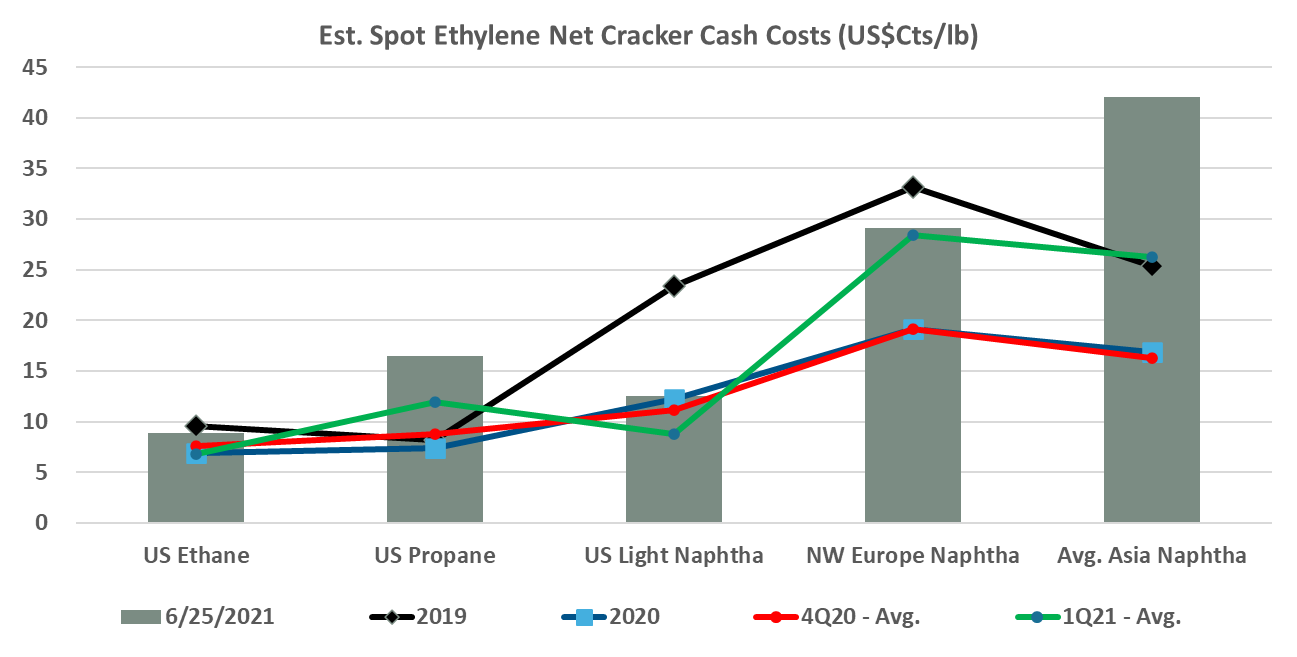

The chart below focus on the ethylene cost curve and show that the US currently retains a distinct cost advantage despite escalating domestic feedstock costs. The current cost advantage in the US is sufficient to move ethylene derivatives into most markets profitably and while US spot prices for ethylene may not quite reflect the levels needed to stimulate exports today – US ethylene costs certainly do. The restart of the Nova unit in Louisiana may put some further downward on US ethylene prices but as we discussed yesterday, given the weather risks in 3Q it is an interesting dilemma today over whether you sell surplus ethylene or store it on the basis that spot prices will rise because of production outages – this time last year the “store it” decision would have been the right one as spot prices rose through 3Q.

Recent Posts

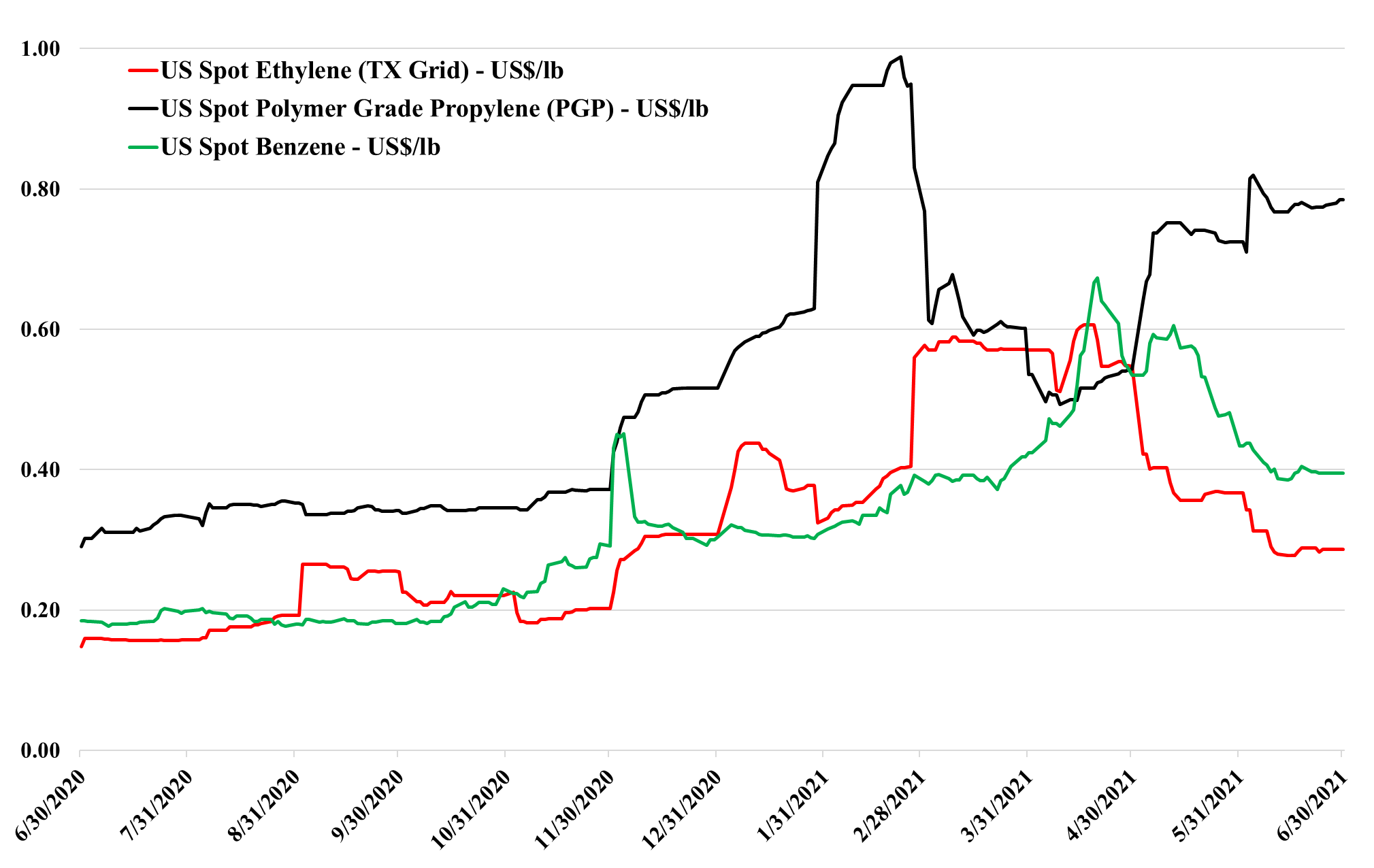

The higher ethane prices and the sharp increase in 2Q is likely offering some support for ethylene, but the more likely leveling factor of the last week or so has been the Nova outage and any lost production at Westlake, which will have a direct impact on export availability. Until ethylene spot prices in the US approach costs, which are around 10 cents per pound based on ethane feed, the more important driver of pricing will be whether or not there is a surplus and if there is what price is needed to generate export demand. The US ethylene surplus is equivalent to a couple of large plants and consequently, the market can swing from short to long depending on who is operating and is very vulnerable to weather-related closures, although these often take down ethylene derivative plants as well, creating shortages of the derivatives. Polyethylene can afford to pay more than y twice the current price of ethylene, while the ethylene export market needs a further step down from here. Consequently, the range of potential volatility in 3Q is very high – we underestimated the weather impact last year, as did everyone else and it would be a tough call today for a producer with a surplus as to whether to push it into the export market or hold on to it. See more in today's Daily Report.

The Air Liquide announcement linked is consistent with the widely held view that semiconductor markets desperately need new capacity and shows that existing China-based manufacturers are stepping up. Air Liquide will supply new capacity in Wuhan, where it has been an active producer of high purity gases for the semiconductor industry for decades. While this is likely a sound investment for Air Liquide, backed by strong “take or pay” agreements from customers, the risk to the expansion is that while the world is in dire need of new semiconductor capacity, it is unclear how much of that need is for more China-based production. There is significant semiconductor demand in China and that demand will continue to grow, but consumers in the West are not only looking for more semiconductor supply but also more semiconductor supply security, and with the concentration of production in China and Taiwan, supply from outside the region is more desirable. We see new semiconductor capacity announced for the US and the auto industry, in particular, is calling for more diversity of supply, not just for semi’s but also for other EV components, especially batteries. There is already anecdotal evidence of a preference for non-China-based materials – all the way back to lithium - but how much more US and European producers are willing to pay for this “preference” will dictate the ultimate level of spending. Despite these concerns and absent broader geopolitical risk, this is likely a relatively safe project for Air Liquide and the capital commitment is not going to break the bank.

The LG Chem announcement may be a hollow victory for a while, and we would use the analogy of being the “best-looking horse in a glue factory”, given the weakness in the Asia ethylene and derivative markets right now. In this case, being the biggest means you lose the most in a down-cycle (see chart below and more on today's daily report). The significant capacity adds in China have collided with lower than anticipated demand growth, and driven prices down to costs (or below in the case of polyethylene in China). However, one thing we have learned over the last few decades is that you should never underestimate China’s ability to grow its way out of oversupply, and to assume that the surplus in Asia is here for the long-term is probably wrong. However, it could last a year or so and this is very unfortunate for LG Chem as making a loss in your first year of operation is very hard to come back from when looking at the project on a DCF basis.

Source: Bloomberg, C-MACC Analysis, June 2021

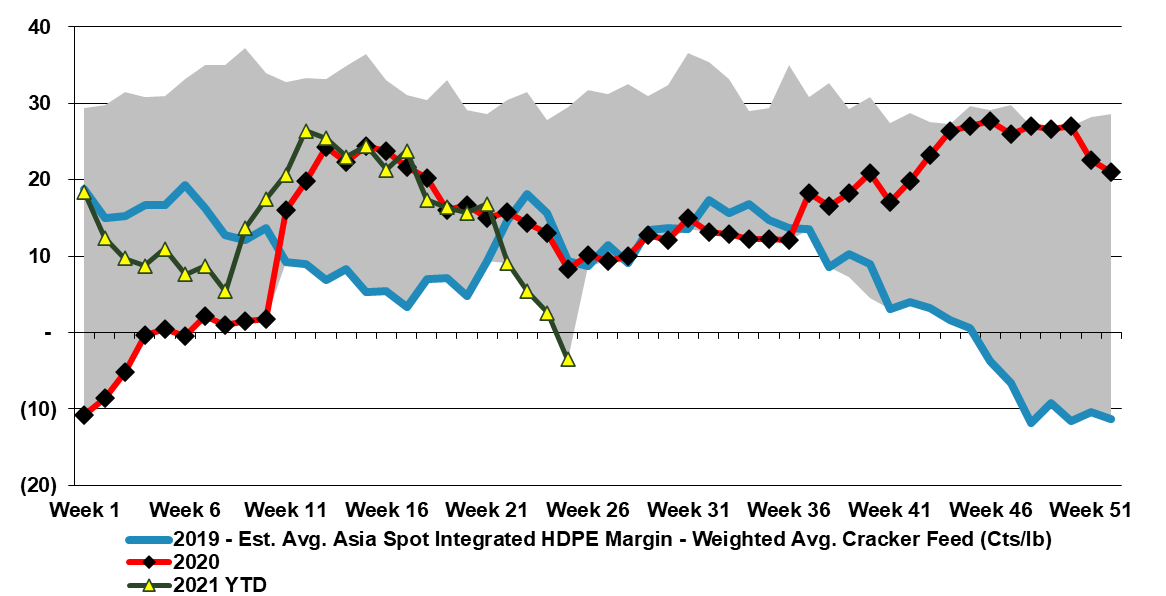

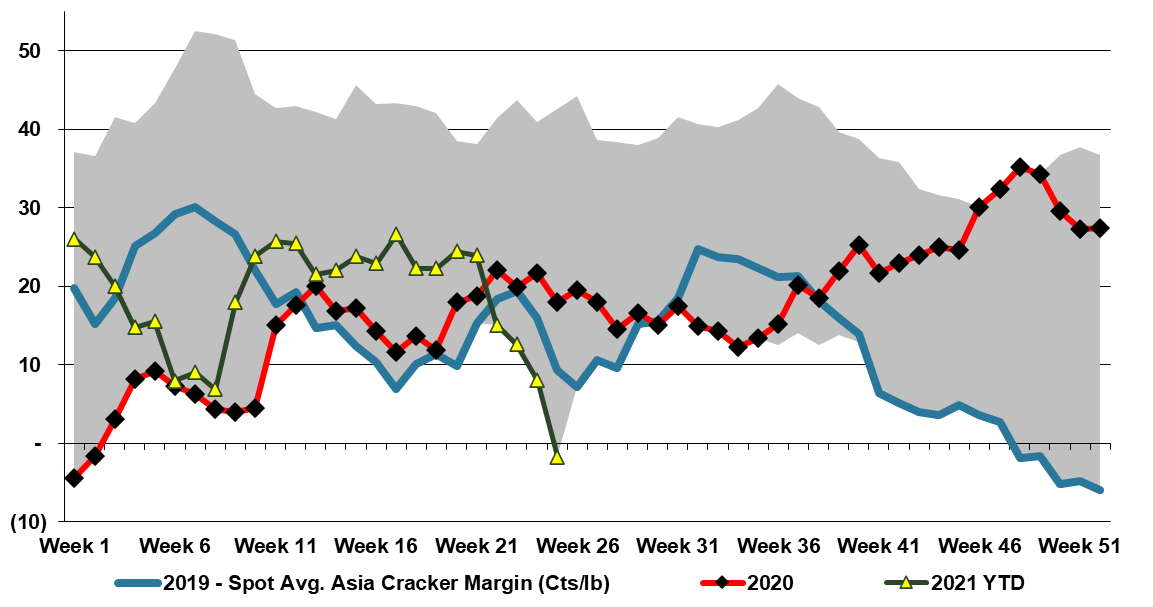

The charts below focus on ethylene and the significant decline in Asia prices, now to levels that suggest negative cash margins. While we may see some cutbacks in production, especially if ethylene from the US can be secured at prices that are even lower than we see in Asia today, most producers will run until they cannot cover variable costs, and given that some of the imbalance, in China especially, might be short term in nature, it is unlikely that we will see any drastic production decisions yet. While the capacity additions in China have been extreme, demand is subdued domestically as consumer spending has not returned to its pre-pandemic trend and the shipping and port problems are hindering export demand.

The Baystar polyethylene start-up date is consistent with the guidance that the company has been providing for a while, but it still leaves the venture with an ethylene surplus until that time and while the ethylene has been placed, according to the company, the ethylene that it has displaced will likely keep some downward pressure on US ethylene pricing until the polymer plant starts up (all things being equal). Even when the polymer plant starts, the US is expected to have a net ethylene surplus and we would expect exports to continue and prices to reflect levels to make the exports possible.

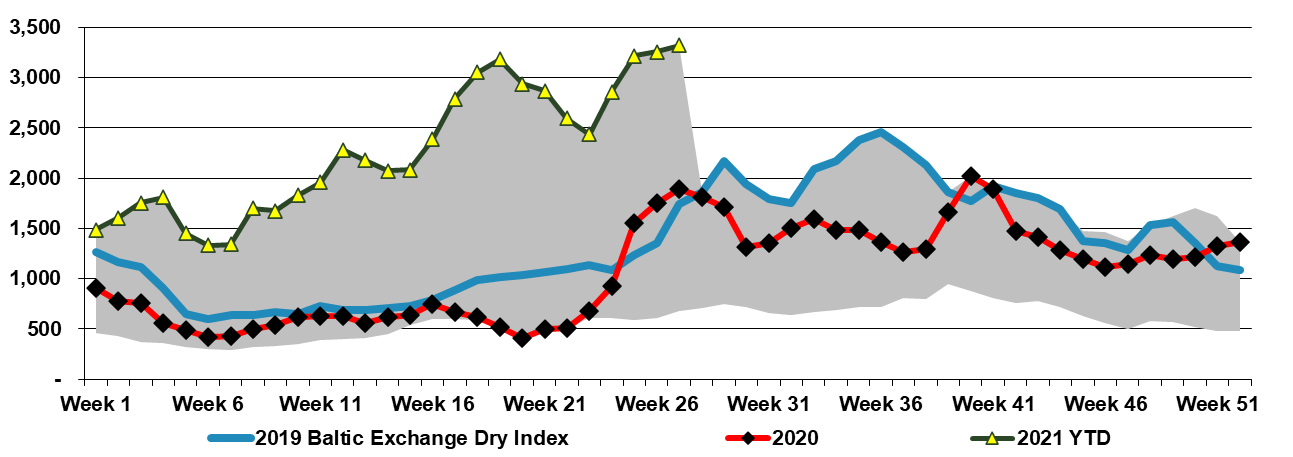

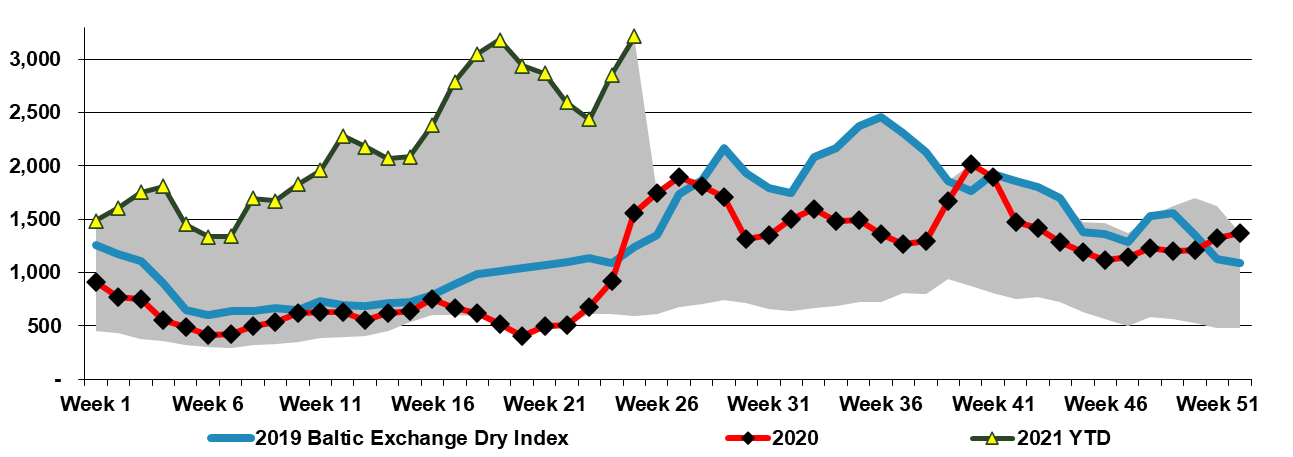

See today's daily for more on this, but while the freight rate moves are more than likely going to correct to a degree at some point, their continual escalation has multiple implications for the chemical and plastic industry as they are most impactful on cheap imports from Asia targeting low-cost furniture, appliances, toys, and household goods where the base cost of the product is low and the move from $3,000 to $10,000 per container wipes out any advantage of manufacturing offshore.

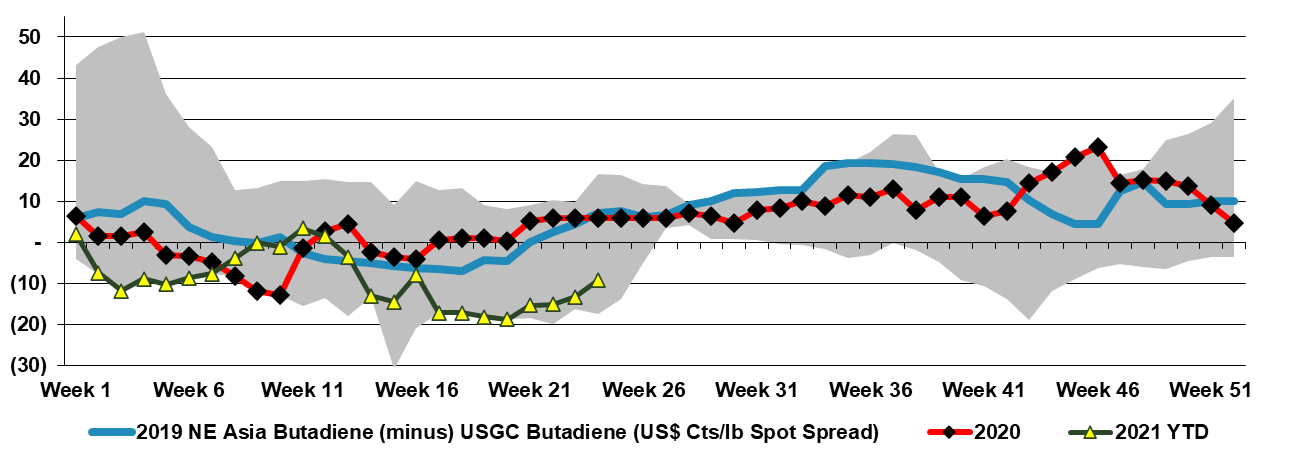

The exhibit below looks at the difference between a strong butadiene market in the US and a much weaker one in Asia. The strength in the US is a function of the stronger US economy and consumer spending as well as logistic issues with products containing butadiene derivatives, but also because there is no incentive to increase heavier cracker feedstock use right now in the US and consequently co-product butadiene supply remains constrained.

The commentary on oil reflects the opposing views that OPEC+ capacity is looming and that every piece of incremental negative demand news is frightening, versus that OPEC+ is disciplined and wants higher prices, resulting in every incremental positive being welcomed. We are firmly on the side of higher oil prices as we cannot see any stakeholder in oil wanting anything except opportunity profits for as long as it may last from here.

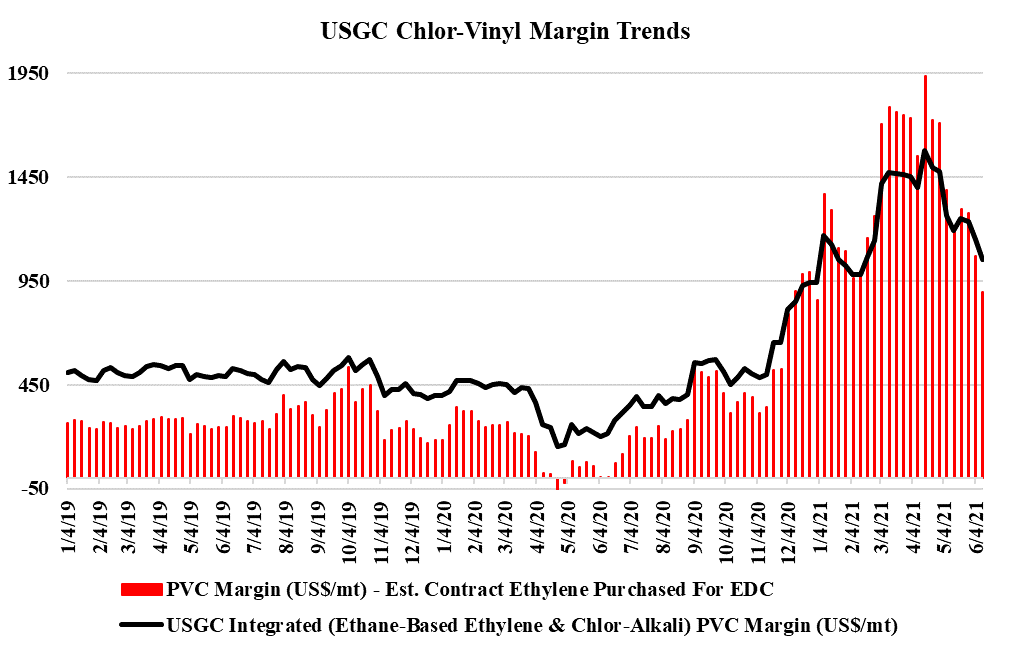

PVC margins are off their highs, as pricing is falling through June. The building product markets remain robust in our view, albeit off their highs, and some of the strength in PVC in April and May was a consequence of production shortages caused by the winter freeze in February. While PVC may be falling faster than polyethylene today, we see support for US PVC at higher prices and margins than for polyethylene in a weaker market unless oil climbs further relative to US ethane. See more on our daily report.