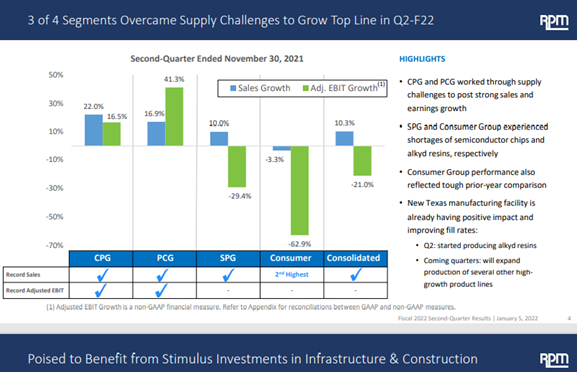

Following on again with our inflation theme, which features heavily in today's Daily Report, note that RPM’s release is riddled with references to inflation impacting results negatively as raw material and logistic costs increased. The commodity chemical and polymer producers have much more pricing flexibility than the specialty makers like RPM, and they can generally pass through higher costs quite quickly. For the specialty companies, there is generally a lag, as is clearly shown in RPM’s results, but they generally catch up with pricing as long as demand is robust, which it appears to be. The benefit for the specialty companies is that they can often hold on to price increases or at least some of the increase longer than a commodity producer can as raw materials and fundamentals ease. We expect the intermediate and specialty chemical producers in the US and Europe to have strong demand growth in 2022, as the reshoring momentum should continue and offset any risk of weaker consumer spending on durables as the year progresses. We have been more focused on companies that are selling materials into construction and renewable energy and EV markets, but RPM has enough exposure that it should also be a beneficiary as long as prices can keep pace with costs.

Recent Posts

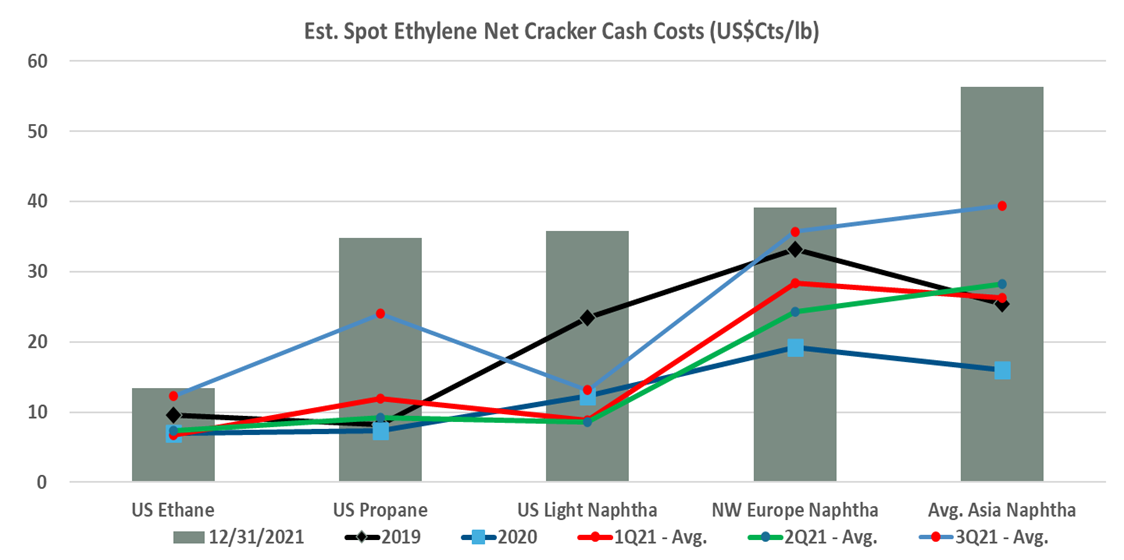

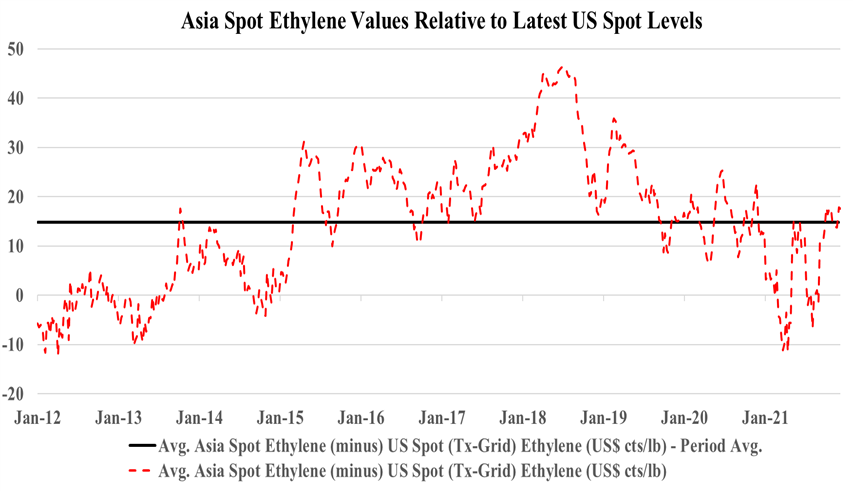

Given the higher prices of natural gas in the US, the shape of the current cost curve for ethylene in the exhibit below goes very much against traditional thinking and anyone looking at a historic crude oil to natural gas ratio as a proxy for the US competitive edge would be underestimating the advantage today. The major factor driving the change is the oversupply of ethylene co-products and their derivatives in Asia following a wave of new capacity in China and relatively lackluster growth locally during the Pandemic. As China and the region swung from net-short propylene and butadiene derivative markets to net-long, the price of derivatives declined and the price of the underlying monomers also fell – note that in our Daily Report today we show very positive margins for ethane based ethylene in the US and naphtha based margins in Europe, but negative margins in Asia and on top of that positive polyethylene margins in the US versus more break-even in Europe and negative in Asia. The exception in Asia is low-density polyethylene where there is extremely strong growth for solar panels, both for domestic markets and also for export.

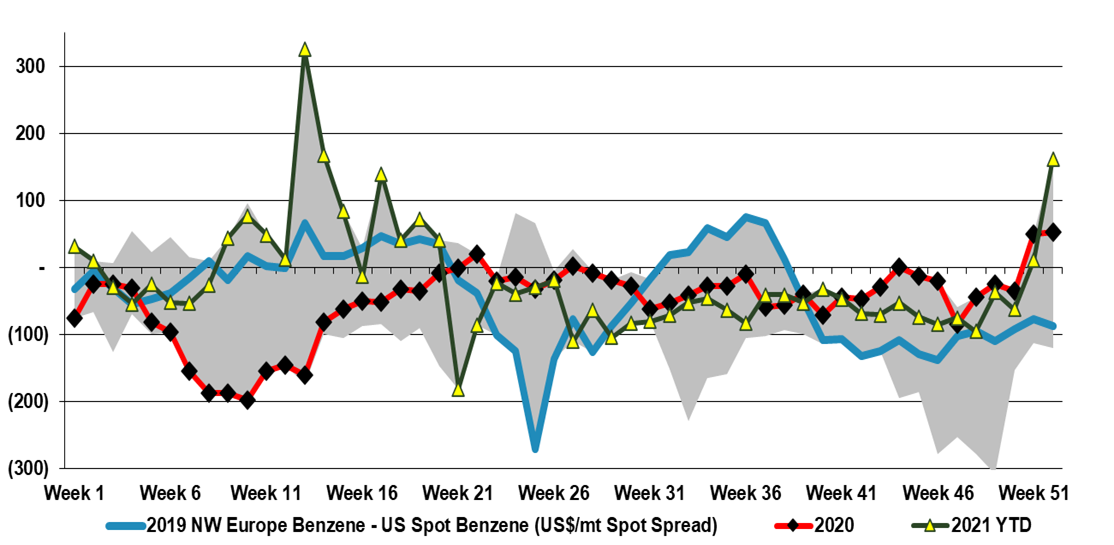

The surge in European benzene pricing (first chart below) is likely a function of lower production as refiners adjust to account for the new COVID restrictions in the region, lowering short-term demand for jet fuel and gasoline. Prices in Europe are high enough today to justify shipments from the US but are more likely to result in shipments that were bound for the US heading to Europe instead. By contrast, US refining rates are edging higher, as the holiday season has created more demand for air travel and gasoline, despite the rise in COVID.

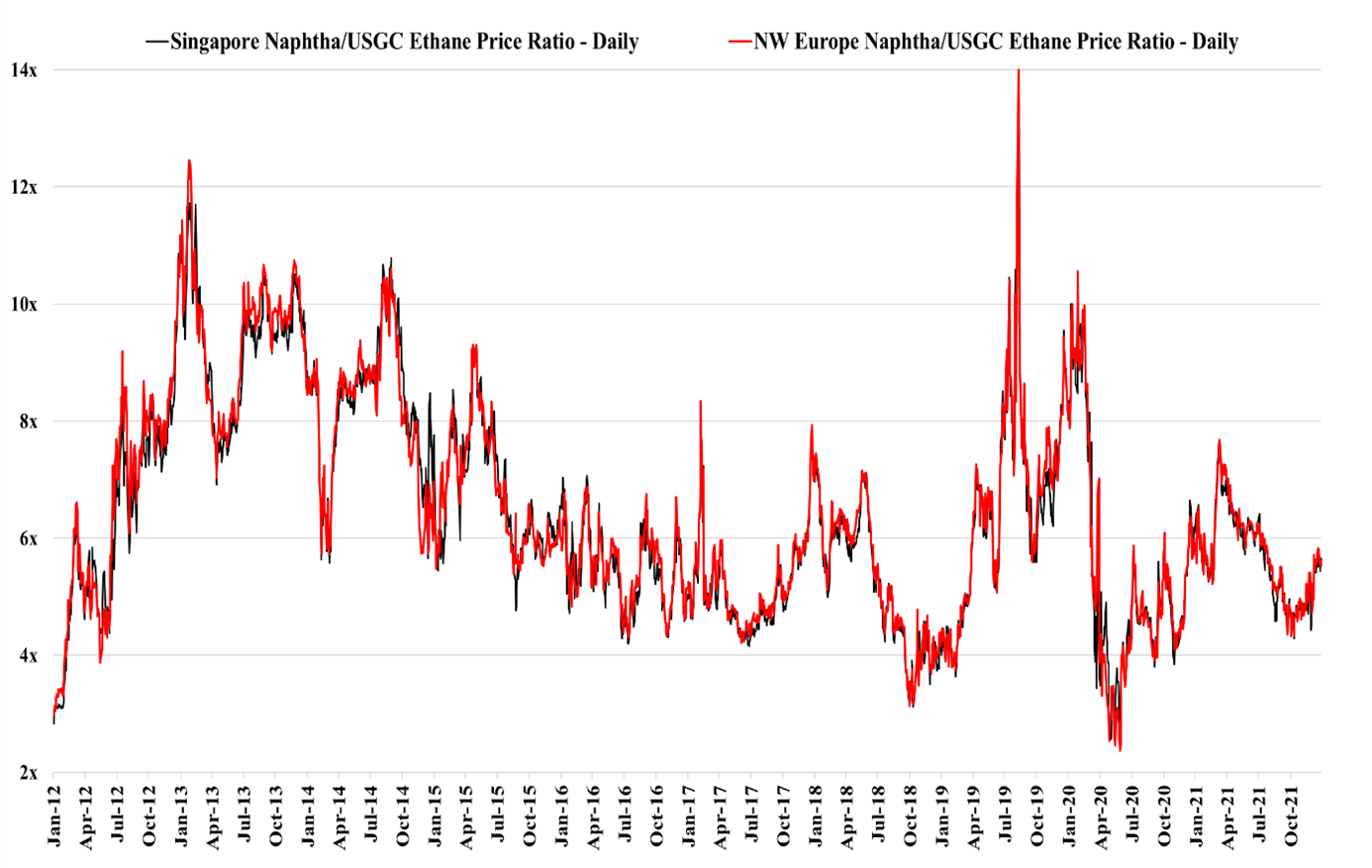

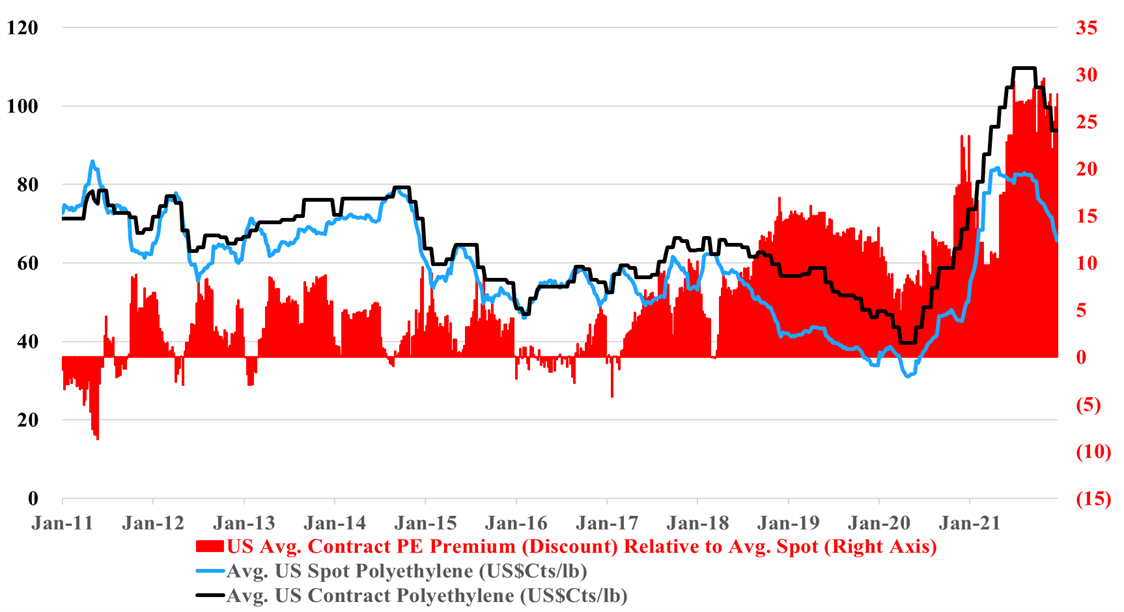

Looking at the exhibit below, it is clear that planning for consumers of hydrocarbon feedstocks is a challenge, and this is especially true for anyone looking at new projects, adding to our view that new project announcements will slow in basic chemicals, setting up for a major upcycle after 2023. The volatility in relative feedstock prices over the last ten years likely means that you would need to be able to demonstrate profitability under a wide range of possible feedstock price scenarios, while at the same time assuming that prices are set by marginal costs. Today global prices are set by marginal costs as parts of Asia are operating at break-even economics, with the much more profitable US and Europe impacted by feedstock advantages in the US and higher freight costs for polymers trying to enter the US and European markets. The US trade balance discussed in today's Daily is partly influenced by rising prices on some imported goods because of higher freight costs. While we continue to see some basic chemical expansion announcements, there have been periods of relative feedstock costs over the last 10 years where any project would have looked unprofitable. The volatility in the chart confirms that any producer will have better and worse times throughout a facility’s operating life, and consequently, start-up timing can be everything. Losing money for the first few years of any project’s life can destroy any ROI goals.

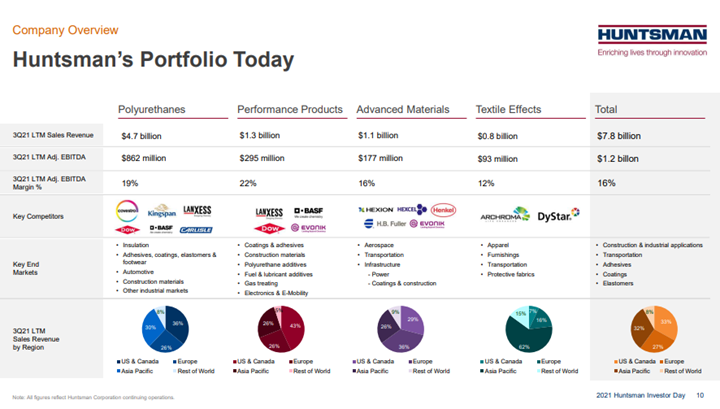

We want to focus on the Huntsman strategic review of its Textile Effects business today, but in the context of the proposed management compensation program that was also discussed in today's release. If you are going to use total shareholder return (TSR) as a key factor in executive and senior management compensation (which is aligned with shareholder goals), then it must also be core to your corporate strategy. Every action or proposed action should be looked at through the lens of how it will align with the core strategic goal. Hunstman may be doing the right thing by looking to sell its Textile Effects business because it has a lower EBITDA margin than other businesses in the portfolio, but is this necessarily what a shareholder is looking for? In our experience, shareholders pay more for earnings certainly – so lack of volatility – and growth. Margins are important but margin improvement is only important if it impacts growth. Margins can be improved through divestment, but unless the divestment increases earnings certainty, and/or the growth rate of the remaining business, the divestment may have limited impact. That said, Huntsman is thinking about this correctly, and has been active in transforming its portfolio in the past – some might say too active – but we would not be in that camp. Compare this story with LyondellBasell, which has had the TSR component in its compensation scheme for years, but has not – in our view – managed the portfolio with that in mind. Acquisition and capital spending programs have in theory added to core EBITDA (not the case for the Bora JV in China today), but they have not done anything to address volatility, and investors are rightly questioning the cost of the growth – given the increased debt load. If LyondellBasell management was truly focused on TSR, the company should separate its much higher value compounding and licensing business from the core. See our past work on LyondellBasell

The negative momentum in US polymers prices is overwhelming all other factors in the eyes of public shareholders, with Dow and LyondellBasell share prices both down 6% since October 1st, underperforming the S&P500 by 16%. The data in our Daily Report and the exhibit below show that current industry profitability is very high and much higher than it was in 2019 when share prices were roughly where they are now. Our expectation is for profits to fall in 2022, but not to the levels seen in 2019 unless there is a significant increase in US natural gas and NGL pricing relative to crude oil (which is possible). But while these stocks look very attractive based on historic relationships to cash flow, we cannot ignore years of experience covering this sector which says that no one gets interested until the earnings revisions bottom out - so not yet, and likely not in 1H 2022. Complicating the story is the lack of clarity around what sort of EGS penalty is implied in current valuations and whether it could get worse as ESG funds grow, which they surely will in 2022. In our ESG and Climate report tomorrow we will look at some chemical stocks that could benefit from the rise in energy transition and infrastructure spending in 2022 and are less exposed to commodity polymer global oversupply.

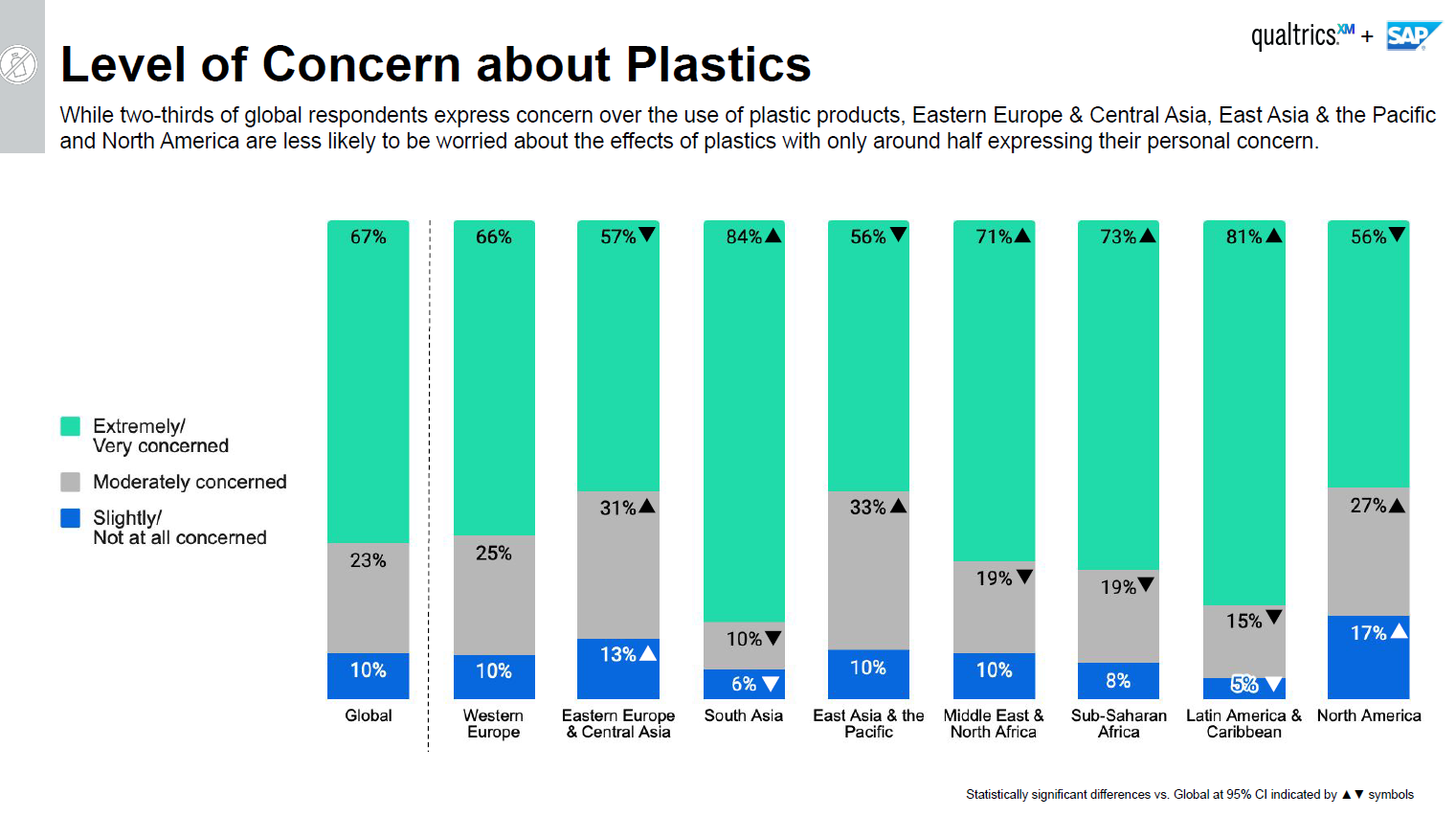

The linked headline is interesting and accurate, but the “civilian” education around plastics has just begun – and will need to be continuing education. Plus, the agenda for plastics producers likely changed with COP26. On the first point, while consumers have been made more aware of plastic waste issues and recycling in 2021, it is still very mixed by geography, with some countries and some US states making major pushes in 2021 while others have lagged. There remains a significant level of skepticism and disinterest in recycling in the US as we discussed in a recent ESG and Climate report – linked here (See chart below). The continuing education comment is based on the likely significant evolution of plastics over the next ten years. If we introduce more biodegradable polymers into the mix, these will have to be dealt with differently by consumers. Also, as packagers move towards more “recyclable” packaging, more materials will move from a waste stream to a chemically recyclable stream and ultimately to a mechanically recyclable stream – as this evolves, consumers will need constant updates is they are expected to play a part.

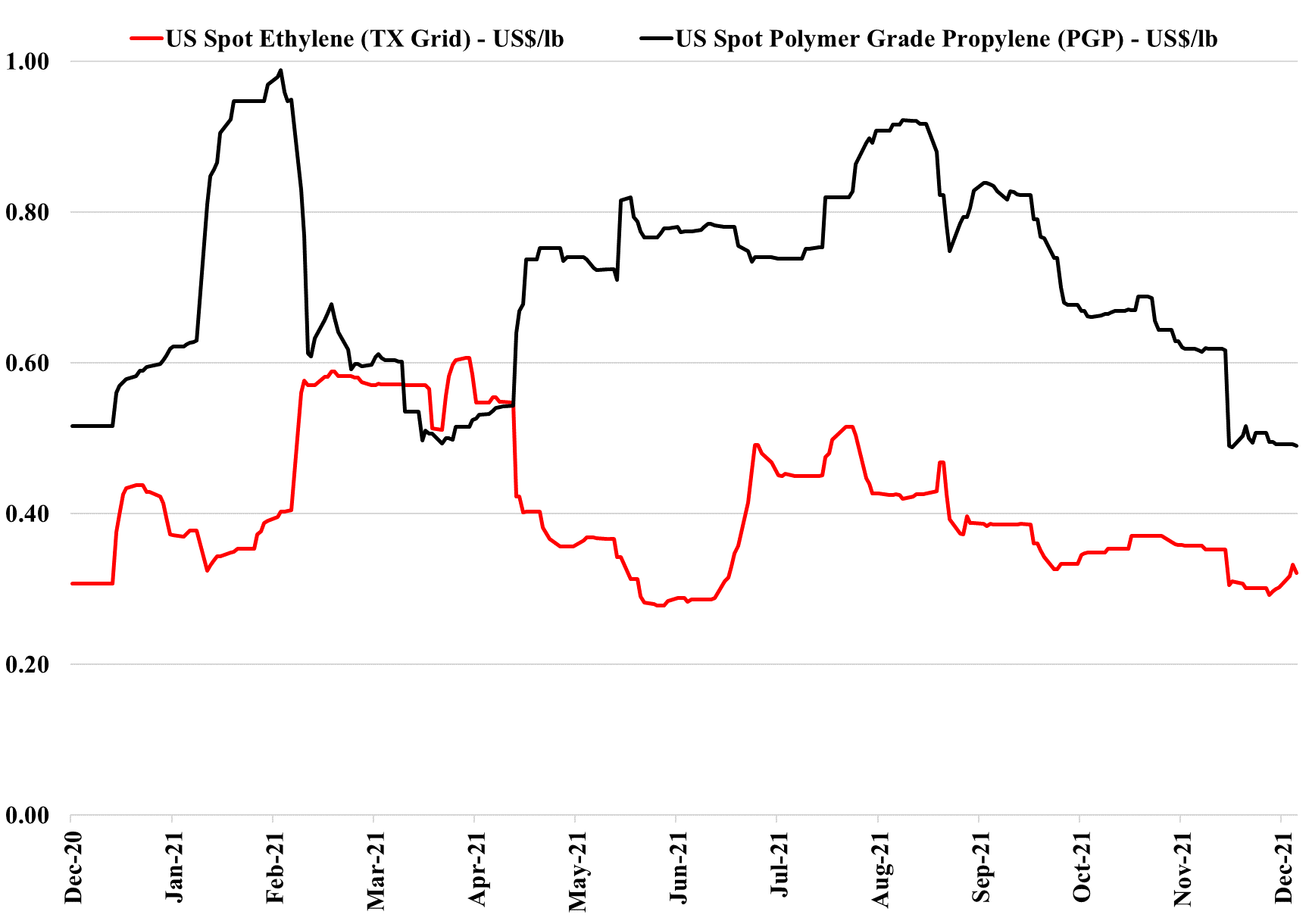

We have seen relative stability in US spot ethylene and propylene prices for several weeks now, despite some volatility in feedstock markets. Ethylene likely has significant export support in that there are complexes in Asia that are net short of ethylene and where derivative production can be increased if ethylene is available at the right price. There are also displacement opportunities if US ethylene can be delivered to importers in Asia at lower prices than local production costs. This is broadly the case today and there may even be select opportunities in Europe. In Asia it is likely easier, as the buyer would be replacing an alternate supplier. In Europe, most potential buyers would be looking at cutting back their own local production and that is a more marginal decision given the impact on unit economics of lower operating rates. US propylene demand remains high, but prices are now settling closer to PDH costs, although not close enough to encourage anyone to slow production. See more in today's daily report!

Following on from the Enterprise comments covered in our daily report, the company is more likely to acquire something in chemicals than build it in our view, especially if a move into ethylene or polymers is on the table. Today, building capacity will come with all sorts of emission-related restrictions most likely, and many of the new build announcements we have seen since COP26 have come with a carbon plan (Dow, Air Product, and Borouge). While it is not obvious today that any Gulf Coast ethylene capacity is up for sale, we would imagine that most companies are reviewing strategy and evaluating whether they have assets of entire businesses that may have a better owner. This would be especially true if a basic chemical business is holding back the valuation of a more interesting core. In the recent past, we have talked about the relative value arbitrage open to LyondellBasell from separating its compounding, licensing, and recycling business from the core. Maybe the core would fit well with Enterprise? As the chart below shows, there is money in buying ethylene for export, but there is more money in the US in making ethylene, as discussed in our daily report.

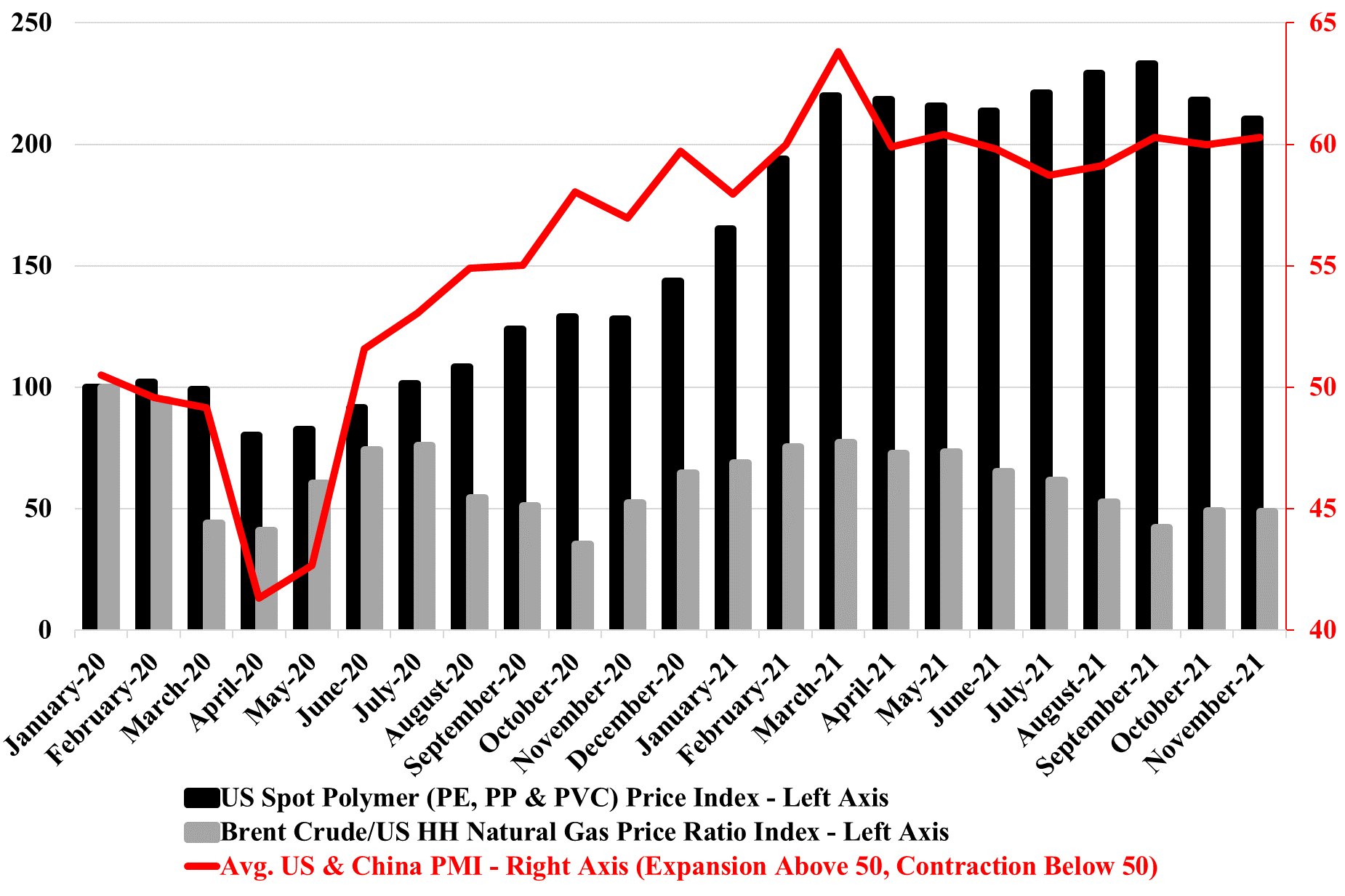

We have been asked a couple of times in the last week how US polymer (polyethylene in particular) pricing can remain so robust in a market where there is an inventory build going on. The PMI numbers are part of the answer. While we may be in the seasonally weaker part of the year, customers are still looking for more material than a year ago, and this makes the “we need a lower price” argument much harder, especially when the memory of 1H 2021 acute shortages is still fresh in the memory and when, more than likely, they are getting signals from their customers of a further step up in demand in 2022. We have done some traveling recently and the incremental demand for packaging polymers is very evident in the travel and leisure business, even if the number of travelers is still down. There is more packaging on airline and airport food and hotels are offering pre-packaged food for breakfast that would previously have not been individually packed. The reasons are obvious – safety and hygiene from the consumers' end and costs from the providers' end, as prepackaged food, can be bought in bulk and more cost-effectively and they likely have a longer shelf life.