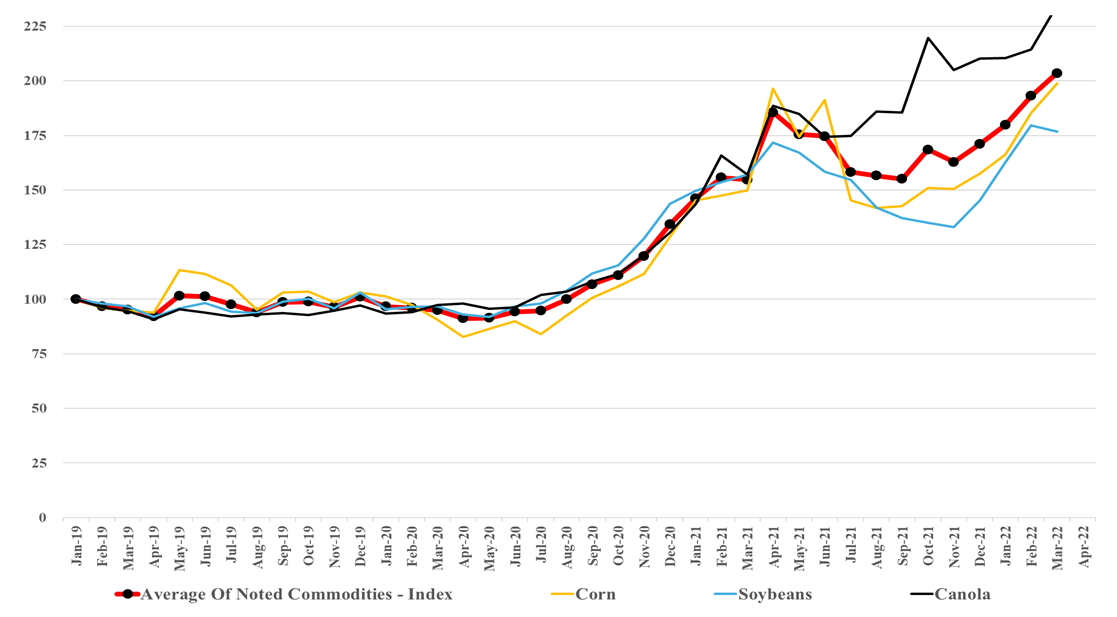

In our ESG and Climate report tomorrow, we are focusing on renewable materials and fuels, emphasizing counting carbon and the importance of verification and auditing. However, one of the side issues concerning renewables is their impact on food prices if they bid crops away from the food chain. The chart of the day from our daily chemical reactions report shows that corn prices are above their historical correlation with crude oil, but it also indicates a correlation and fuel markets can pay more for corn and other crop-based fuels when oil prices are high. The issue with exhibit below is that we already have inflated crop prices with minimal incremental demand for the fuel markets today. Prices are rising on strong global demand growth for food – supply chain issues that existed before the Ukraine crisis and – the supply challenges that are a direct consequence of the Ukraine crisis. This is before any significant investment in renewable fuels or materials. As governments implement policies to encourage renewable fuels – especially SAF – they need to consider what policies and incentives might be required in addition to price, encourage meaningful changes to the acres planted around the world, and help productivity where it is low.

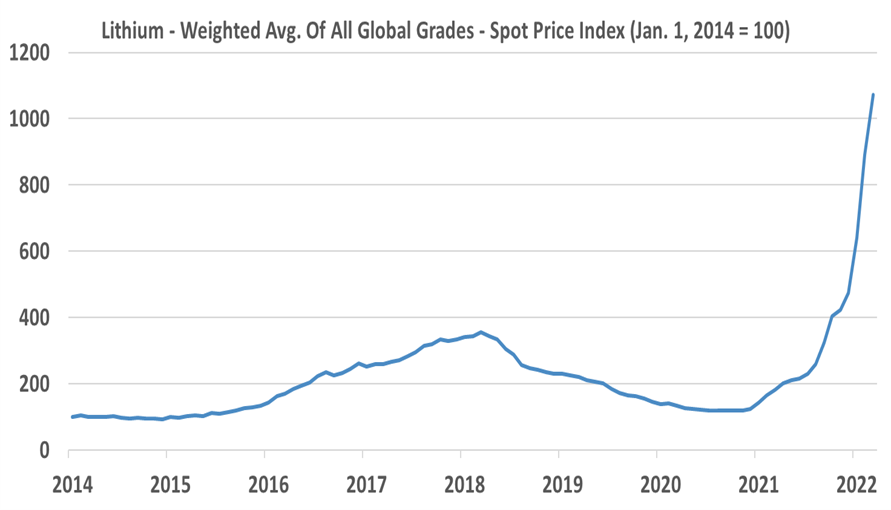

Lithium prices keep rising. We refer back to some work we did on the subject several months ago, where we predicted that lithium was likely to be a cyclical commodity - eventually. Right now we see demand for new EVs, demand to fill the supply chain for new EVs, and demand to fill the supply chain for new battery factories – and consequently, demand is likely overstated relative to the number of EVs leaving production lines. In lithium’s favor, EVs are surprising on the upside in production and sales, but this will add to the need to fill supply chains. We do not see the lithium bubble bursting soon, but we do not see enough barriers to entry for lithium to protect the product from overbuilding. There are many dilute lithium sources, and high prices could allow for some high-cost options to move up the learning curve and become future low-cost options.

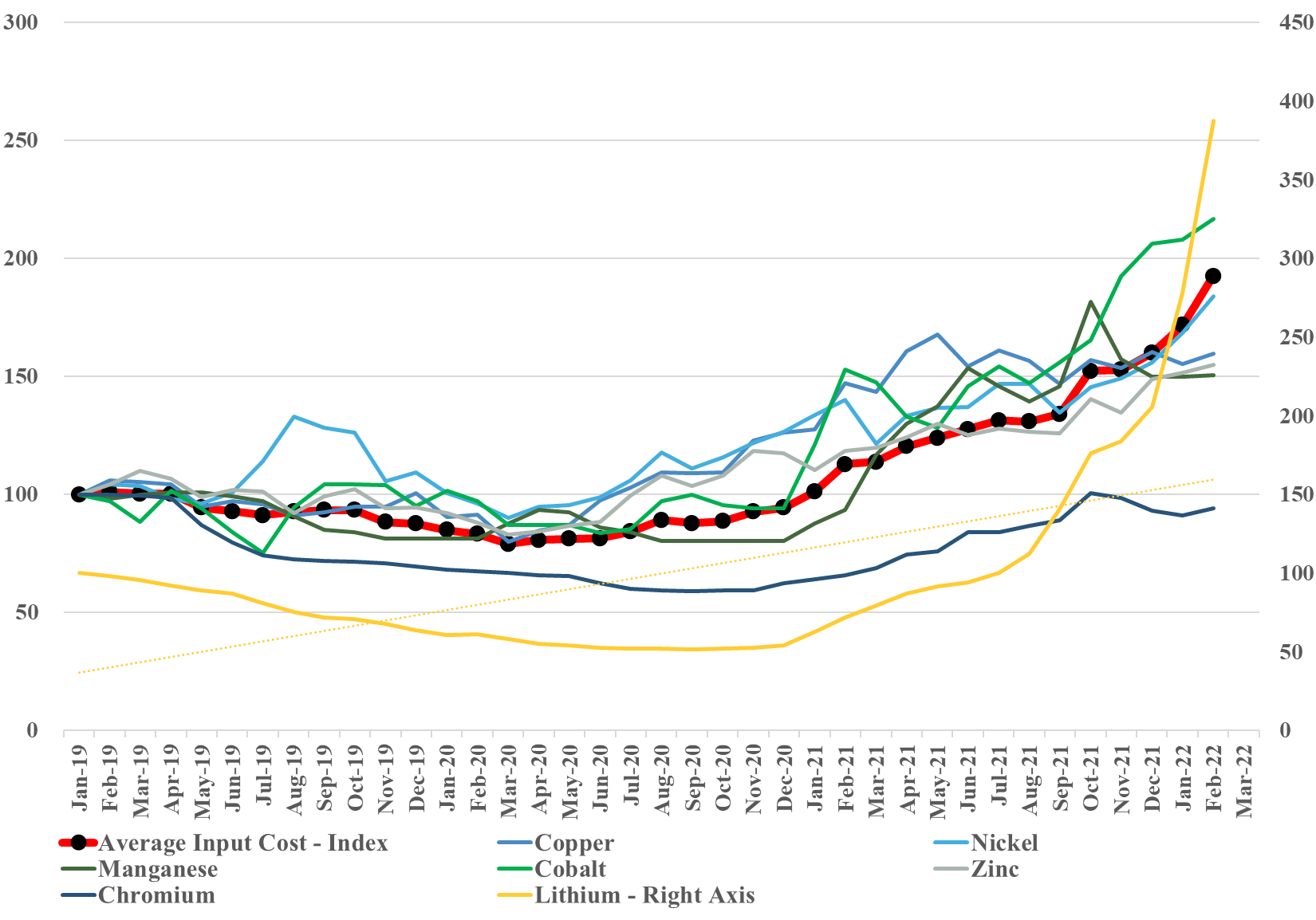

One of the key messages from the World Petrochemical Conference is that it is not an oil shortage, it is a commodity shortage, and we show our key metals index (updated through February) again in the chart below. We will update this again at the end of March (when consistent data is available) and given what has happened to both lithium and nickel prices we would expect a jump in the March index.

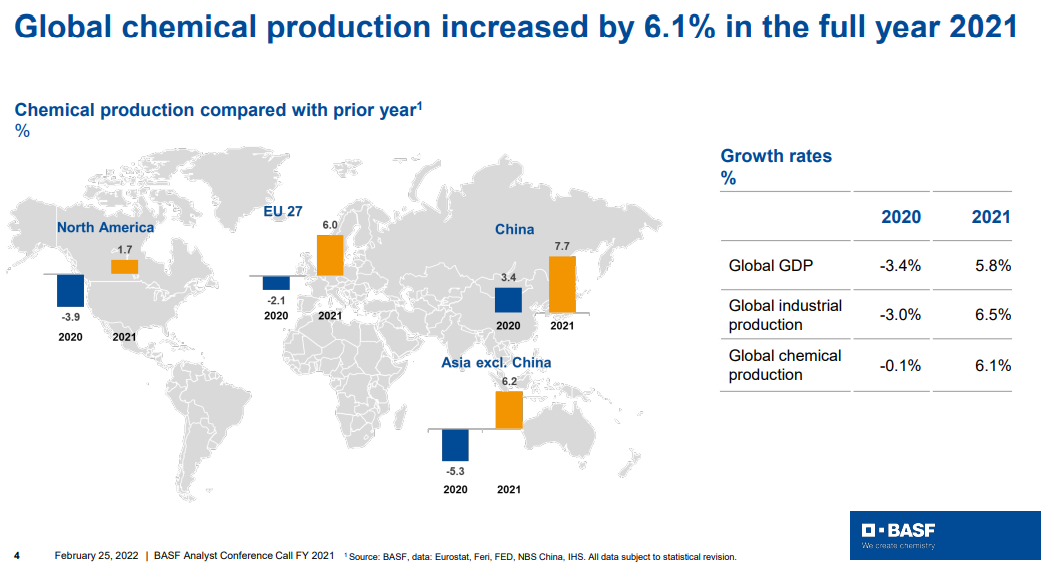

Fear of shortages is the one factor that is most supportive in terms of helping to push through pricing and the events in Europe and their associated impact on energy prices should be all the support that the chemical and polymer industry needs to push pricing through that will cover cost inflation. Buyers of raw materials and intermediate products will naturally look to buy a little more than they need in the near term, both to ensure that they get something ad to try to build a bigger inventory cushion. This will have the effect of pushing apparent demand higher, making the pricing initiatives easier. Few will push back on pricing if their primary concern is availability. Looking at the BASF results summarized in the chart below, demand is already very robust and this will lead to higher utilization rates and higher volumes for chemical producers as well as high pricing. The commodity producers are likely more interesting here as they can move prices much more quickly than the specialty companies who might see margins squeezed over the next couple of months. None of this is good for inflation. See more in today's daily report.

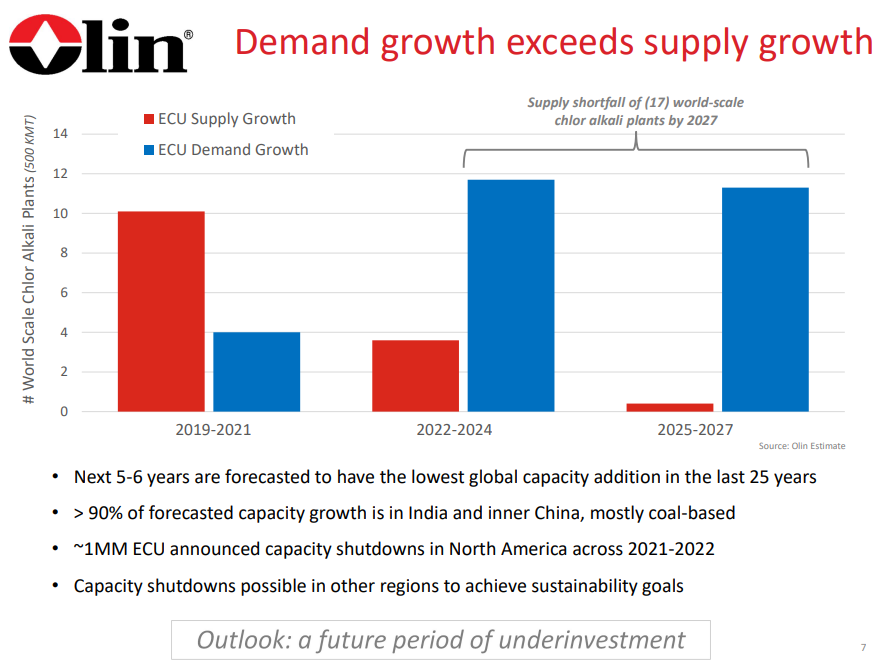

We are already seeing the impact of ESG-pressure related underinvestment in many commodities, and the picture that Olin paints around chlor-alkali is not dissimilar to some of the analyses that could be done around some metals today – especially those that are critically important to the EV, Solar, and Wind industries – this is a topic that we have covered at length. While chlor-alkali may be a pressing very near-term example of how underinvestment could impact chemicals, we suspect that the issue may be much broader, just not yet apparent in other sectors because of the wave of new investment from 2017 through 2022. The polyethylene equivalent chart to the one below would show more balanced supply/demand in the 22 – 24 period than for chlor-alkali but the same deficit thereafter. Many of the other base chemicals would look the same. This supports our expectation of an industry mega-cycle, possibly starting as early as 2023. Of course, there is time to add new capacity by 2025/26, but most companies are more focused today on how they comply with tighter environmental standards today than they are on their next expansion. Further hindering new expansion-driven capital investment decisions is the uncertainty around polymer demand (how much will be recycled, will there be more bans, will there be a substitution from other materials). Our view is that base polymer demand will continue to grow and that we will run short as a consequence of underinvestment. See our report titled - Waiting For The Big One – Is A Chemical Mega-Cycle Ahead?

We have covered some of our Huntsman logic in today's daily report, but we would like to point out another concern that we find with Starboard’s proposal – the focus on operations and the nomination of Jim Gallogly as a potential board member. While we have nothing but great respect for Mr. Gallogly, and the work he did at LyondellBasell, we are concerned that Huntsman’s business model would not be best served with a “larger than life” board member with a very strong commodity background. We have seen several significant mistakes made in the past by commodity-minded companies and leadership, applying somewhat linear thinking to acquired businesses and we believe this could be a risk here. When Dow acquired Rohm and Haas one of the few mistakes that were made was looking at the acrylic acid business like a commodity and trying to drive more production through the units. The effect was to oversupply the markets and depress pricing and margins and it took a couple of years for the right management team to get the business back on track. Huntsman likely does not need more polyurethane and epoxy production if doing so creates a race to the bottom with competitors and destroys margins. The intermediate and specialty chemical business is as much about matching supply to demand as it is about plant throughput and efficiency. Every company can improve its operations and improve efficiency and costs but for some businesses, more material is not necessarily better. We believe that Huntsman’s stock would react negatively if the strategy changed to one of pushing as much volume as possible.

Another Lesson From The Past: Costs Will Matter

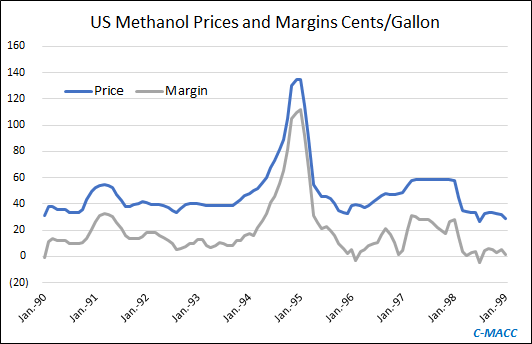

High prices are spurring behavioral changes throughout the supply chain. Per our analysis, it is causing buyers to look for alternatives and ways to use less material and increasing interest in new production, often without much thought about relative cost. In Exhibit 1 (from yesterday's report), we show the methanol peak of the mid-90s. This development resulted from supply shortages rather than high costs. It encouraged multiple projects to receive serious consideration – including methanol from wood chips – where costs looked good at the time but not on a historical basis, and as the chart shows, not on a forward basis. Most ideas never got past the planning stage. With sustainability driving a significant share of the growth investment decisions, we think several “renewable” ideas could encourage investment that rely on price premiums to keep returns attractive. While this setting might look supported today, it will likely look less tenable if traditional commodity prices retreat into a commodity trough or lower-cost competitive materials emerge.

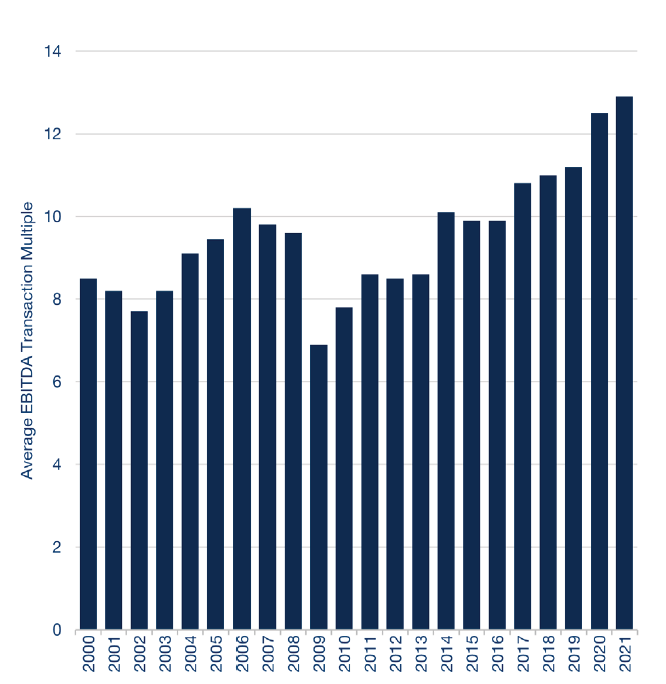

Our Sunday Thematic research a week ago (see linked report) discussed slowing growth investment in the traditional commodity chemical industry and suggested that ESG and climate pressures might slow investment even further. Yesterday, our Sunday Thematic made the argument that some of those dollars will target strategic M&A. We have recently seen an uptick in global chemicals sector M&A, and we find few items suggesting activity levels will slow in the near-to-medium term. In part, we think strategic M&A will be easier to get Board approval for than “new build” capacity additions, and it can be viewed as better use than holding cash or complementary to dividends and buybacks. Also, ESG and climate concerns could spur M&A activity, as companies look to separate bad emission assets from good ones – especially if the market values them very differently.

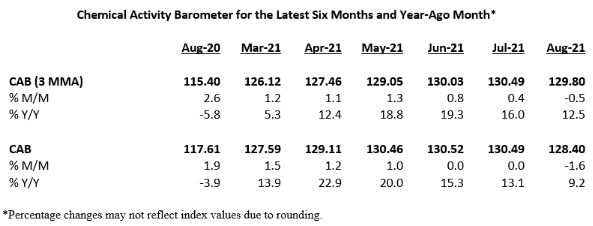

The ACC “chemical activity barometer” shown in the exhibit below is more impressive when you consider that by August of last year the demand recovery was in full swing and operating rates were high. There was some negative impact from the first hurricane, but this hit very late in August 2020 and would not have influenced the ACC reported activity significantly. We focus on price and margin in most of our commodity commentary and this is appropriate, given how much more important they are than incremental volume for all commodities, but it is worth noting that all of the chemical producers get decent cash flow gains from uninterrupted high (optimal) operating rates. The last two years have been a little plagued by more than expected unplanned stoppages, and this has helped keep the US market buoyant, but those that have been able to run at optimized rates for prolonged periods are benefiting. Prices have been the biggest contributor for Dow and ExxonMobil on the integrated polyethylene front in the US this year, but both have had the benefit of very strong operating performance, as have most others with a bias to Texas. Dow and ExxonMobil have large facilities that were in the path of Ida. LyondellBasell and CP Chem do not. See our daily report for more.

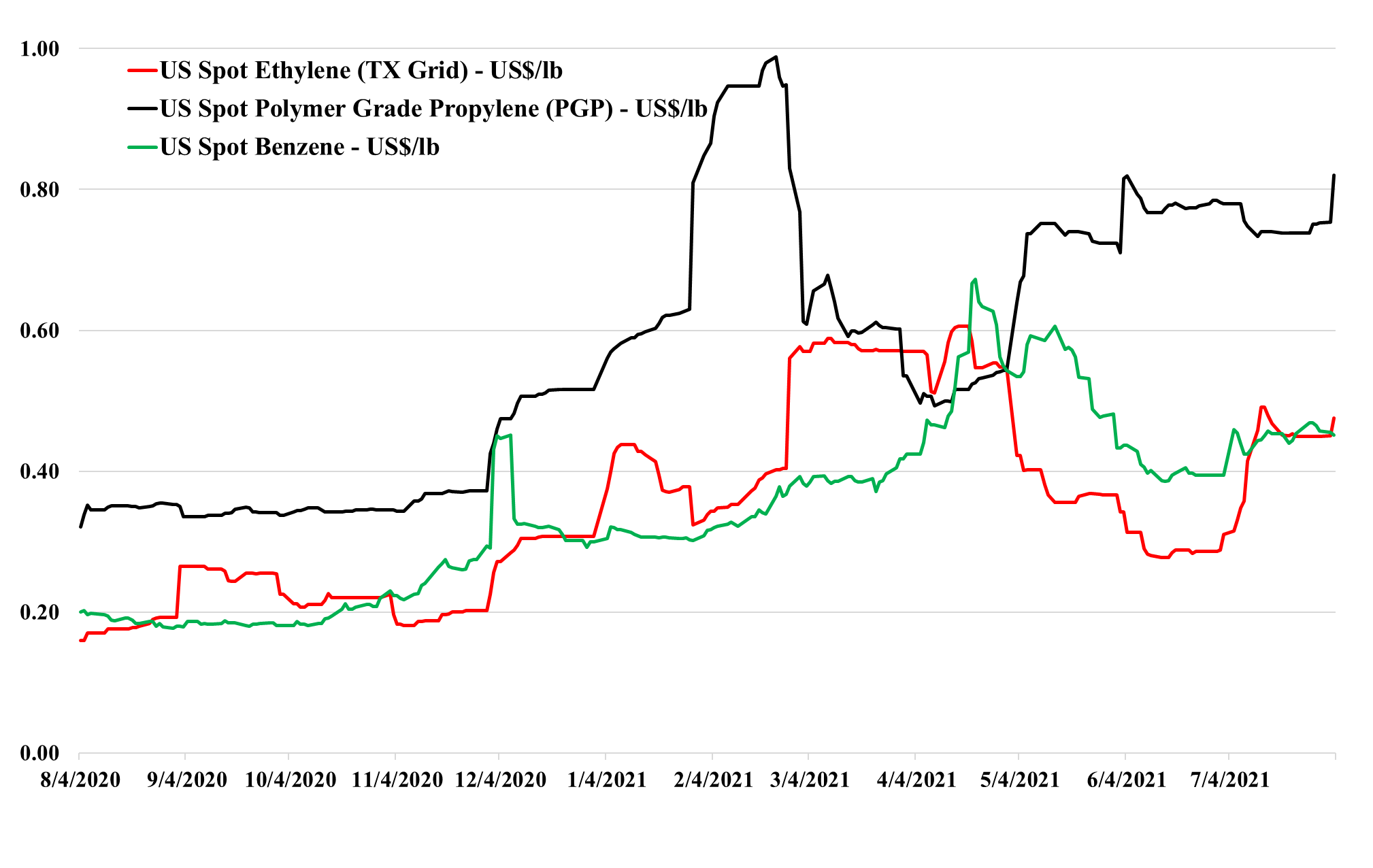

If this commodity cycle has the same drivers as prior cycles, producers like LyondellBasell and others will make comments like “stronger of longer” until prices turn, and if history is any guide, that turn will catch everyone by surprise, and even if it does not, there is no upside for any producer in predicting its end. As with all commodities, markets are tight until they are not, and markets are long until they are not. If you look at the ethylene and propylene price movements in the exhibit below you can see the speed of change that is possible and while the slope may be less severe for polymers in both directions, it can still be abrupt. The worst-case for the US industry would be a step down in demand coincident with the rising natural gas trend. There is no evidence of demand weakness today, but there will not be until it is happening. The extraordinary incremental freight rates shown in Exhibit 1 of today's daily report, make it increasingly unlikely that anyone sitting on surplus polyethylene or polypropylene in Asia can exploit the regional price difference. When demand and sentiment around supply chains turn, we would expect this spot shipping rate to collapse also – but there is no sign of that today.