targeting the durables markets – such as Kraton.