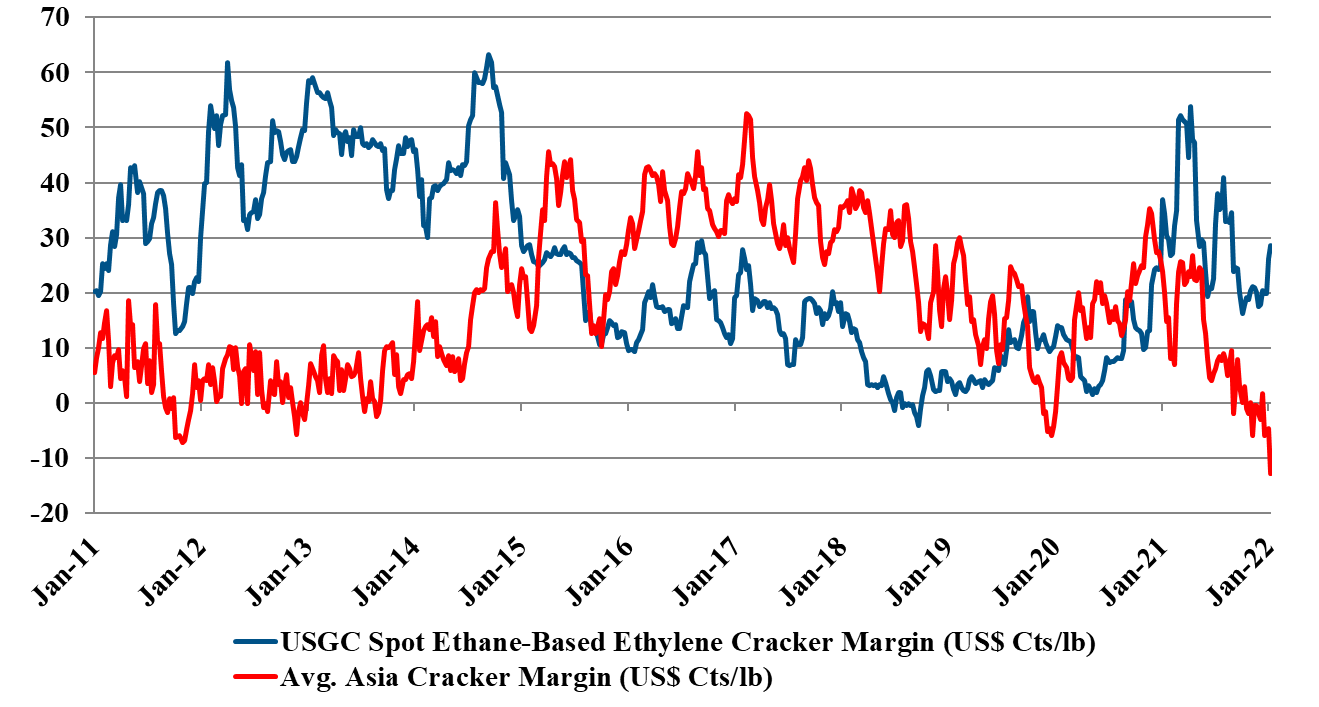

While it might be tempting (and perhaps easier) to focus on the negatives in the Dow earnings release – such as price declines in polyethylene and higher costs in Asia, we think it is much more interesting to focus on the positives. For a while now we have been suggesting that the industry is gearing up for a mega-cycle of profitability, perhaps as early as 2024 – see report – and we see nothing in the current macro environment or in Dow’s release to suggest we might be wrong. Demand growth is very robust across the industry, with consumer spending driving some quite impressive GDP growth numbers in the US in 4Q 2021, as an example. We often see companies suggest improving global operating rates in earnings calls, and while it is mostly hopeful and self-serving, the chart below, from Dow’s report may be conservative. The very high ratio of Asia costs versus US costs in the 2012 to 2014 period (second image below), because of high oil prices, effectively shutdown new naphtha based ethylene investment in Asia for several years and it is what prompted China’s move into coal-based and methanol chemicals (China has almost no ethylene capacity from methanol or coal in 2011, but close to 6 million tons by 2016). As the price of oil rises and the cost curve works against China and the rest of Asia again, the move to more coal is less attractive because of the environmental footprint – coal gasification creates a lot of CO2 emissions and elaborates CCS investment would be needed to justify further expansions, which increases the cost of ethylene production.

Recent Posts

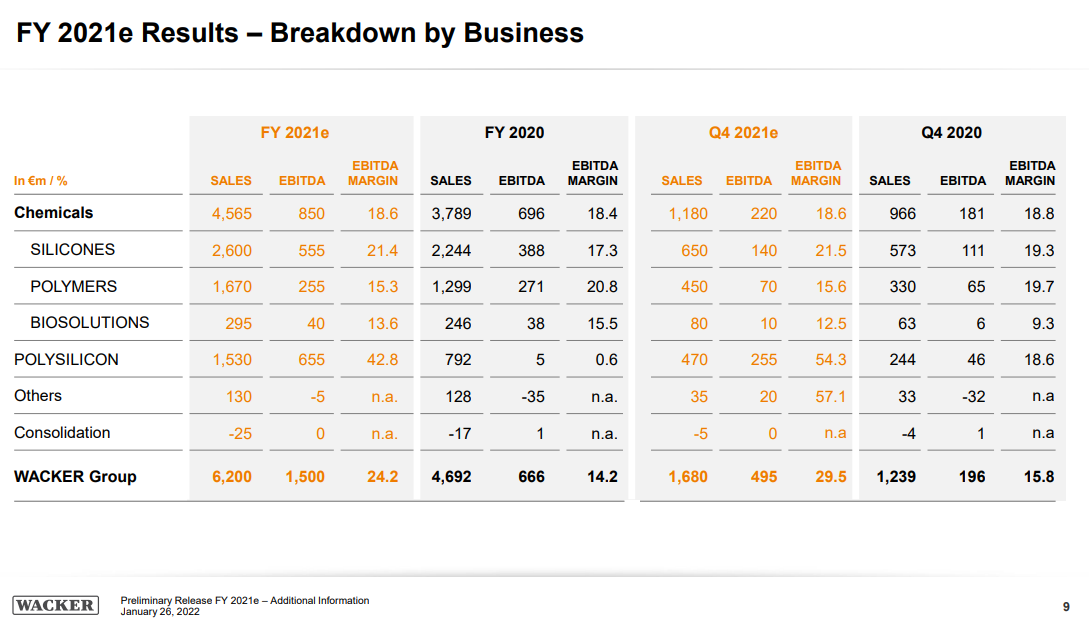

While this is covered in more detail in our ESG report today as well as our daily report, we highlight the Wacker results below. This confirms a key inflation fear for renewable power, as we see the rapid increase in silicon and polysilicon sales at Wacker – Exhibit below. Wacker has certainly seen significant volume growth between the periods highlighted, but the step-up in demand will have allowed the company to move prices up., something we have been noting for months, but it is good to have confirmation. This is additional cost pressure for the solar panel manufacturers and is driving solar module prices higher. Given the expected demand growth for solar installations, we see no reason why this demand-pull should ease any time soon. While this is a problem for the solar industry, their materials suppliers could do very well for many years.

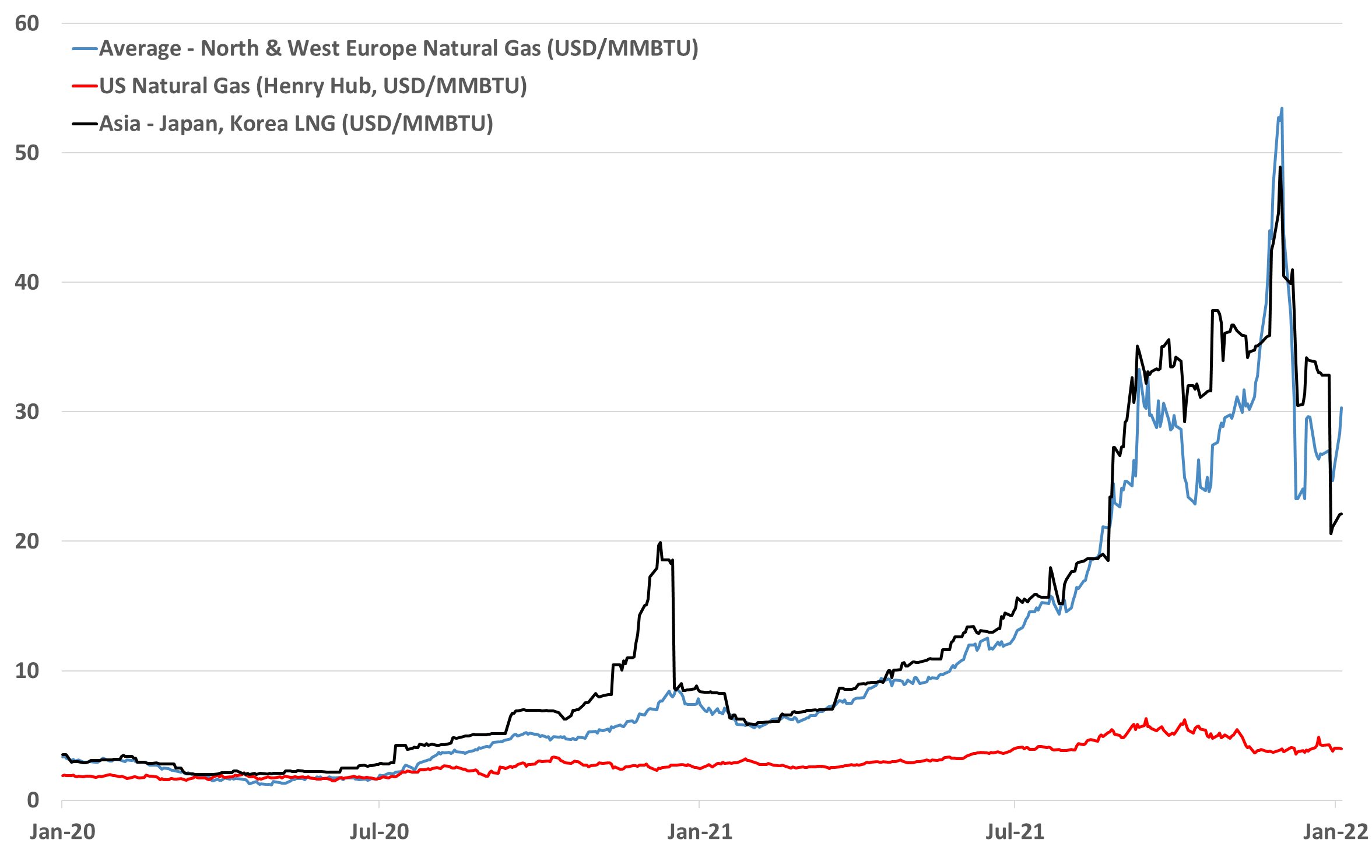

There are a couple of related topics in the charts below from today's daily report, as any conflict with Russia would almost inevitably impact European energy supply, raising prices for natural gas and pulling on as much LNG as possible. That said, we suspect that part of the recent run-up in prices has likely been to build a cushion of inventory, as much as that is possible with limited storage relative to demand.

Following on from the core theme of today's daily report, demand could provide the lifeline that the US chemical industry needs to get through what looks like a potentially oversupplied 2022 – note the successful start-up of the ExxonMobil/SABIC facility in Texas, announced today. While we still think that the US market will be looser in 2022 than in 2021, barring any above-trend weather events, strong demand growth could offer some pricing protection for the industry – especially given the input inflationary pressures that we are seeing. If the customer base is looking for increases in deliveries, which we expect to be the case in 2022, it will be easier to defend pricing and gain pricing where costs are higher. Some of the momentum that we are seeing in the commodity stocks year to date is a function of a broader inflation trade, but some is likely in anticipation that 2022 will not be as bad as had been expected and on that basis, the sector looks particularly inexpensive – even today after the early year rally. It will be a little harder for the specialty and intermediate companies depending on how long they have to play a lagging catch-up game with costs. But if, and when, costs peak, they should see margin expansion as costs fall and will be able to keep some of the gains, especially if their demand is also growing.

Ethylene producers in Asia are cutting back production because of the negative margins that some are seeing for much of their production. This will initially lead to higher losses as lower rates will impact plant efficiencies and raise unit costs. Cutting operating rates only works if prices rise as a consequence and if other producers choose not to cut back and seek to gain share, things get worse before they get better. The margins we show in the exhibit below are exceptionally low for Asia and are certainly at levels that would have caused many shutdowns in the past, but there are so many new players in Asia, especially in China that it may either take time or government intervention to get enough of a cutback to move prices. But if ethylene prices do improve in the region the arbitrage for moving ethylene in from the US goes up, so the US may gain more than the local producers. Also, as prices rise, someone in the region could look at marginal economics and start increasing rates. See more in today's daily report.

We have covered some of our Huntsman logic in today's daily report, but we would like to point out another concern that we find with Starboard’s proposal – the focus on operations and the nomination of Jim Gallogly as a potential board member. While we have nothing but great respect for Mr. Gallogly, and the work he did at LyondellBasell, we are concerned that Huntsman’s business model would not be best served with a “larger than life” board member with a very strong commodity background. We have seen several significant mistakes made in the past by commodity-minded companies and leadership, applying somewhat linear thinking to acquired businesses and we believe this could be a risk here. When Dow acquired Rohm and Haas one of the few mistakes that were made was looking at the acrylic acid business like a commodity and trying to drive more production through the units. The effect was to oversupply the markets and depress pricing and margins and it took a couple of years for the right management team to get the business back on track. Huntsman likely does not need more polyurethane and epoxy production if doing so creates a race to the bottom with competitors and destroys margins. The intermediate and specialty chemical business is as much about matching supply to demand as it is about plant throughput and efficiency. Every company can improve its operations and improve efficiency and costs but for some businesses, more material is not necessarily better. We believe that Huntsman’s stock would react negatively if the strategy changed to one of pushing as much volume as possible.

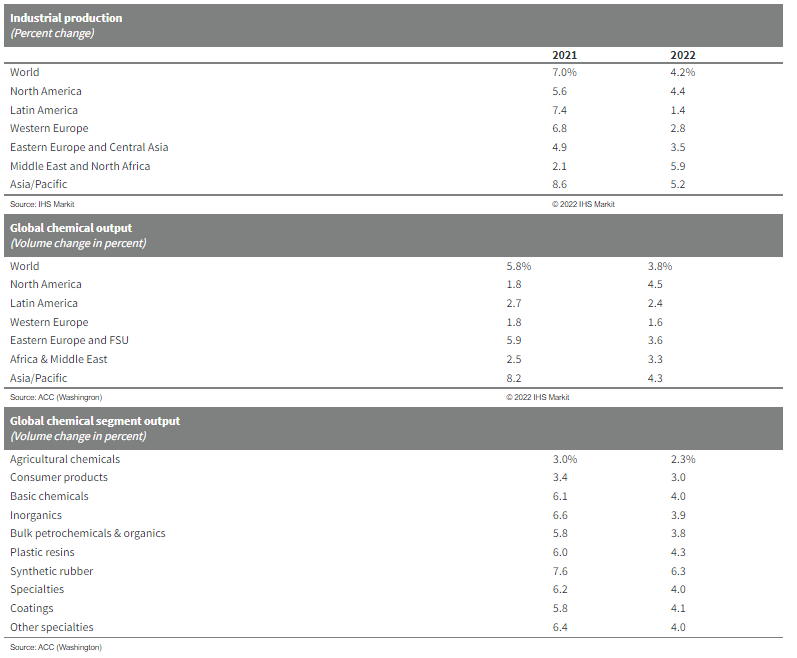

The jump in expected US chemical production in 2022 versus 2021 and the more anemic growth in 2021, is in part due to new capacity in the US but is likely more a function of lost production in the US in 2021 because of the February freeze and the hurricane that hit the New Orleans area. These two weather events, especially the freeze, cause significant production cutbacks, and not only would production have looked better in 2021 without them, but the inventory decline shown in Exhibit 1 in today's daily might have been less severe. IF we assume that climate change is causing more severe weather, then perhaps it would be prudent to build more unplanned downtime into forecasting models and on that basis perhaps the production growth forecast in the exhibit below is too hopeful. However, if you model more unplanned downtime you are inevitably going to end up with a more volatile market as available capacity will swing around the forecast average by a larger amplitude, which would make production and inventory planning more complicated.

We are seeing pockets of real demand strength in some areas of chemicals, such as building products, and this is allowing producers to push through price increases to reflect higher costs and most likely add some margin. In other areas where the fundamentals might not be quite as supportive, we are still seeing attempts to pass on higher costs. Sika has supported what we have heard from many over the last few weeks, which is that the building products chain remains tight, as demand is strong, capacity is running hard and logistic issues continue to cause problems in some cases from a raw materials perspective and in others from getting finished products to market. Where there is limited ability to increase supply, those selling into the building products space are likely to make more money as they should have strong pricing power – in the US chemical space, we would favor Westlake as a potential big winner from this trend, but Huntsman should also be on the list.

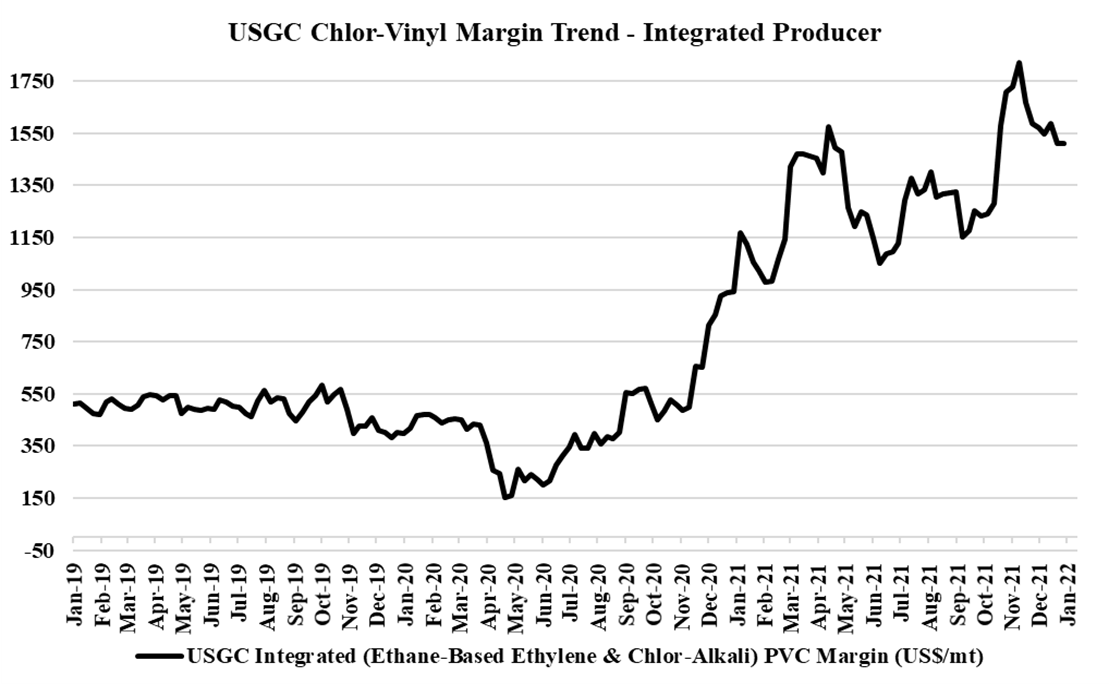

While the Shell headlines today are probably the biggest news, it should not be a surprise to anyone that earnings are lower in 4Q than they were in 3Q, as all of the market indicators have been telling us this for months, and Dow made a statement to this effect in early December. Given the location of Shell’s Norco facility, it took a full hit from Hurricane Ida and the company made several statements at the time regarding delays to restarts. We expect other chemical companies to post meaningful declines in earnings for 4Q relative to 3Q 2021, but unless, like Shell, they experienced meaningful production outages, we would still expect 4Q results to be above “normal” and higher than earnings in 2019. We still see share prices for the public companies as very low looking at values relative to 2019 and earnings relative to 2019, but the negative momentum in earnings is more important to investors today than the absolute level of earnings. As we have stated in prior work, we need to get through negative revisions before the sector could look interesting. The exception, as noted in our Daily Report today, could be PVC, where pricing could look better than is already implied in 2022 estimates and valuation. A positive tone in upcoming conference calls may be a turning point for the PVC-related stocks – Westlake primarily. We could see the trend in the chart below reverse.

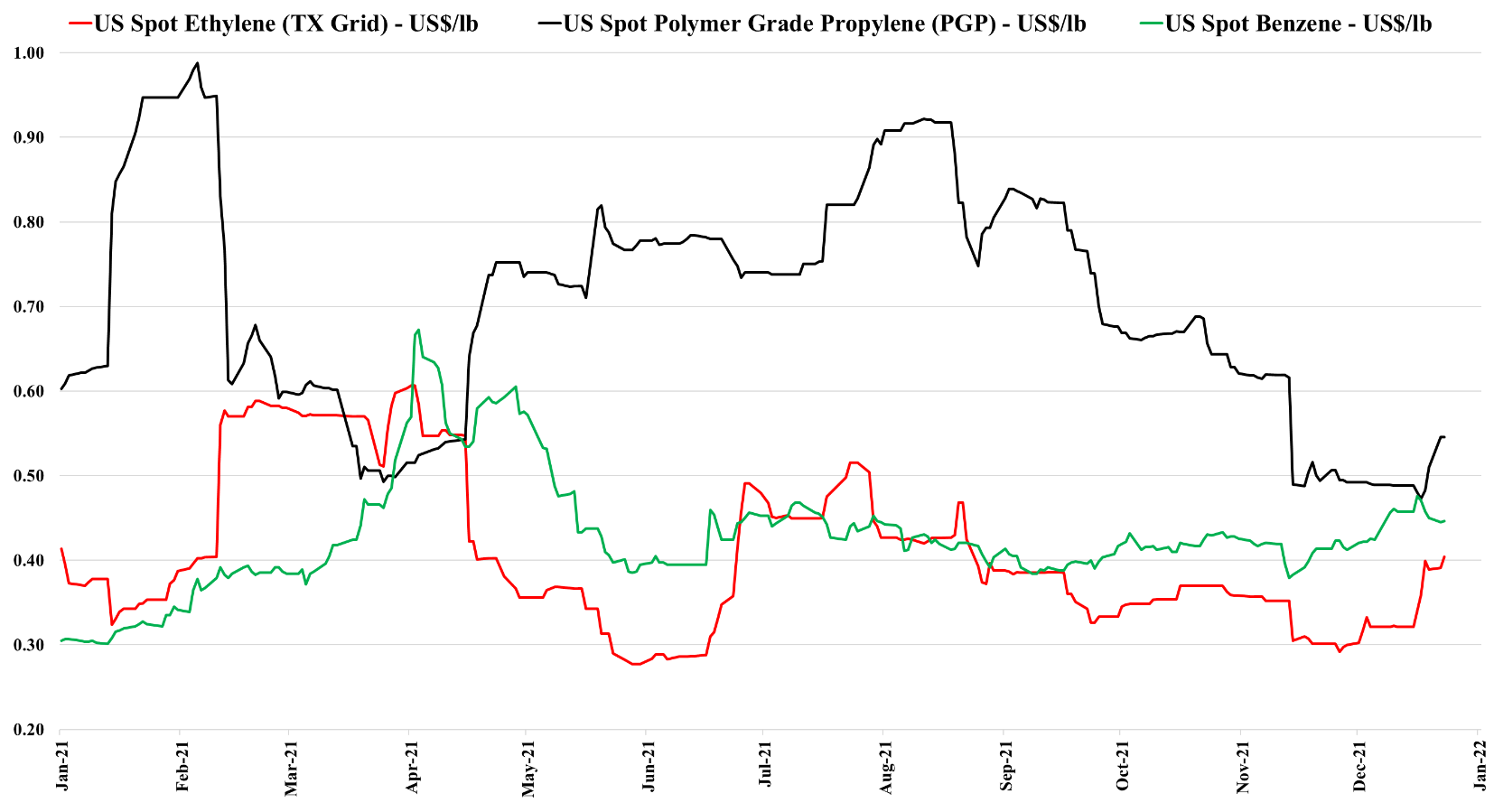

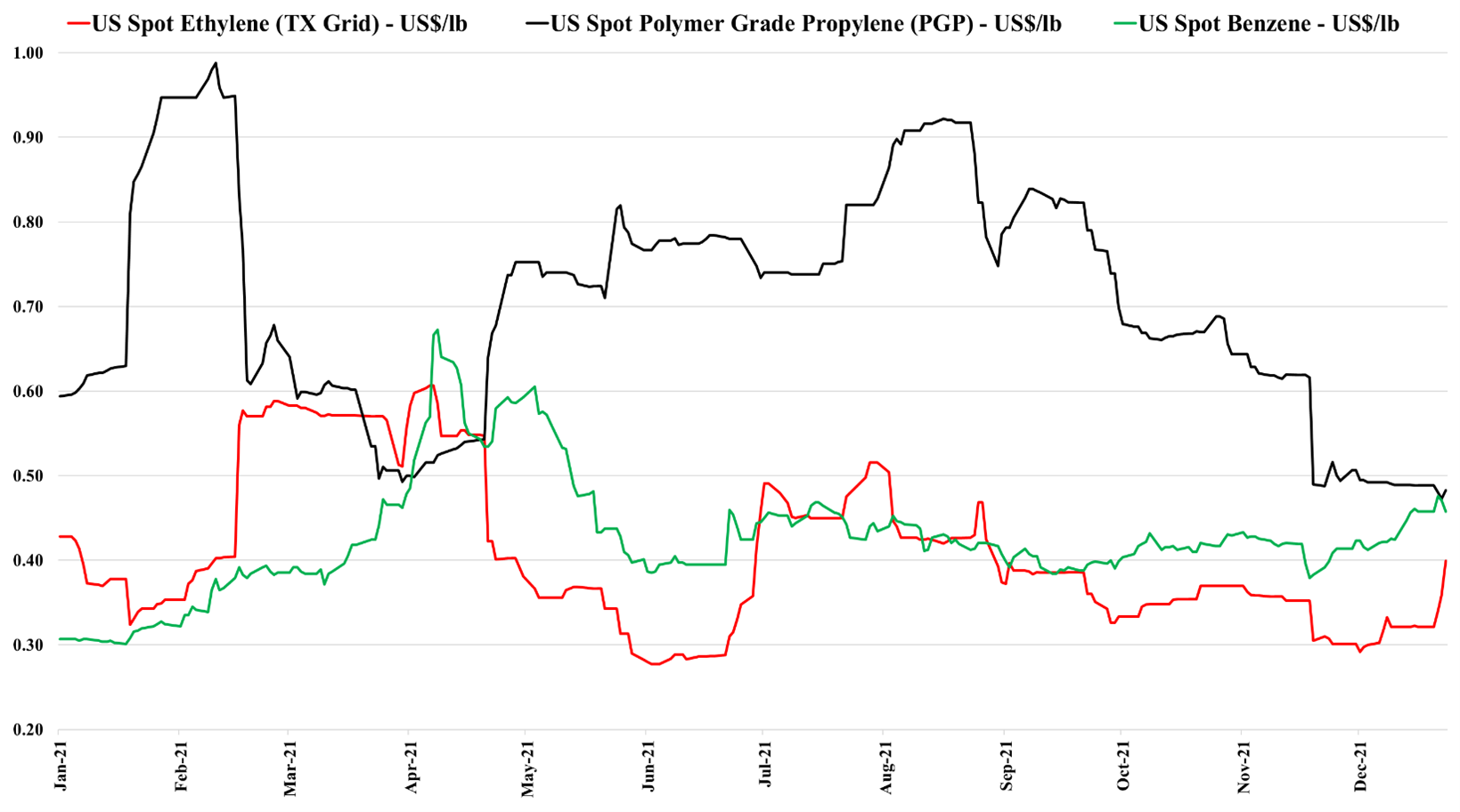

The run-up in ethylene spot prices in the US is interesting because it takes away most of the export arbitrage to Asia, as summarized in the charts below. Our margins models suggest that Asis is losing money making ethylene from imported naphtha today – especially in China and the arbitrage looks more interesting for US exporters of ethylene if you look at China costs as opposed to China prices for ethylene. The US remains a preferred supplier of ethylene to parts of Asia that would otherwise import from more local producers as our local cost analysis does not include a freight component. For example, an ethylene buyer in Southeast Asia could still get material from the US cheaper – even with higher US prices – than from China or other local exporters. For more on ethylene and propylene markets see our Daily