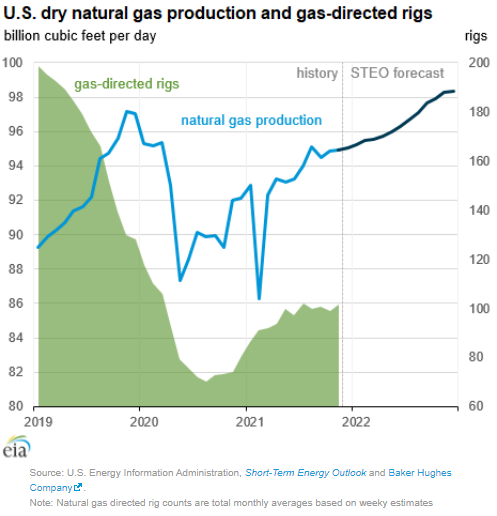

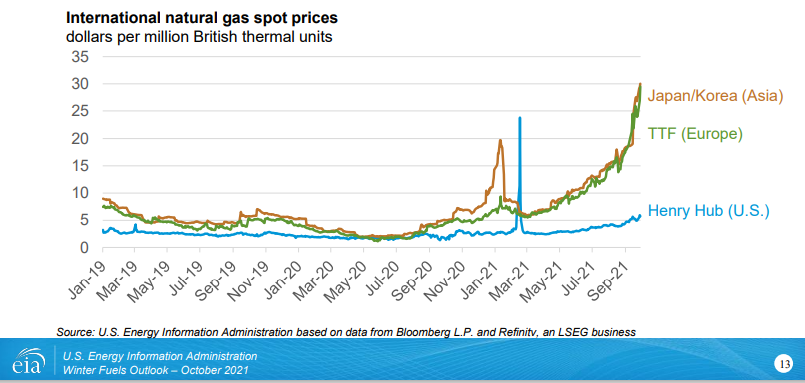

The theme of our Sunday report (to be found here) will be inflation this week and the signs that we are seeing across multiple industries which suggest it could be more problematic and worsen in 2022. One of the focuses is energy and how the pressures to be seen as good citizens is lowering investment in oil and natural gas production, while the world is not far enough advanced on energy transition to be able to substitute for the missing hydrocarbons. We would agree with many of the recent comments from some segments of congress, which is that the answer is not to curtail exports of LNG and crude, as by doing so we will starve the rest of the world of hydrocarbons and create worse shortages than Europe and China are seeing today. The better solution would be to support “clean” US production of the lowest emission fuels possible – especially for natural gas. As we have noted in prior research, with a global solutions hat on, the relatively low costs of natural gas F&D costs in the US, when combined with what we expect to be relatively low costs of emission abatement in the US, should drive more investment in the US, creating jobs and export income.

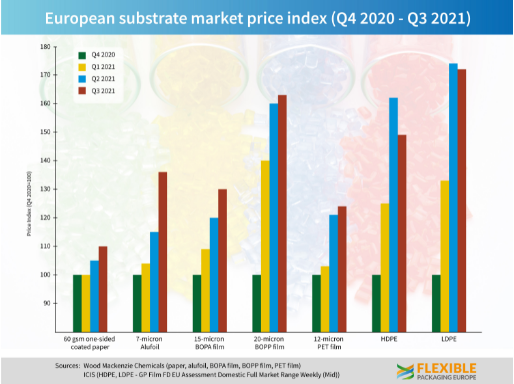

Focusing on a theme from our daily report today and our ESG report yesterday, the cost pressures in Europe are very real, and the more the power or natural gas component to your costs the more the pain and the more important it will be to raise prices. The industry and consumers, in general, have not had to deal with significant inflation for decades and it is very easy for customers to push back with a “this is transitory” argument, especially when many governments are telling that story. The supply chain is to blame to a degree, but it is largely a symptom of the underlying cause, which is that demand has outstripped supply. It is easy and more palatable to try and brush it off as temporary, but if the energy price issues persist in Europe and China and companies are not successful in passing on prices they will, at some point, choose not to operate. Alternatively, if power shortages are enough to cause interruptions, industrial users may have no choice but to close down. All this will impact product availability and buyers pushing back on price increases could find themselves without supply which is generally worse than paying more. The European packaging industry is right to raise the flag around higher prices, but their customers will pay the increases needed to ensure that they can keep operating, even if the discussions are more challenging than they have needed to be for the last 30 years.

The linked article looks at the chemical inflationary cycle of the 70s, which has some relevant indicators for what we are seeing today, but there were also some stark differences. Rising raw material prices is a common theme and while it is convenient to blame OPEC+ this time, the group is not nearly as much to blame today as it was in the 70s. Consumers were facing not just higher oil prices, but also genuine shortages because of the OPEC cutbacks and the multi-year lead times that it took non-OPEC producers to ramp up E&P and ultimately production. This time the oil is there and relatively easy to get to, especially in the US, but the capital spending decisions of the US oil producers – mostly because of ESG related pressure – are holding back the production.

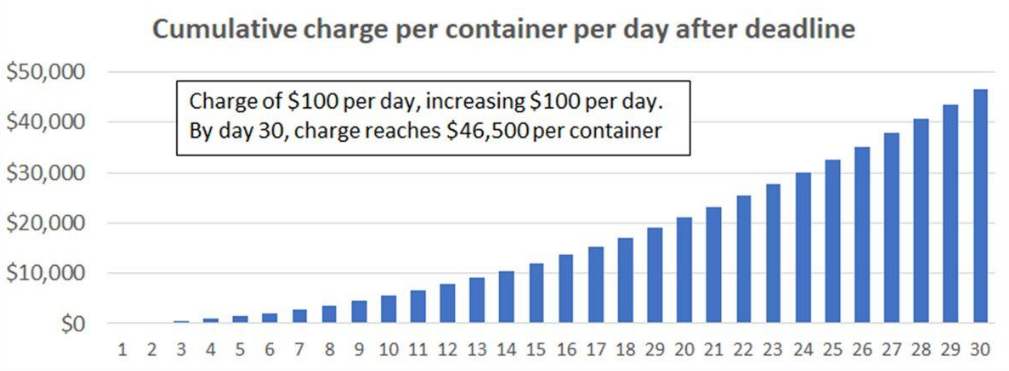

Shipping rates are falling steeply but we are not out of the logistic woods yet with the Ports of Los Angeles and Long Beach proposing very punitive charges for containers that are not collected quickly enough. The initiative is intended to decrease bottlenecks at the ports by clearing the docksides more quickly, but the reason why there are delays is often out of the shippers' and buyers’ hands as it is a lack of truck drivers and rail capacity that is at issue. The penalty rates proposed are steep and might discourage some shipments – especially of polymers and other low-value products. If it takes you an extra 20 days to offload a container from the port the cost of shipping polymers from Asia would double – very few importers would take that risk given the small margin opportunity that exists in the trade already. The penalties might encourage trucking companies to increase driver compensation to attract more drivers, but only if they can pass the potential penalty through to their customers. While this move proposed for containers may help drive down some of the port congestion times it is not a good sign for inflation as someone will have to pay – either pay the fines or pay up to improve resources to clear the containers more quickly.

There are lots of discussions around the durability of higher energy prices and energy inflation is a central topic on some earnings conference calls and in many of our discussions with clients, especially those at chemical companies with the unfortunate task of having to prepare a 2022 budget, which of course includes a forecast of costs. We see continuing strain on the US and global natural gas system and, behind what will inevitably be some seasonal weather-related price volatility, a stronger market that could endure for years. The rate of addition of renewable power does not seem to be able to keep up with demand growth and replacement needs caused by some fossil fuel-based power plant closures around the World. Natural gas (LNG) is the natural plug-in replacement, and we continue to see underinvestment, relative to natural gas prices, as a consequence of ESG related pressure around capital spending. We would advise all clients to look at a 2022 scenario with natural gas, and oil higher than current levels.

The commentary on oil reflects the opposing views that OPEC+ capacity is looming and that every piece of incremental negative demand news is frightening, versus that OPEC+ is disciplined and wants higher prices, resulting in every incremental positive being welcomed. We are firmly on the side of higher oil prices as we cannot see any stakeholder in oil wanting anything except opportunity profits for as long as it may last from here.

The concerns about supply chain inflation hurting chemical demand are likely very end-use specific. While the packagers and consumer goods sellers are seeing significant inflation in all raw materials, not just polymers, the packaging is a minor component of the cost and value of what they are selling and while it may hurt their earnings, it is unlikely to stifle demand – none of us is likely to stop buying milk, orange juice or cookies if the prices rise a couple of cents because the manufacturers are trying to cover some of their higher costs.