The CP Chem propylene splitter announcement linked suggests that CP Chem expects surplus refinery propylene to be around for the long-term, and likely has supply lined up from the parent companies. However, this is still a bit of a gamble unless both parents see a scenario where they would change catalysts on FCC units longer-term and run at higher severity for more propylene and more hydrogen. This project looked a lot better only a few weeks ago than it does today – based on the spread in the Exhibit below, but propylene demand continues to grow faster than ethylene demand in the US and with all incremental ethylene capacity based on ethane, propylene consumers either have to choose the path from refineries or invest in on purpose PDH. PDH is an energy-intensive process with a large carbon footprint, and splitting refinery propylene likely looks far less problematic from an emissions perspective, especially if there is surplus process heat on-site. In our ESG report today we talk about polymer recycling into new end markets, but polypropylene may see more direct substitution, especially if we see consumables related polypropylene recycled into durable polypropylene markets. This might dent demand growth for polypropylene going forward, but probably not meaningfully.

Recent Posts

Following on from the LyondellBasell commentary in today's daily report, we would make one further, but very important point. With its refinery (granted the company is exploring opportunities to exit) and its huge commodity polyethylene, polypropylene, and propylene oxide business, any attempt to pursue a “specialty” strategy that encompasses the whole portfolio will be seen (crudely) as trying to put some lipstick on a pig! This rarely works in the chemical sector and the real transformation stories involve wholesale portfolio shifts, many of which have taken notable periods of time to develop. We still believe that the right path for LyondellBasell is to spin off the good piece – recycling, licensing, and compounding, or even better, find someone they can sell the business to through a Reverse Morris Trust. This strategy would likely allow the company to pay down (or shift) a significant amount of debt. The commodity business can then focus on the best strategy for a commodity polymer business in the face of energy transition, which might involve taking the business private or merging with another.

The theme of our Sunday report (to be found here) will be inflation this week and the signs that we are seeing across multiple industries which suggest it could be more problematic and worsen in 2022. One of the focuses is energy and how the pressures to be seen as good citizens is lowering investment in oil and natural gas production, while the world is not far enough advanced on energy transition to be able to substitute for the missing hydrocarbons. We would agree with many of the recent comments from some segments of congress, which is that the answer is not to curtail exports of LNG and crude, as by doing so we will starve the rest of the world of hydrocarbons and create worse shortages than Europe and China are seeing today. The better solution would be to support “clean” US production of the lowest emission fuels possible – especially for natural gas. As we have noted in prior research, with a global solutions hat on, the relatively low costs of natural gas F&D costs in the US, when combined with what we expect to be relatively low costs of emission abatement in the US, should drive more investment in the US, creating jobs and export income.

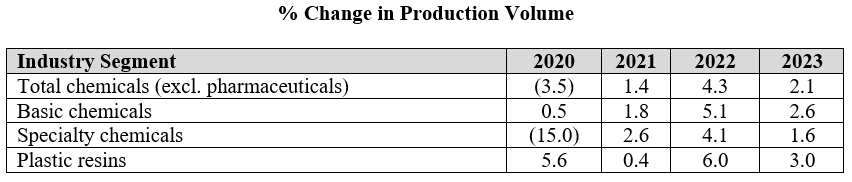

The ACC forecasts below leave us a little confused as the implication for specialty chemicals is that production declines in the US by an average of 2.0% per annum from 2019 to 2023. Given the demand that we are seeing for US manufacturing, as covered in our most recent Sunday Report, we would expect demand for all inputs to rise and it is unlikely that the gap would be filled by a swing in net imports. The lower demand from the Auto industry in 2020 and 2021 and broader manufacturing shutdowns in 2020 explains the 2020 and 2021 numbers to a degree, but it is not clear why there would not be a rebound as auto rates increase. We would also expect to see a stronger rebound in polymer production in 2022, assuming weather events are less impactful than in 2021, given substantial new capacity for polyethylene from ExxonMobil/SABIC, BayStar, and Shell.

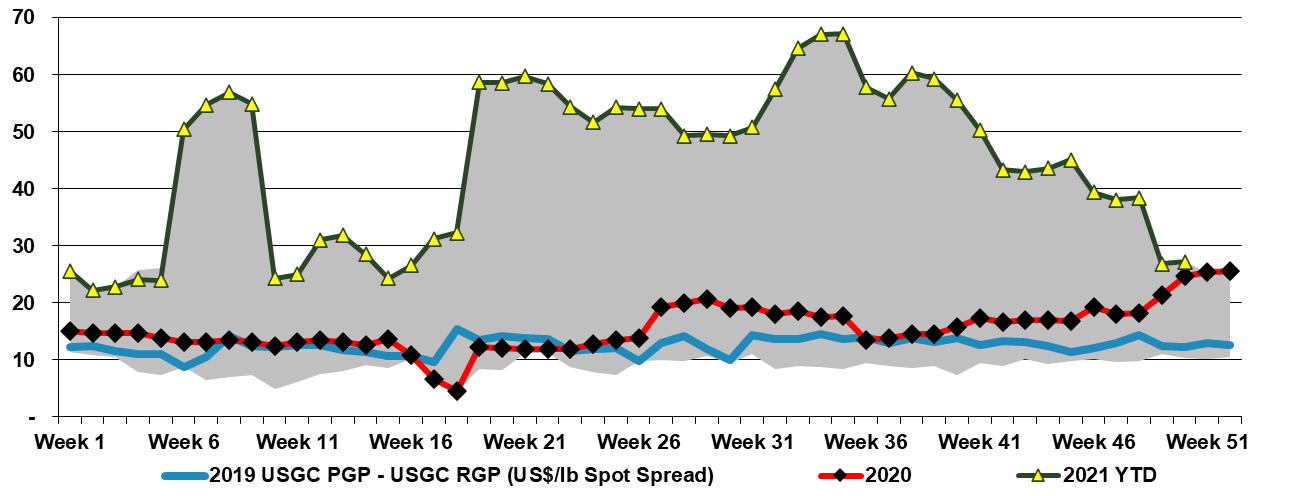

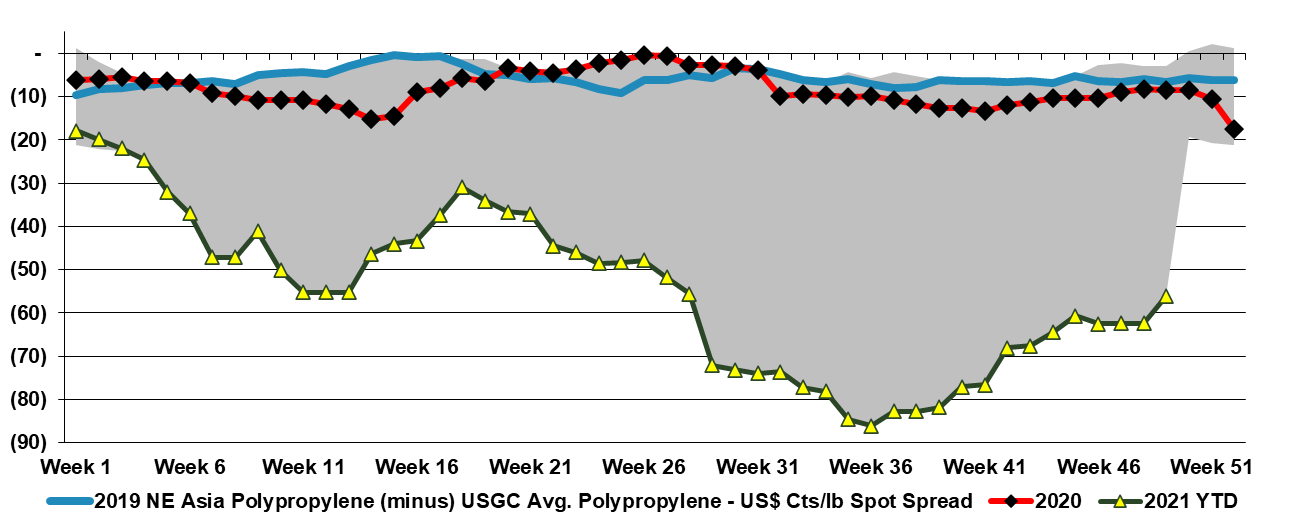

The polypropylene chart below, shows just how much of an impact the polymer has on the “average” in Exhibit 1 from today's daily report. Polypropylene is the only large volume polymer that can afford the freight rates to move surpluses from Asia to the US today and while some material is moving, volumes remain limited by the high cost of shipping and some of the additional logistic hurdles getting truck-based materials to US consumers that generally take the product by rail. The very high polypropylene margin in the US is a function not only of very strong demand but also demand that is likely growing faster than expected, giving buyers little negotiating room to get materially lower pricing. A year-end inventory correction from polymer buyers might send prices lower more quickly, but we have yet to see much evidence. We remain surprised by the apparent demand for polypropylene in the US given the lower automotive throughputs in 2021.

Our latest Sunday Thematic research report titled, "Reshoring Should Remain Supportive of Chemicals in ’22" studied the investment in US enterprise zones, near and medium-term, and the broad-based benefits for domestic supply chains.

The decline in US and global chemical pricing this week (as discussed in today's daily) is a function of oversupply in the US and lower costs in the rest of the world. The US has had an incentive to produce everything for most of the year and has had essentially full capacity to do so since the beginning of the 4th quarter. This will have collided with seasonally weaker incremental demand in December and the recent abrupt drop in oil and gas prices to swing momentum very much in favor of buyers. Polymer prices have to date been more stubborn in the US, but we expect continued weakness here also through the end of the year.

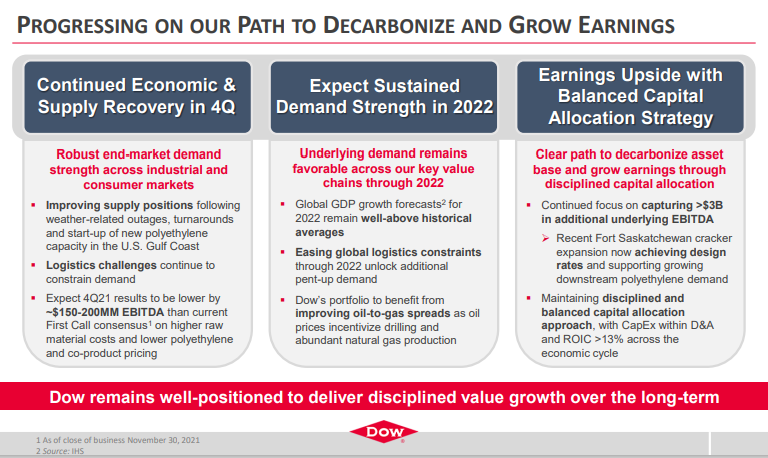

The recent Dow guidance is worth some further comment as it is being heralded in the stock market as an earnings miss, or at least that is what is implied in the stock performance, even though the signals around margin squeezes in 4Q have been in place for weeks and have been covered extensively in our work. Some elements of modeling chemical company earnings are complex, but rising energy (and therefore feedstock) prices is not one of them. We have commented several times over the last couple of years about the lack of almost any effort being made by the sell-side to rethink estimates mid-quarter, choosing instead to take or interpret company guidance (generally in the first month of a quarter) and then wait until earnings are reported. This does a disservice to both the institutional investors and the chemical companies, as the investors quickly conclude that estimates are likely too high – simply looking broadly at what sectors get hurt by rising energy – but generally do not have a good measure of by how much earnings will be impacted, so they sit on the sidelines, expecting the surprise. That said, there are so many algorithms working today that the alternative of gradual negative revisions to a more reasonable target for the quarter is also likely to hurt stock performance.

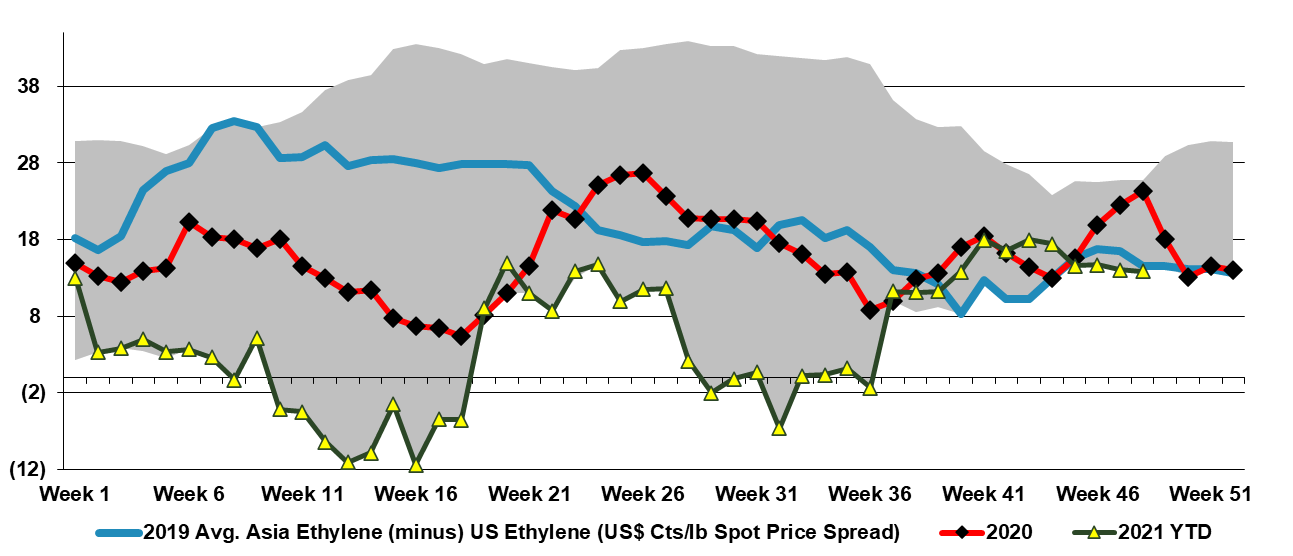

The Navigator Gas announcement should not be a surprise as the ethylene export arbitrage reopened in the US in September (Exhibit below) and since the terminal opened there has been a demand for ethylene exports each time the numbers have made sense. There are ethylene consumers in Asia that are net short and will buy incremental volumes from the US when the price is right relative to local suppliers and there is incremental demand in countries and regions that appear to be in surplus, including Europe, where a buyer can leverage an import to try to push local prices lower. In China, some of the facilities that require either propane or ethane imports might be better off buying ethylene versus making it today, and this is certainly the case for naphtha importers, as we highlighted in our Weekly Catalyst report on Monday. Today a US exporter can buy spot ethylene in the US and deliver it to China for less than the cost of manufacture in China, before the cost of getting the local ethylene to any consumer that is not on site.

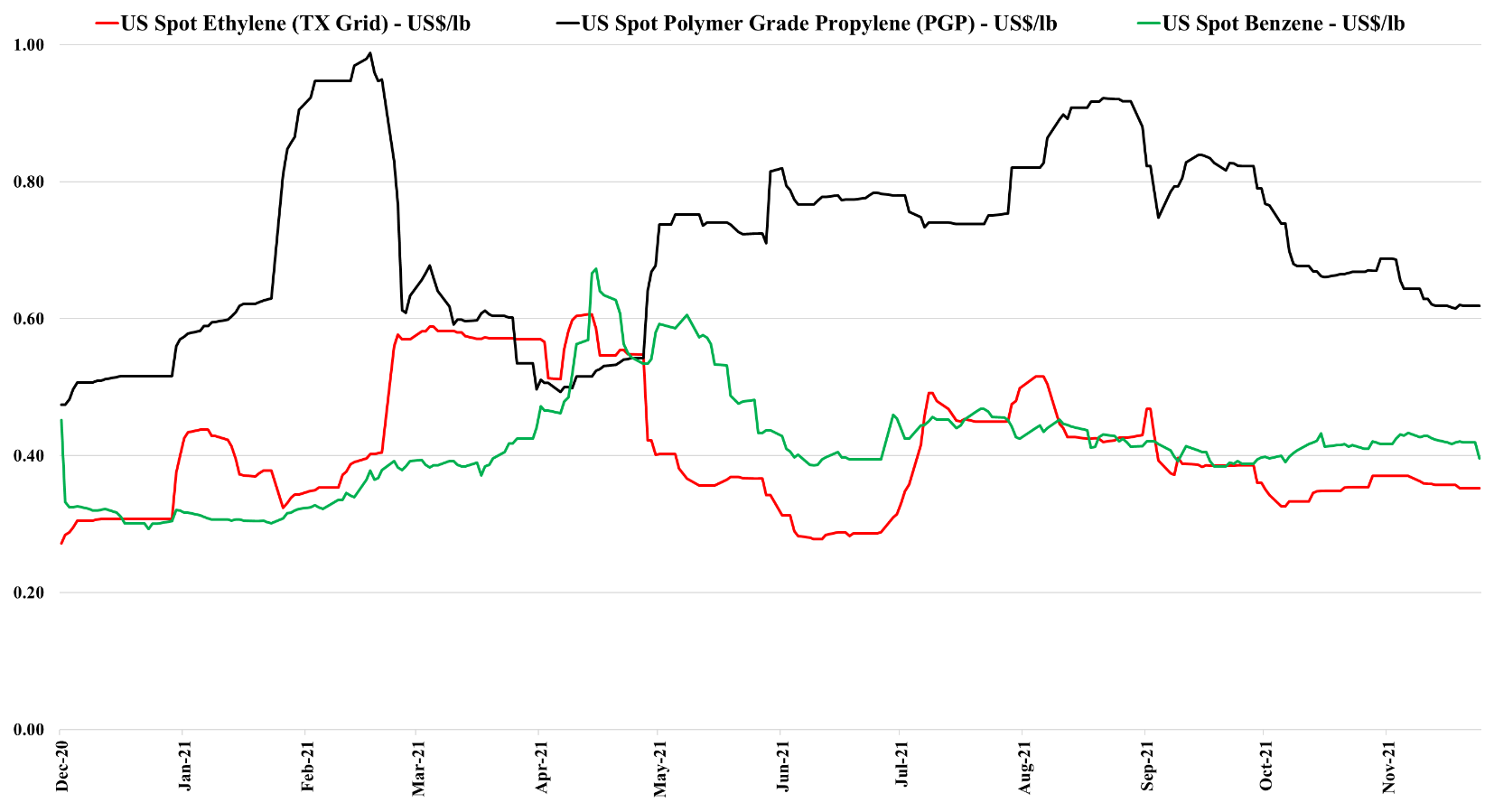

The drop in US benzene pricing is likely a function of lower crude oil pricing and the overall impact this is having on oil product values. As the US has moved to much lighter ethylene feedstocks, the proportion of benzene that is coming from refining is overwhelming and alternative values for benzene or reformate in the gasoline pool are a strong driver of US and international pricing. Lower naphtha pricing for ethylene units outside the US will also hurt benzene values. By contrast, the stronger natural gas market – through the end of last week - supported ethane pricing in the US and we saw a step up in propane pricing – which have provided support for ethylene and propylene – also note that the analysis we published yesterday in the weekly catalyst suggests that the US can export ethylene to Asia at current prices – delivering ethylene into the region below current local costs. This should keep a floor under US ethylene pricing although any further decline in crude oil prices relative to US natural gas and NGLs will close this arbitrage.