The linked China polyethylene headline highlights a possible risk for US producers, as we link much of what is happening in China to logistic challenges. China has high production costs in a high oil environment, which is driving some of the cutbacks, but a portion is likely driven by an inability to move product and a huge disincentive to build inventory at break-even or negative margins. If the current shipping challenges in China roll over more aggressively into the rest of the world and container and vessel availability fall again, the US may face more challenges exporting polymers. As warehouse space fills, especially on the Gulf Coast, we may see some need to cut back rates, even if all of the material in storage currently has an agreed home and an agreed price. The US can afford to build inventory, as production costs still remain attractive relative to international prices, but if the supply chain is full there could be nowhere to put more material. One of Union Pacific's issues highlighted last week was too much inventory in rail cars, snarling up the system.

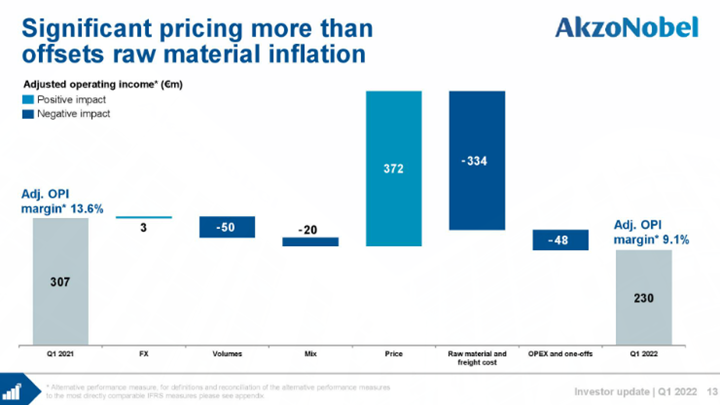

We have discussed in several recent reports the very mixed fortunes in the intermediate and specialty chemical sector related to whether companies have been able to move prices fast enough to cover costs. The two large blue bars in the AkzoNobel chart below show that Akzo was close, but did not make it. We expect other examples like this over the coming weeks but we also expect some companies to have done better – some of this depends on mix and contract terms, but a lot has to do with how early you acted on the rising cost trend and how aggressive you were willing to be with customers. Dow is another example of a company struggling to get pricing high enough to cover cost increases, although Dow and others have aggressive price increase announcements in the market for polyethylene for April and May that would make a significant difference to US margins if successful.

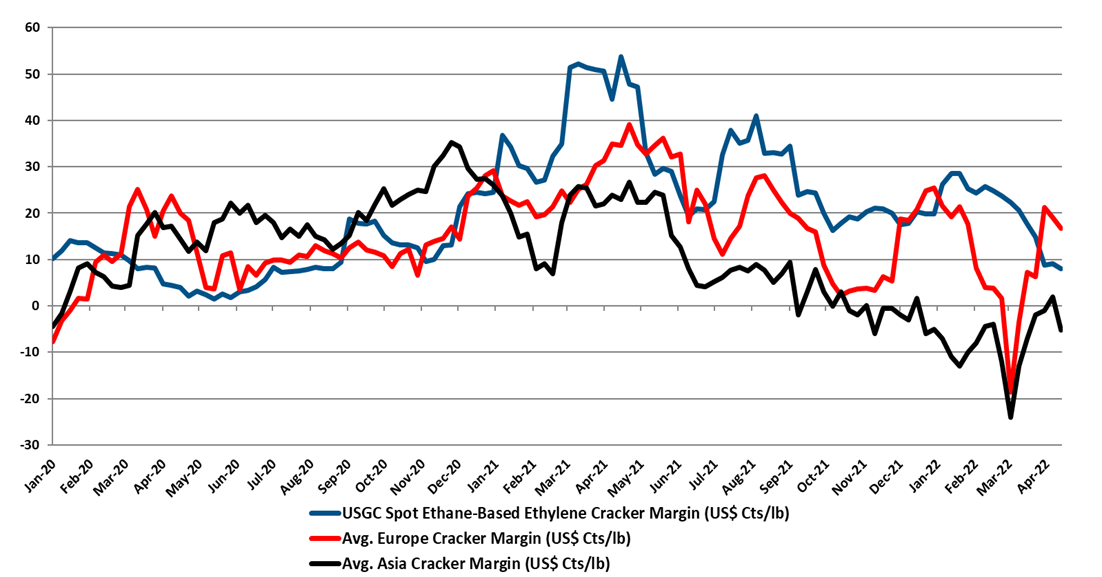

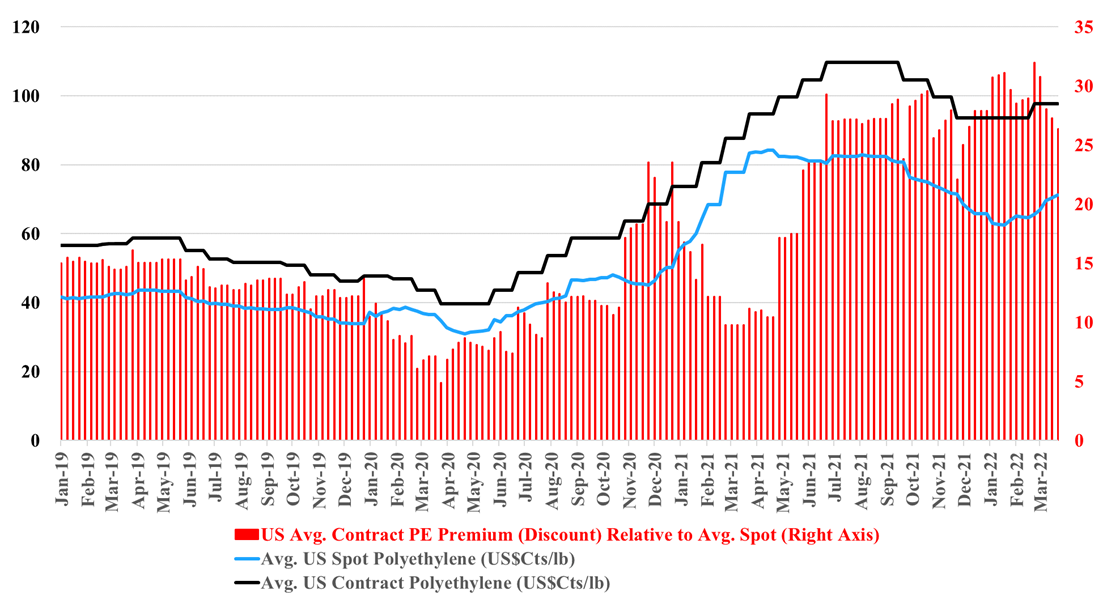

We note the polyethylene price nominations in the US, timed by some to coincide with earnings releases this week and next, and would remind clients that there is always price momentum in commodities, one way or another. In our view, the price increase moves aim to maintain directional momentum (upwards) while giving the polymer producers some cover should natural gas prices spike further. US ethane prices are now tracking natural gas more closely and have moved up meaningfully over the last few weeks, and US ethane-based ethylene margins have fallen around 80% since the start of the year, with at least half of that coming from cost increases. All polyethylene producers are integrated back to ethylene, and the price nominations will be attempts to recoup some of the cost increases. This is against a backdrop of still very strong polyethylene margins in the US, which although way off their 2021 highs remain much higher than in 2019 and 2020 and the longer-term average. This is covered in our Weekly Catalyst report each Monday. Ethylene margins are summarized in exhibit below and the chart shows the impact of higher costs in the US and falling spot ethylene prices as the US now has more surplus ethylene capacity and is looking for export homes for ethylene and easy to ship derivatives. As we have noted before, the jump in margins in Europe and Asia is because of extreme volatility in naphtha markets over the last couple of weeks. We would expect margins to be lower next week based on naphtha moves this week.

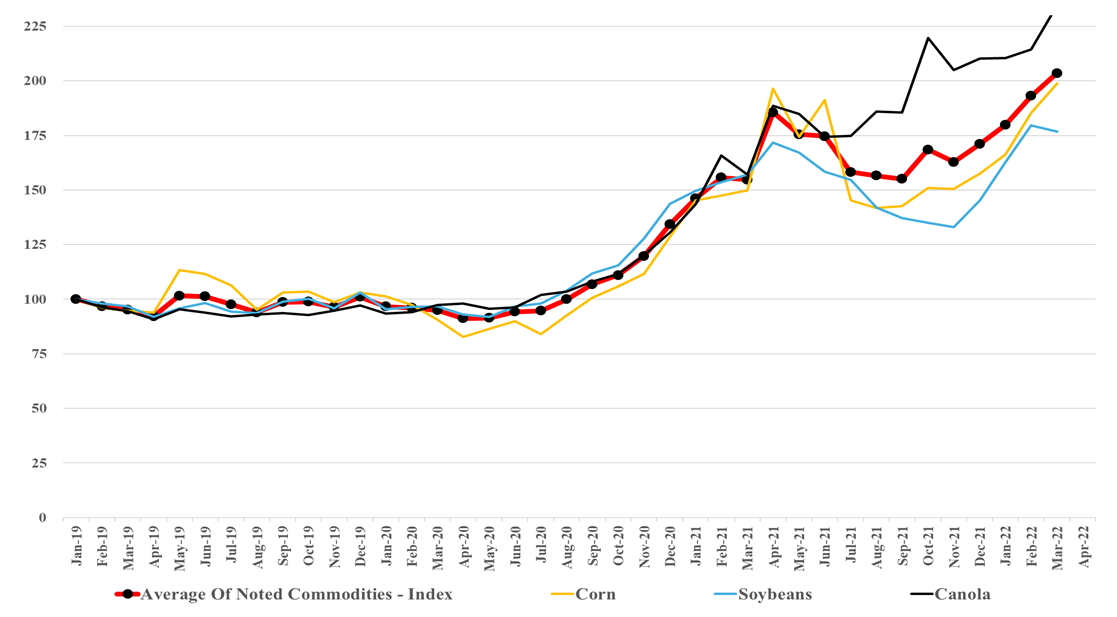

In our ESG and Climate report tomorrow, we are focusing on renewable materials and fuels, emphasizing counting carbon and the importance of verification and auditing. However, one of the side issues concerning renewables is their impact on food prices if they bid crops away from the food chain. The chart of the day from our daily chemical reactions report shows that corn prices are above their historical correlation with crude oil, but it also indicates a correlation and fuel markets can pay more for corn and other crop-based fuels when oil prices are high. The issue with exhibit below is that we already have inflated crop prices with minimal incremental demand for the fuel markets today. Prices are rising on strong global demand growth for food – supply chain issues that existed before the Ukraine crisis and – the supply challenges that are a direct consequence of the Ukraine crisis. This is before any significant investment in renewable fuels or materials. As governments implement policies to encourage renewable fuels – especially SAF – they need to consider what policies and incentives might be required in addition to price, encourage meaningful changes to the acres planted around the world, and help productivity where it is low.

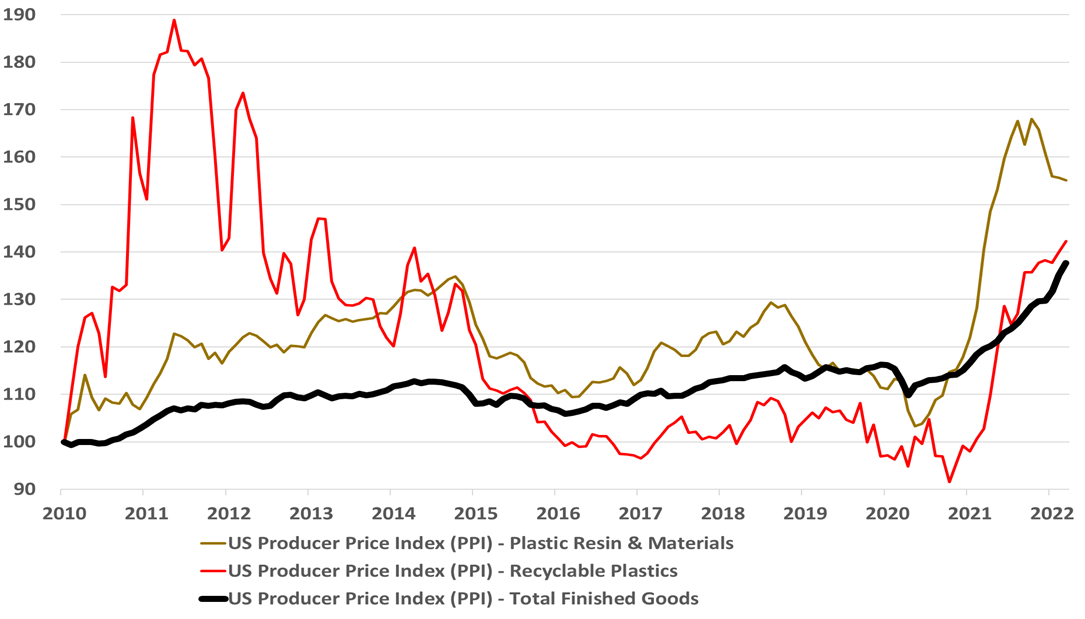

It is important to note from the chart below that the US plastic resin price index is out of phase with the overall industrial products markets as we saw a shortage driven peak in 2021 – largely weather and supply chain-related. The US on average continues to command resin price premiums relative to Asia. The China polymer surpluses are largely land-locked for now because of very high shipping costs and very high oil-based production costs, and the US surplus is also challenged because of logistic issues with exports. In the US, exporters are building inventory in anticipation of better logistics and on the basis that the surpluses for the most part have customers. If we do see a global slowdown in demand, triggered by inflation – see our most recent Sunday Recap – the inventories in the US and China could become a problem.

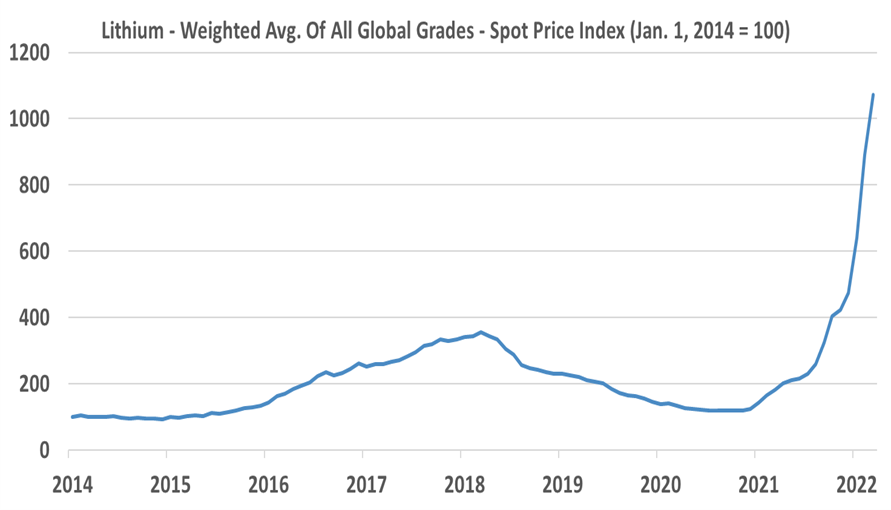

Lithium prices keep rising. We refer back to some work we did on the subject several months ago, where we predicted that lithium was likely to be a cyclical commodity - eventually. Right now we see demand for new EVs, demand to fill the supply chain for new EVs, and demand to fill the supply chain for new battery factories – and consequently, demand is likely overstated relative to the number of EVs leaving production lines. In lithium’s favor, EVs are surprising on the upside in production and sales, but this will add to the need to fill supply chains. We do not see the lithium bubble bursting soon, but we do not see enough barriers to entry for lithium to protect the product from overbuilding. There are many dilute lithium sources, and high prices could allow for some high-cost options to move up the learning curve and become future low-cost options.

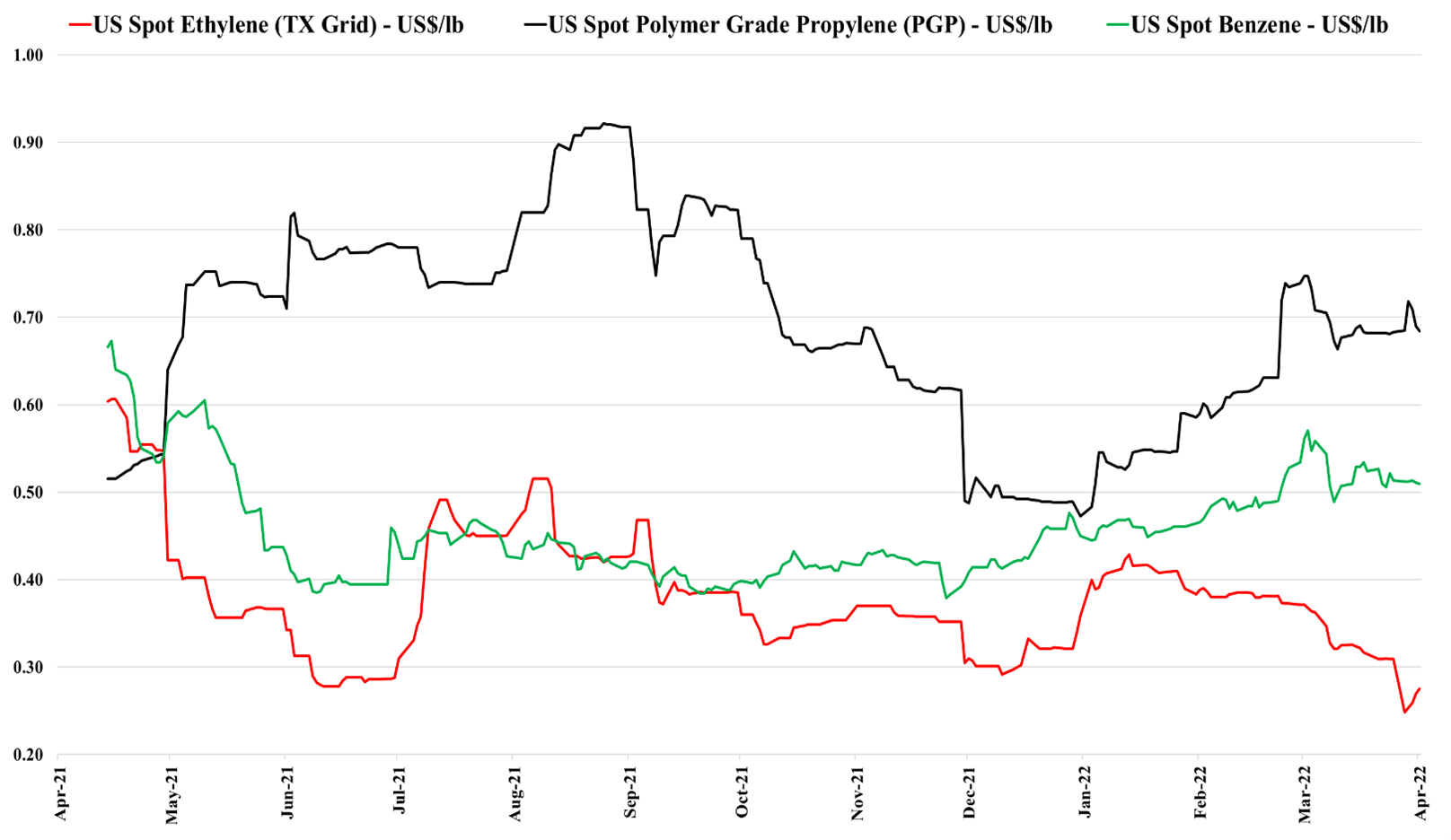

US ethylene prices have bounced off a low this week largely, in our view on the steep rise in natural gas and ethane. The drop in ethylene prices over the last couple of weeks signals an imbalance whereby production is more than enough to satisfy domestic demand and export demand. Export demand is limited by terminal capacity, and we have seen some domestic demand issues for polyethylene, not because of demand weakness, but because of export logistic bottlenecks, that are resulting in product (with homes to go to) backing up in the US ports. Given the timing of this build-up, we may see some higher end-quarter working capital from some of the chemical companies with sizeable export footprints for 1Q 2022. The sharp increase in US natural gas prices and the catch up that ethane has made to natural gas, should keep some upward pressure on spot ethylene prices if gas prices remain high. Propylene remains very supported by high propane prices.

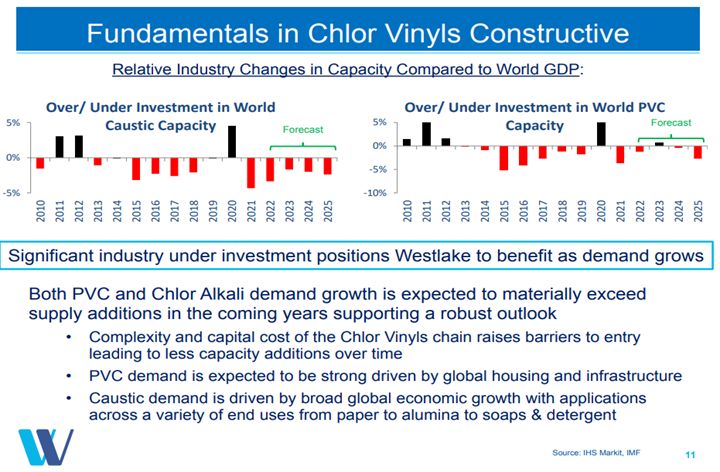

The margin weakness in PVC, as shown in Exhibit 1 from today's daily report, suggests that the market might be weakening, but higher prices would suggest that it is not. The integrated margin weakness is mostly the result of rising costs, and the US PVC market may be strong enough to allow producers to pass on these costs fully over time. We still see PVC as the least risky way to play the US polymers market as infrastructure and manufacturing investments should keep demand strong even if we see a decline in consumer durable related spending. The Westlake chart below highlights one of the primary drivers behind our mega-cycle view – no new capacity. The supply shortfalls that are implied in the chart will be mirrored in other basic chemicals in our view but PVC is likely the most acute example – creating what could be a prolonged period of strong margins for the industry.

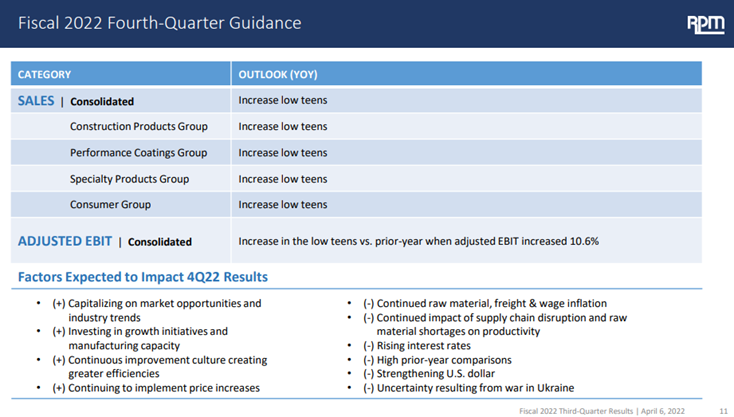

While we remain advocates of “stronger for longer” with respect to chemical demand and pricing in the US, the auto data does suggest that the US consumer may be cooling off a bit in reaction to higher prices and higher borrowing rates. Historically, the chemical industry has a habit of running headlong into a downturn while waving an “everything is great” flag, and the RPM results and outlook have a vague “deja vu” feel to them. We also note some surprise at the robustness of the MDI market in the chart below, and it would be wrong not to admit that our cautionary antennas are rising. The auto exposed products should still see some upside from higher auto production in the second half of the year, but otherwise, a possible consumer pullback to take the wind out of the sector sales, especially if the US is constrained moving out products because of container and shipping issues. The significant cost advantage remains in the US but the ethylene market over the last week is a reminder of what can happen when you struggle to find someone who can take the last pound. Given infrastructure, energy, and clean energy investment, as well as reshoring, many materials could see significant offsets to consumer spending pullbacks and our focus would remain on PVC and building products, as most of the hit would be in consumer durables. Metals demand should remain strong regardless. For more see today's daily report.

It's back to 2012/2013 for polyethylene, but with a potential twist. As we noted in today's daily report, international prices for polyethylene are being pushed up by oil prices, and even with higher prices in Asia, margins are still negative locally, which suggests that they will go higher. This margin umbrella is what generated windfall profits for US and Middle East producers in 2012, 2013, and half of 2014. The upward pressure remains high for international polyethylene prices because producers are not covering costs locally and in theory, the US should continue to benefit and we see domestic polyethylene prices rising again, both contract and spot. The risk for the US is local overcapacity of polyethylene and potential export challenges. The pricing arbitrage to export US polyethylene is huge and rising, but we are in a constrained trade world and we understand that export terminals are at capacity and warehouses are full. It is possible that the sharply lower US ethylene price is not just a function of new ethylene capacity, but also a function of integrated polyethylene producers choosing to limit production and looking for homes for the extra ethylene. If the polyethylene producers in the US try to push more volume domestically we could see local prices fall well below their export alternative – this is possible, but unlikely, in our view. Polypropylene does not have the same significant net export and the two plant closure in the US are likely enough to drive the price support that we are seeing this week.