Our latest Sunday Thematic report, "Damned if you Dow and Damned if you Down’t. Hard to win", centers around Dow's announced development of a new net-zero carbon emissions site in Alberta, Canada. It discusses company-specific and sector ramifications for Dow's strategic move to produce low-cost low carbon polyethylene in Canada while also expanding capacity.

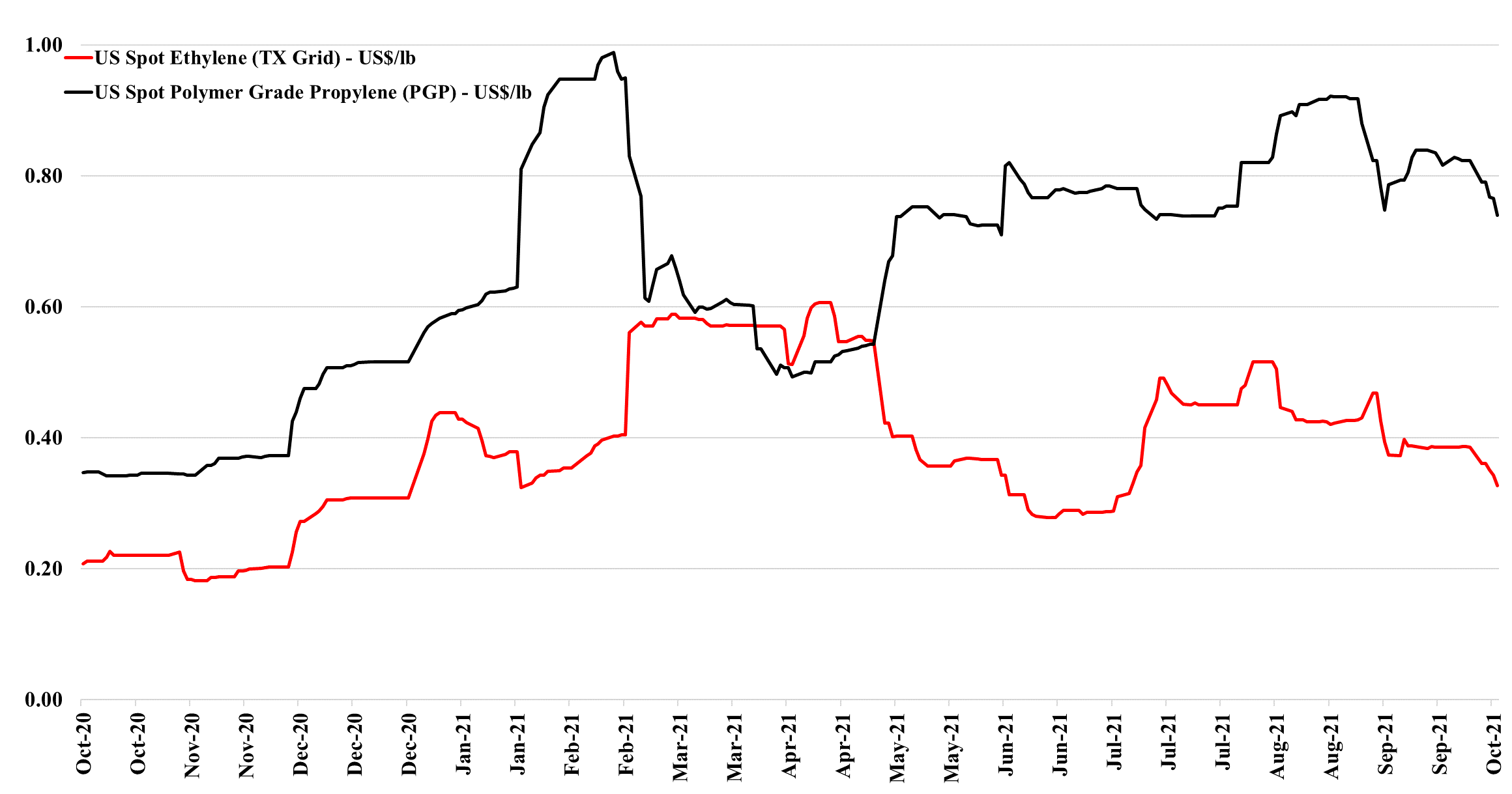

While we will talk more about the Dow project in Alberta on Sunday, one of the problems that the stock faces in the light of the announcement is largely unrelated, which is the growing expectation that margins in 2022 will be significantly lower than in 2021. This is the view coming out of the recent EPCA meeting and as the ethylene/propylene chart below shows, monomer pricing is already weakening in the US as production ramps back up following the recent storms – we note in Exhibit 1 from today's daily report the squeeze on ethylene margins as prices fall, while costs rise. But it is also worth noting that margins remain quite healthy, while well below their highs. Those companies who built new ethylene capacity in the US over the last 5 years would have had a margin similar to the current level shown in Exhibit 1 in an optimistic capital case.

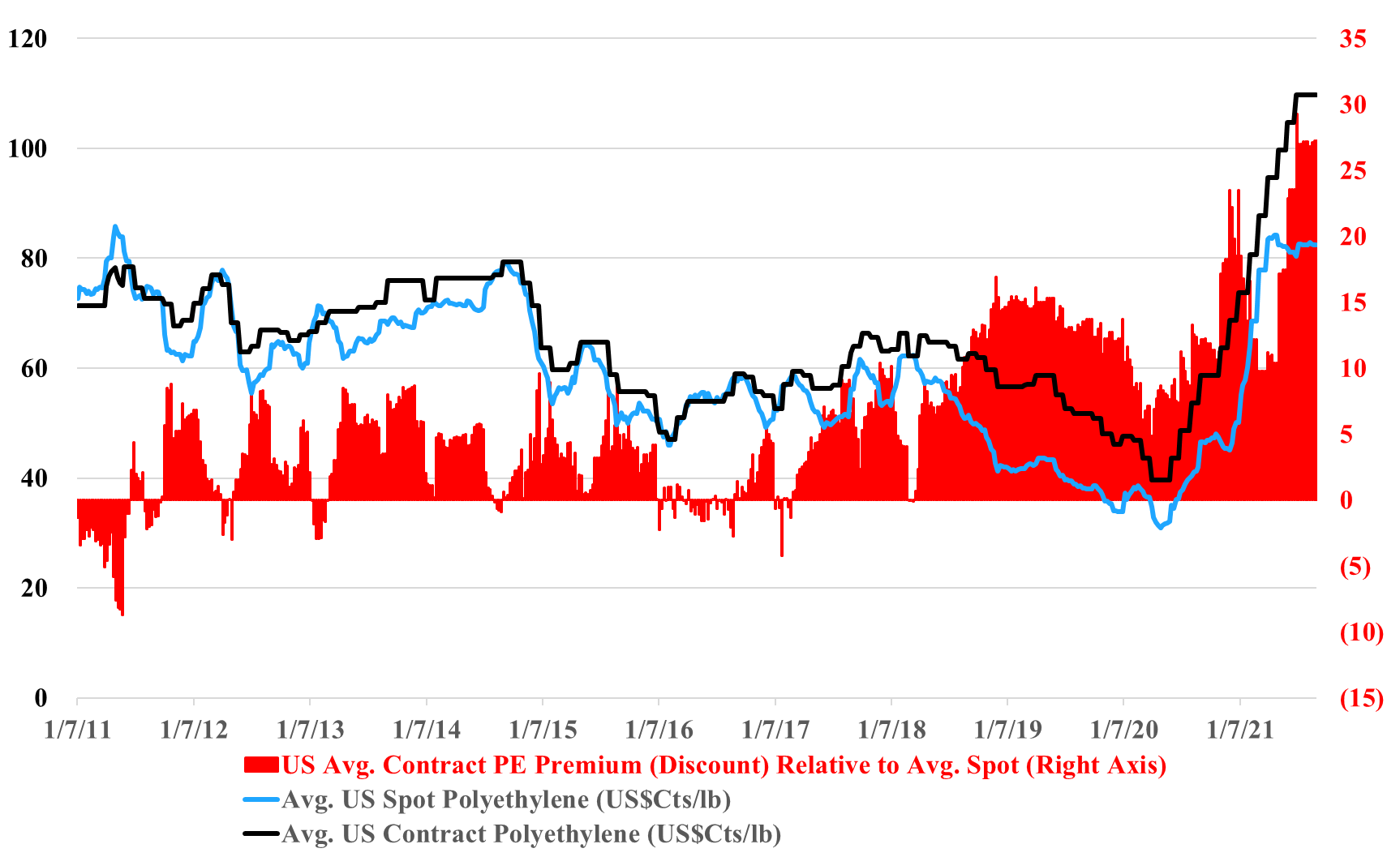

The gap between the US contract and spot price for polyethylene in the exhibit below looks wrong, and it could be wrong in absolute terms but the trend alone makes a statement. In the past, we have seen a couple of instances where reported contract settlements have drifted further from net transaction prices, either because of larger agreed discounts or because of contract formulae that reflect spot pricing to a greater degree. This tends to work for a while, but ultimately smaller buyers with more limited purchasing power become more disadvantaged and there is a breaking point at which the “contract” price is adjusted downwards by the price reporting services to better reflect what is really going on. The current market feels like the times in the past when an adjustment has been needed.

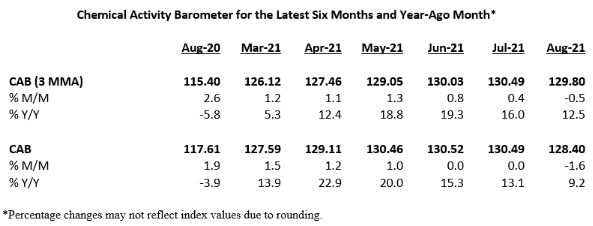

The ACC “chemical activity barometer” shown in the exhibit below is more impressive when you consider that by August of last year the demand recovery was in full swing and operating rates were high. There was some negative impact from the first hurricane, but this hit very late in August 2020 and would not have influenced the ACC reported activity significantly. We focus on price and margin in most of our commodity commentary and this is appropriate, given how much more important they are than incremental volume for all commodities, but it is worth noting that all of the chemical producers get decent cash flow gains from uninterrupted high (optimal) operating rates. The last two years have been a little plagued by more than expected unplanned stoppages, and this has helped keep the US market buoyant, but those that have been able to run at optimized rates for prolonged periods are benefiting. Prices have been the biggest contributor for Dow and ExxonMobil on the integrated polyethylene front in the US this year, but both have had the benefit of very strong operating performance, as have most others with a bias to Texas. Dow and ExxonMobil have large facilities that were in the path of Ida. LyondellBasell and CP Chem do not. See our daily report for more.

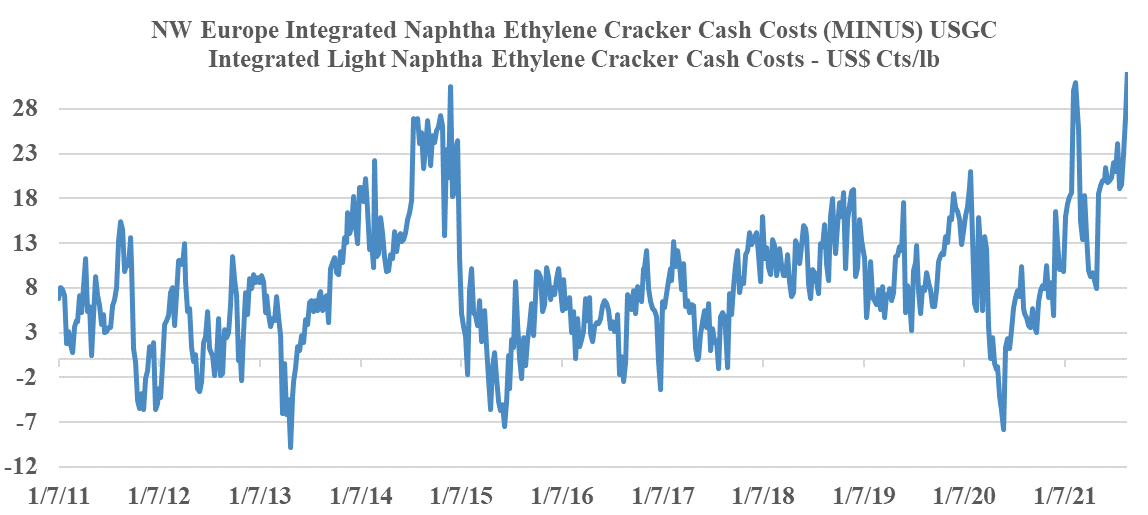

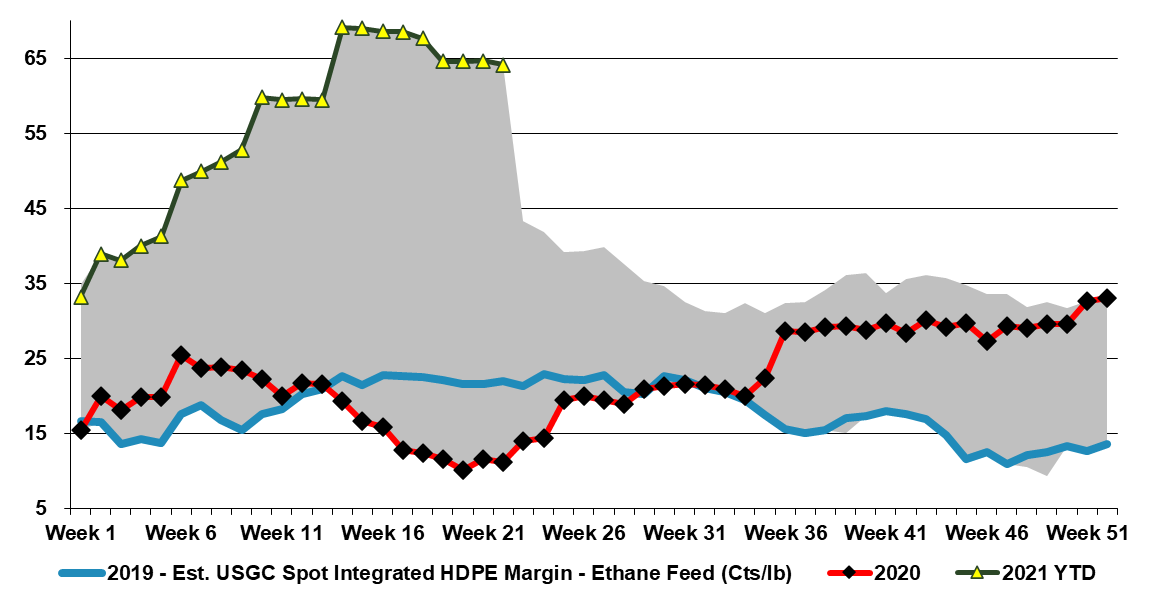

Before the wave on new ethylene capacity came online in the US there were several low-cost expansion projects all of which added the ability to crack ethane and some of which brought constraints around feedstock flexibility. Consequently, it is less clear than it used to be just how much US ethylene capacity can flex to exploit the very attractive light naphtha economics today. Very conservatively, we would estimate that 5-6 million tons of capacity can flex easily and about the same again with some planning and some logistic adjustments. Among the public companies, both Dow and LyondellBasell are well placed, and likely have at least 1 million tons each of flexible capacity – in both cases, there is a need for propylene and LyondellBasell has significant butadiene/C4s capacity. For context, at current prices, both companies are likely looking at an additional ethylene margin benefit in the US of $2.5-3.0 million per week for as long as this opportunity exists. This would be 0.3 cents per share per week for Dow and 0.7 cents per share per week for LyondellBasell – a rounding error in current earning but more free cash regardless. The chart below shows the unprecedented benefit in the US and see our daily report for more.

ExxonMobil Chemicals has announced that its Corpus Christi JV project with SABIC is ahead of its original schedule – ExxonMobil is now targeting a start-up in 2H21, ahead of its previously targeted 1H22 expectation. It is unusual for projects in the US to be ready ahead of schedule these days, and start-up delays tend to be the norm. We also take a positive view of this development upon comparison to the Shell Pennsylvania project, which still has a vague 2022 start-up expectation though its construction began before ExxonMobil. One could argue that the remoteness of the location – well away from petrochemical infrastructure has been a constraint for Shell, but the Corpus Christi location is also a greenfield project for ExxonMobil/SABIC. This will be the largest ethylene plant built in the US, though it is likely that the recent 1.5 million ton units (Dow, ExxonMobil, CP Chem) are expandable to 2.0 million tons. Dow is already discussing such a move with a new polyethylene facility at Freeport. It will be interesting to see what impact this ExxonMobil/SABIC facility has on both the USGC ethane market and the polyethylene market – 1.3 million tons of polyethylene is a large increment and SABIC will have half of the capacity and will be a new market entrant with on-shore production. Aramco has ethylene, through Motiva’s purchase of Flint Hills, and SABIC owns half of the Cosmar styrene plant in Louisiana.

The ExxonMobil board headline linked has come up a couple of times since the Engine No.1 victory at the board meeting. There is no doubt that capital spending plans will be reviewed with the changes at the top, and we expect more management changes, which could also drive spending priorities. Over the last couple of years, several more macro studies have been done talking about oil demand in a climate change-centric world and all have highlighted chemicals as one of the likely longer-term growth avenues for fossil fuels. We would expect ExxonMobil and other oil majors to look at investments in chemicals as a route to more captive consumption of hydrocarbons and believe that this could ultimately keep basic chemical and polymer markets oversupplied through the balance of this decade – we have been writing about this risk consistently since early 2020. ExxonMobil is already building ethylene capacity in the US in a JV with SABIC, but more oil company investments could come in the US. The caveat is that, as Dow covered in its MDI press release yesterday, any new investment is likely to need a carbon plan to get stakeholder and regulatory approval.

The Dow announcement yesterday speaks to a much larger issue within the investment community in our view, which is that research fees have come down so much over the last ten years that the sell-side gets paid very little for doing any real research. We talked about the upside in 2Q for the commodity polymer producers for months. Still, we know that we cannot get paid for maintaining the models needed to get to the numbers with enough confidence to publish estimates. The buy-side does not have the budget. In the past, as sell-side analysts, we would subscribe and talk to price discovery consultants, such as the predecessor companies of IHS (now in the middle of an acquisition by S&P) and CDI (in the middle of a merger with ICIS). This data and these dialogues would allow us to adjust earnings estimates during the quarter and keep up alongside our other work (e.g. corporate marketing/roadshows, etc.) as analysts. There is enough data in our weekly report – published each Monday to do this for many companies. (See an example in the chart below). Today, IHS has made its service so expensive that it is difficult for sell-side analysts to justify the cost when they are not getting paid by clients for real, fundamental research. The JP Morgan alleged base fee for research for an entire platform would not cover 25% of the IHS subscription cost for olefins and polyolefins data alone, per our estimate. Plus, all the merger activity at the data providers is causing some to question quality. The result is limited mid-quarter analysis from the sell-side and moves like Dow’s so that they can have realistic conversations with investors. In the case of Dow, it was to get the message out ahead of the Bernstein Conference.