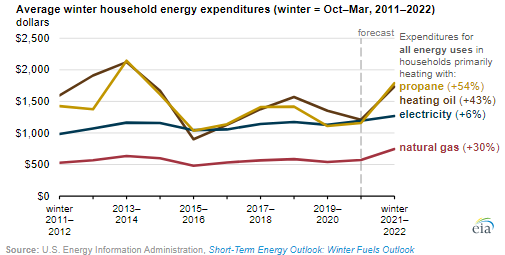

At this point, it has stopped being a story about how transient higher energy prices might be and instead become a story of how high could they go as well as how long the higher prices could last. With sentiment easing in the US because of an expected milder October, we also have the headline of the restart of Cove Point LNG, which should add to natural gas demand. The EIA, in the chart below, shows US prices peaking through the end of the year before falling again in early 2022. There remains an expectation that the rest of the world will be short of LNG and so we will either see the US natural gas competitive advantage remain strong, or the US LNG facilities will stretch their underutilized nameplate capacity and this could be supportive of higher US natural gas prices. New LNG capacity does not hit until late 2022 and how much is exported until them will be a function of the throughput of the existing terminals – which today look like they were very prudent investments.

With the rapid rise in energy prices, we are seeing price increase announcements for many intermediate chemicals, especially in regions of the world where margins were already very slim. The energy inflation issue is hard to call, with more and more commentators suggesting that it could be prolonged (which generally means it will be short), but lots of dislocations support duration. We would certainly be pushing prices today on the back of energy costs that could move higher again, and given that many chemical and polymer buyers have price protection in their contracts (for at least a month), producers could face a margin squeeze and an uphill climb to get adequate price coverage. Seasonally, demand for chemicals and polymers is at its weakest for the next couple of months, so the price hikes may be difficult. However, because of supply chain constraints, buyers may feel less confident and concede more easily. We could see a significant swing in sentiment from the chemical companies on 3Q earnings calls over the coming weeks as they talk about how good results were in 3Q but throw up all sorts of cautionary statements concerning 4Q.

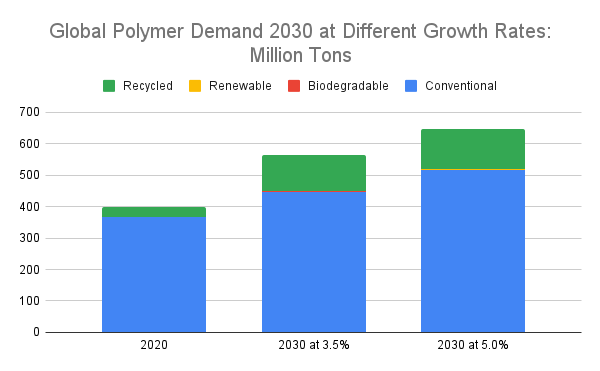

Our latest Sunday Thematic report, "Damned if you Dow and Damned if you Down’t. Hard to win", centers around Dow's announced development of a new net-zero carbon emissions site in Alberta, Canada. It discusses company-specific and sector ramifications for Dow's strategic move to produce low-cost low carbon polyethylene in Canada while also expanding capacity.

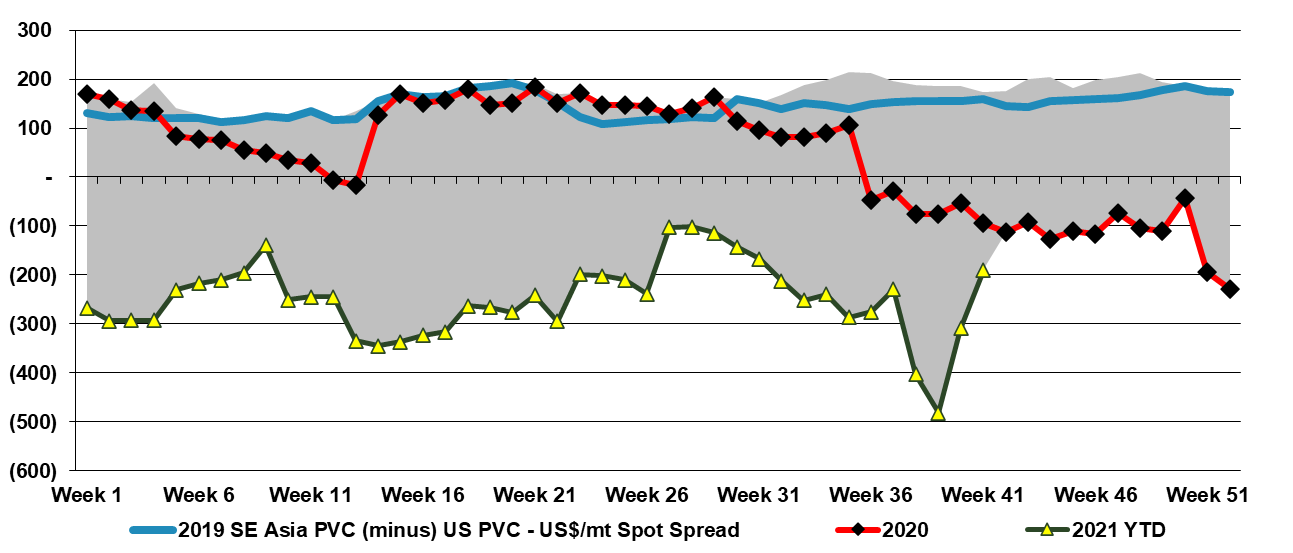

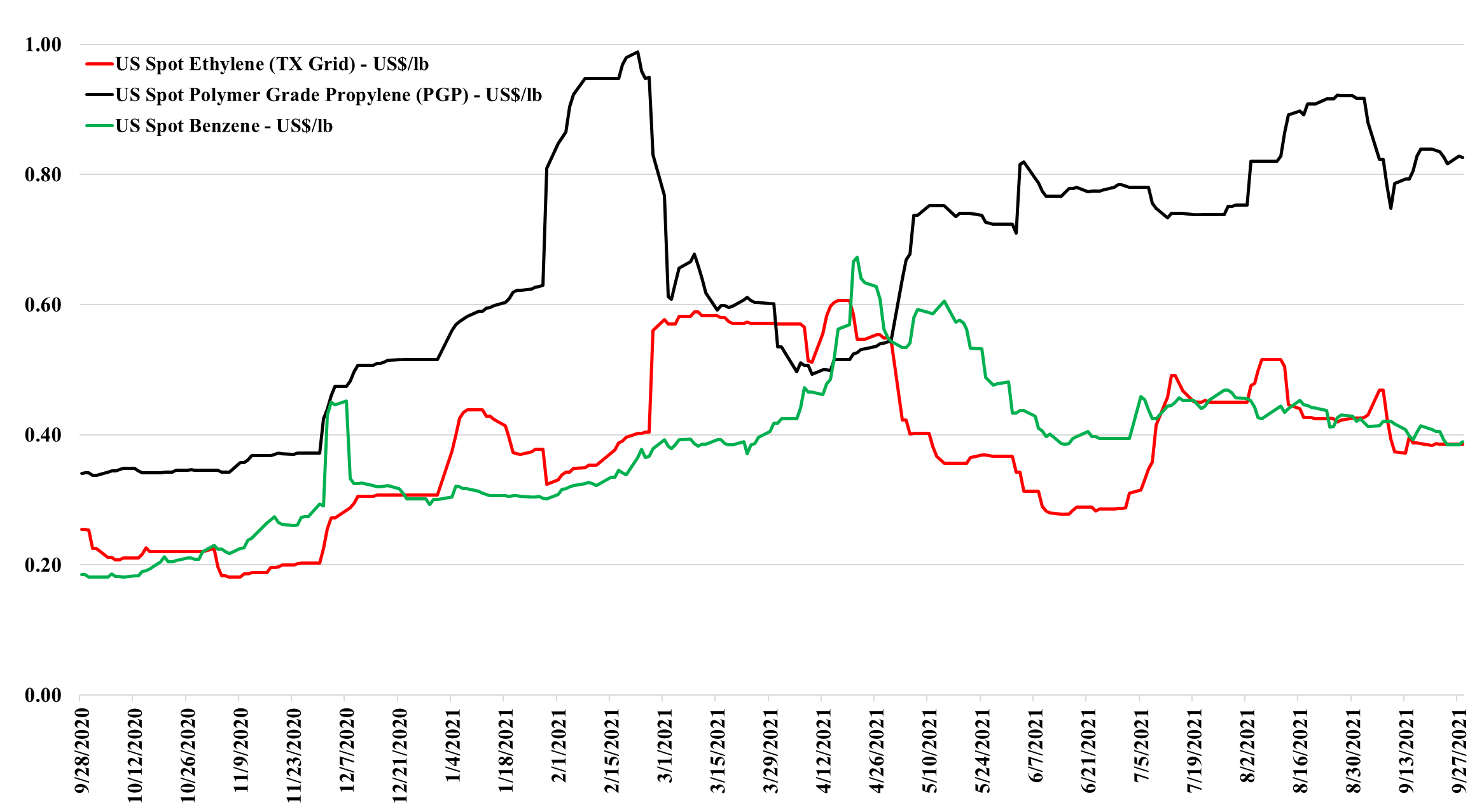

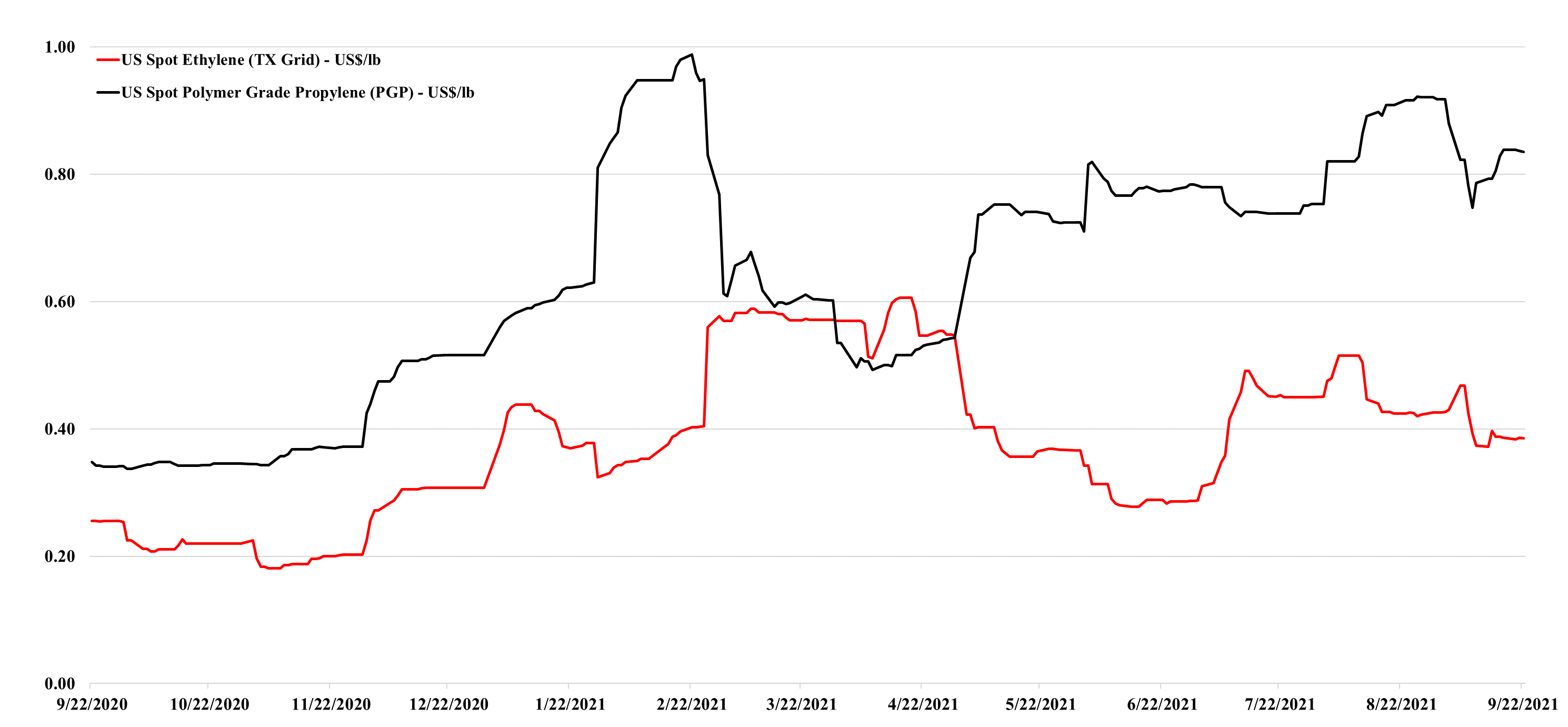

The US petrochemical production cost competitive advantage reflects a sharp decline at the feedstock level. Natural gas and natural gas liquids prices have risen faster than crude oil and Ex-US naphtha values since mid-1H21. In yesterday's report we identified the disconnect between propane and ethane pricing in the US. While both are high, propane is so high that it is now unprofitable to make ethylene from propane instead of just less profitable. The direction of the lines in the exhibit below shows the changing landscape clearly, and the only reason why the US chemical industry is so much more profitable than the markets in Asia is that chemical product prices are so robust, in part because of the high cost of freight between the regions.

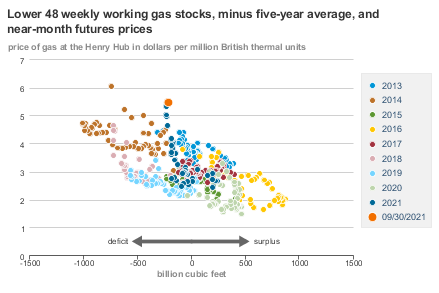

It is a gas, gas, gas! Every other story this week is about natural gas shortages and pricing – whether it is natural gas in the US or LNG everywhere else. The scatter diagram below from the EIA below is very interesting as it speaks of anticipation more than anything else. Gas prices are high given the level of US inventory relative to “normal”. There is speculation that demand is going to outstrip supply over the next few months. Whether much of this will be LNG-related remains to be seen as we may not be able to run the current capacity any faster – that said, through the end of July it looked like there was spare capacity at several of the US LNG facilities and maybe the constraint is shipping. Regardless, the current US price implies shortage, whether because domestic demand overwhelms supply this winter or because LNG steps up. The original timeline of the Venture Global facility at Calcasieu Pass in Louisiana has slipped and this facility will not impact demand for the next 12 months at least, with ExxonMobil’s Golden Pass project a year later and targeting a 2024 start.

We have discussed a theme around shortages that has been going on for months and is prevalent in many of the headlines today. It has also been a central theme of much of our energy transition work, as we think about the raw materials needed to meet the demand for solar and wind power as well as the infrastructure for hydrogen generation. The exception is lithium, where we see regular announcements around expansion projects, such as the one linked from Albemarle. The EV makers and battery storage manufacturers are doing an excellent job of encouraging investment in lithium, taking stakes in battery projects, and in some cases taking stakes in the lithium projects themselves. Offtake agreements also help projects get funding. We suspect that the offtake agreements are tactical – not aimed at buying out a source of lithium or a source of batteries but aimed at ensuring that a surplus of capacity gets built, to ensure no bottlenecks in the future.

The charts below show that North American methanol pricing is seeing support from higher natural gas prices as you would expect, but we are also seeing some significant price improvement in China, See more in today's daily report. If China is coal constrained, as suggested in many of the power-related stories, it may be impacting chemical production from coal at the margin. Alternatively, with LNG prices so high and imported naphtha and propane prices rising in China, the country may be using more coal at the margin to make chemicals.

We have a fairly stable week for US olefins so far – no new production disruptions, but the industry is still recovering from the storm-related shutdowns over the last 4 weeks. We still believe that there is a downside to ethylene and propylene in the US as production recovers and as demand normalizes (especially for propylene). With another month of hurricane season to go, however, it probably does not make sense to force surpluses into an export market where prices are much lower – especially for ethylene. As we have noted in the past, the right strategy in 2020 was to store the ethylene at this time rather than sell it. Inventories would likely have to rise further before those with surpluses were willing to take the cut needed to export. At the same time, rising natural gas and NGL prices are another reason to hold on to products as what you have today did not cost that much to make and costs may rise near term. See more in today's daily report.

The major issue with the higher natural gas prices in Europe (and rising prices globally) is the knock-on inflationary impact it will have on products that have natural gas as a feed, rather than those buying it as a fuel. The fuel buyers will take some of the hit, but will also try to pass on some of the hit, as it is generally a small part of overall product or service costs. The focus has been on ammonia/urea production because of the knock-on effect on food-grade CO2. But other products, such as methanol, would also be impacted, although there is not much methanol capacity in Europe. Higher LNG prices in Asia could encourage more coal-based methanol production, which is precisely what the increased use of LNG was supposed to prevent – replacing a high carbon footprint route with a much lower one. In our view, it is imperative that the attendees of COP26 recognize the need for (cleaner) natural gas and LNG, and enact policies to support it. This inflationary lesson is well-timed.

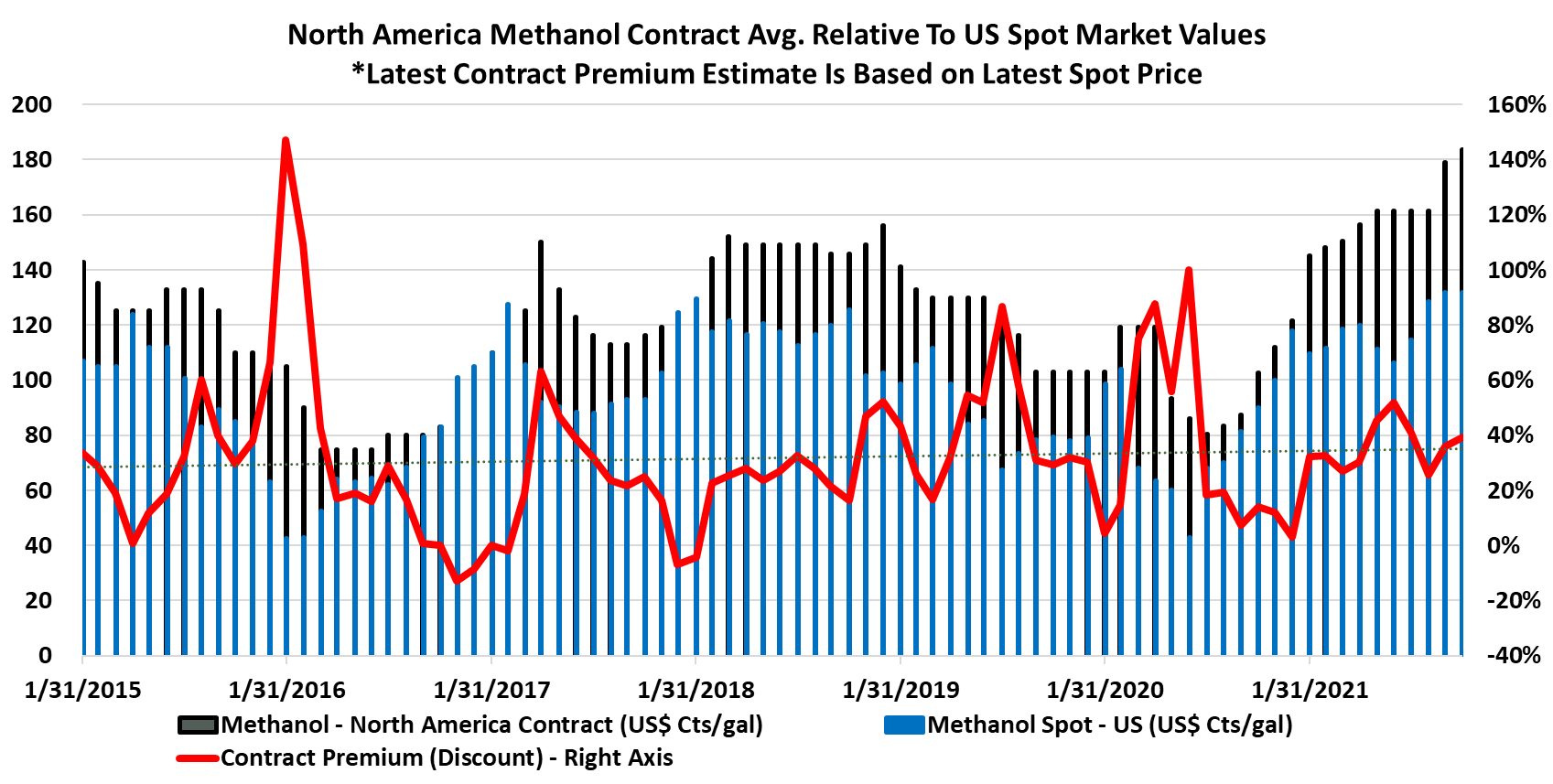

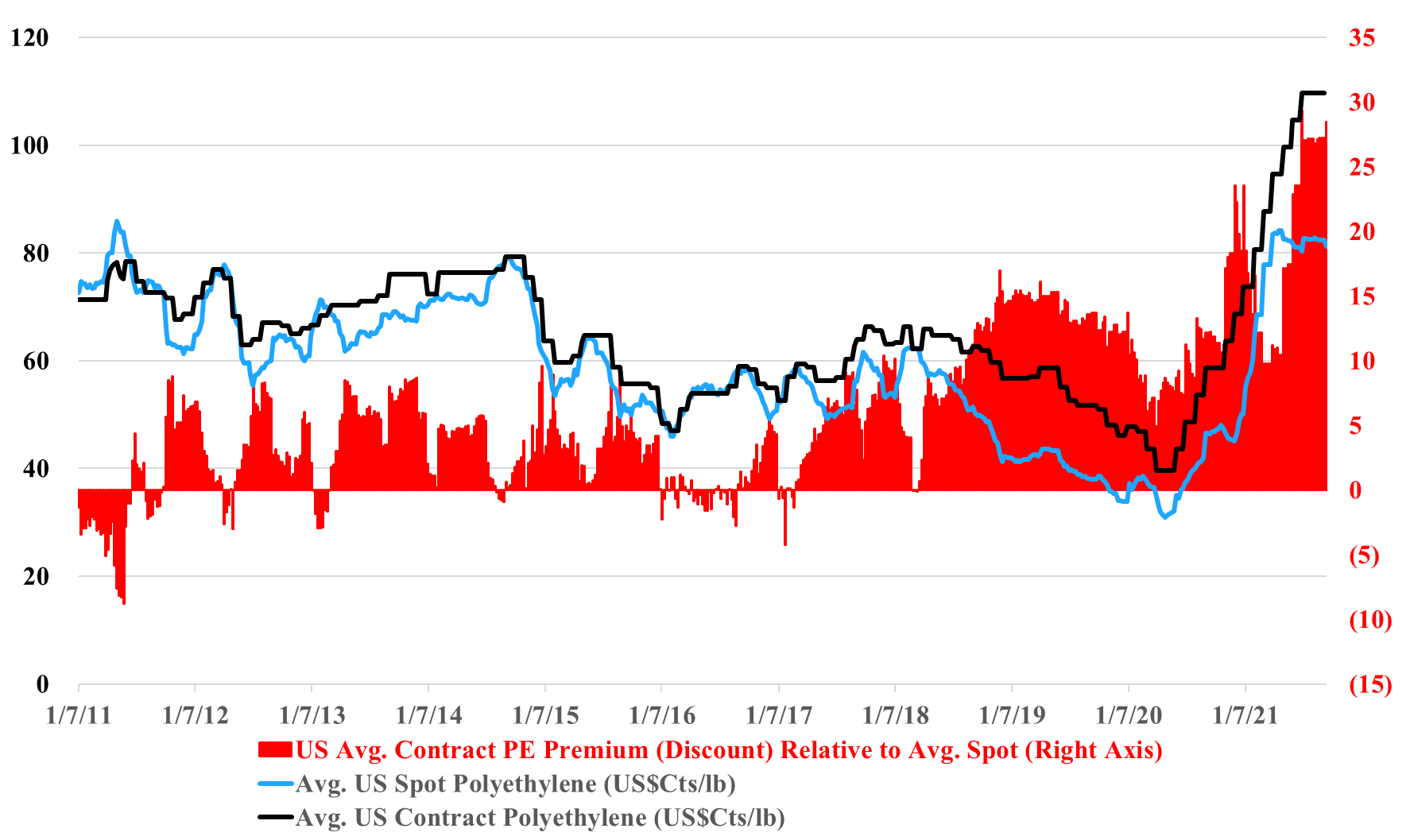

US polyethylene producers are pushing for September price increases and their arguments center around lost production, because of Ida and Nicholas, and rising costs because of the much firmer natural gas and ethane markets. Working against them are the very high margins and what appears to be a stubborn spot market, both covered in the charts below. A contract increase in September would maintain an unprecedented gap between US contract and spot pricing, and while it is likely that the spot market is very thin, it is a very strong push back against producers for a contract hike.