Recent Posts

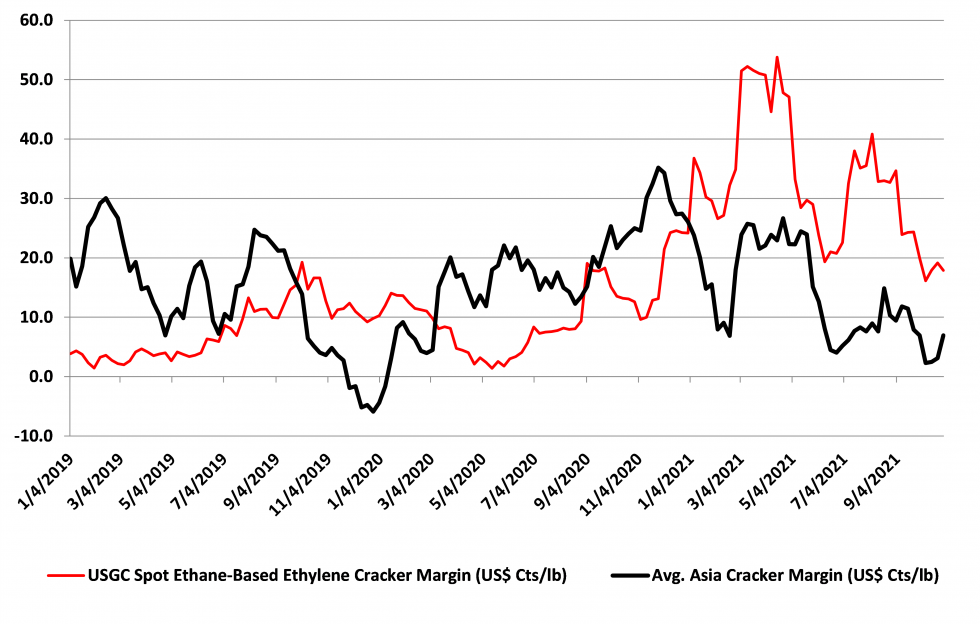

Clearly, as a direct consequence of our shortage theme this week, ExxonMobil announces a large new complex in China is through FID. This may be the company rushing something ahead before tighter restrictions are imposed or it may be an indication that with a 2060 net-zero pledge China is going to let things slide for a while. We would not be surprised to see ExxonMobil face some bad PR around this project if there is not some emission abatement plan with it. The facility will give ExxonMobil some further integration – effectively consuming equity hydrocarbons – but, if the company is setting itself up for criticism for investing in jurisdictions with lower emissions standards, this could backfire. It is also a very counter-cyclical investment given the poor profitability seen in the region right now (chart below) and as we discussed in our Sunday Piece - Waiting For The Big One – Is A Chemical Mega-Cycle Ahead?.

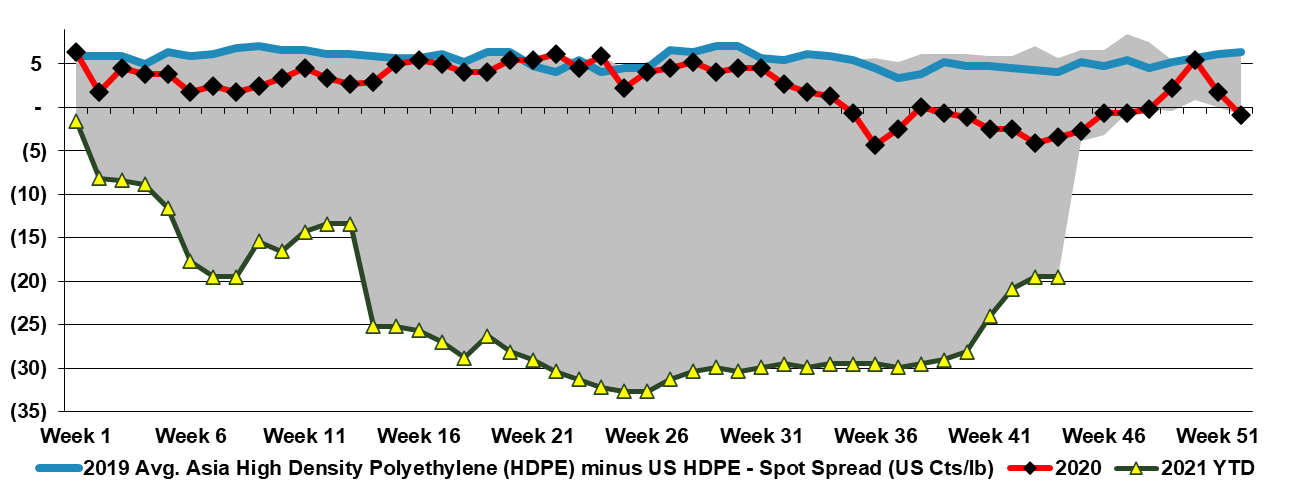

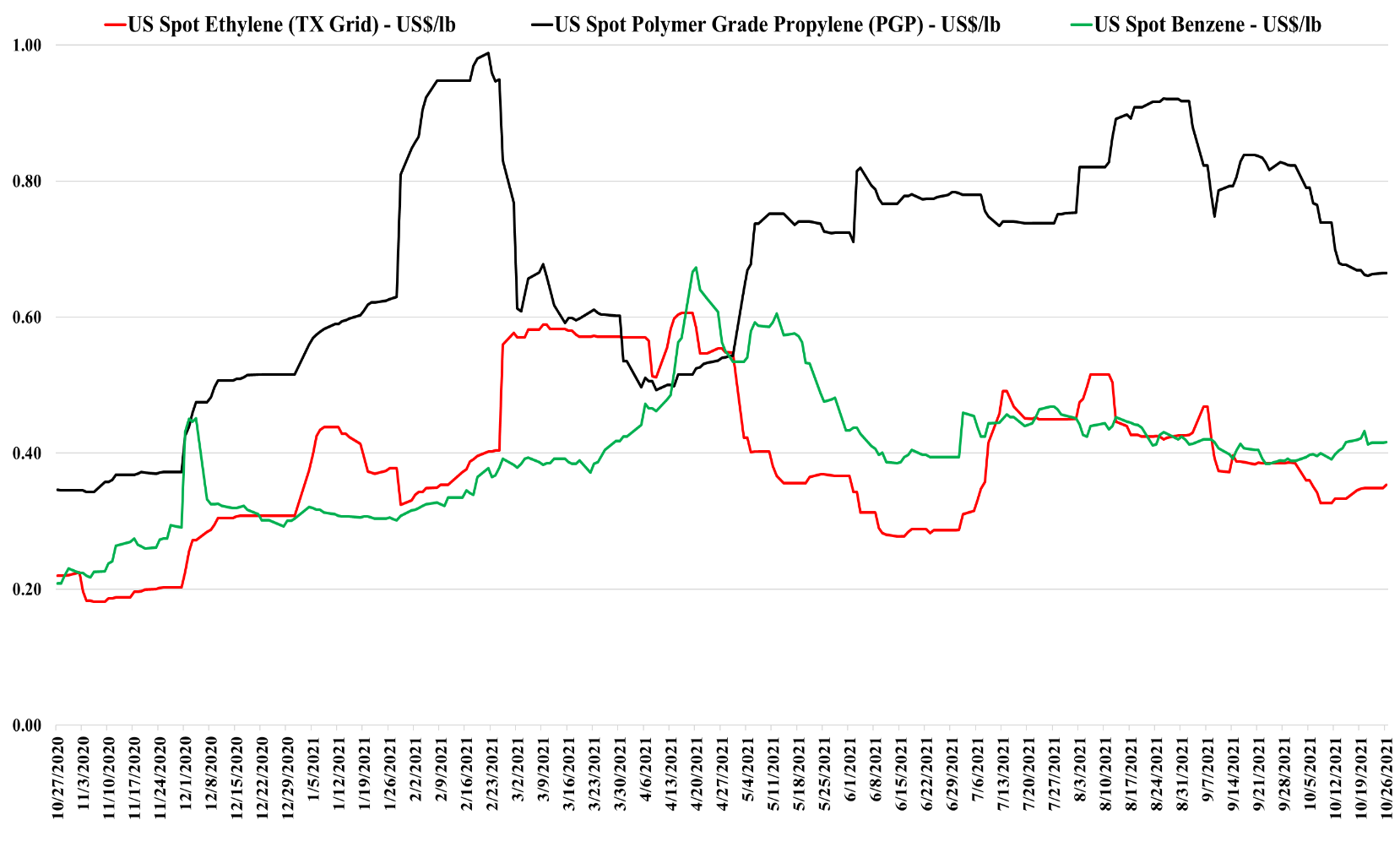

While we are beginning to see some easing in US polyolefin prices we note in today's daily that prices are not falling in step with monomers and so spreads are widening. Because of the very integrated nature of the polyethylene market, we see swings in where the margin is being captured based on relative tightness and today it is squarely biased towards polyethylene in the US. Despite the polymer price declines in the US we maintain a level of pricing that is well above Asia – Exhibit below, but not high enough to attract imports, given the high container rates and the long lead times on shipping. The same is not true for polypropylene, which maintains a spread versus Asia that can cover the very high current costs of transport (bottom exhibit).

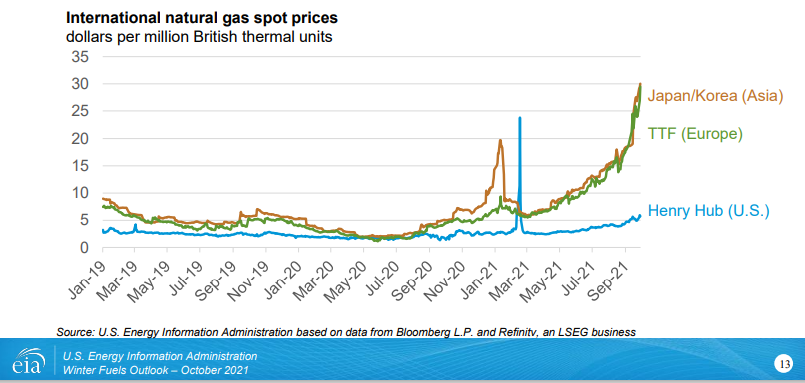

The EU revision to its green energy plans to include both nuclear and natural gas-based power is a direct response to the current energy shortage and price inflation that is evident in the exhibit below. While high natural gas pricing is part of the problem, Europe's renewed willingness to include natural gas in its forward energy planning may drive local investment to produce more gas and foreign investment to provide more LNG. The move indicates that the EU does not see the current natural gas shortage as a short-term issue. The nuclear inclusion is likely aimed at delaying any further planned nuclear closures and we have seen recent delays in closing older US facilities for the same reason - closures will put too much strain on an already challenged power grid and prices for power could be pushed higher by even higher natural gas prices.

We are not surprised by some of the DuPont stories this morning. We had predicted a long time ago that Mr. Breen was far from done on the restructuring of the company and that COVID might have caused a delay in some of the plans but not changed them. Mr. Breen did a very value-enhancing job of taking Tyco from a slightly out of control, then GE wannabe, to a group of focused companies, separated from the whole. What he has panned for DuPont comes from the same playbook in our view. The divestments and acquisitions announced today will create a core at DuPont – focused on electronics, water, protection, industrial technologies, and “next generation” automotive. Given some of the recent industry moves, we would expect significant interest in the engineering polymers and other resins platforms. After these moves are complete, while not yet obvious from a valuation perspective, we could see a further split, carving out an ESG friendly piece focused around water and protection, although the moves announced today may be enough to get the company an earnings multiple boost.

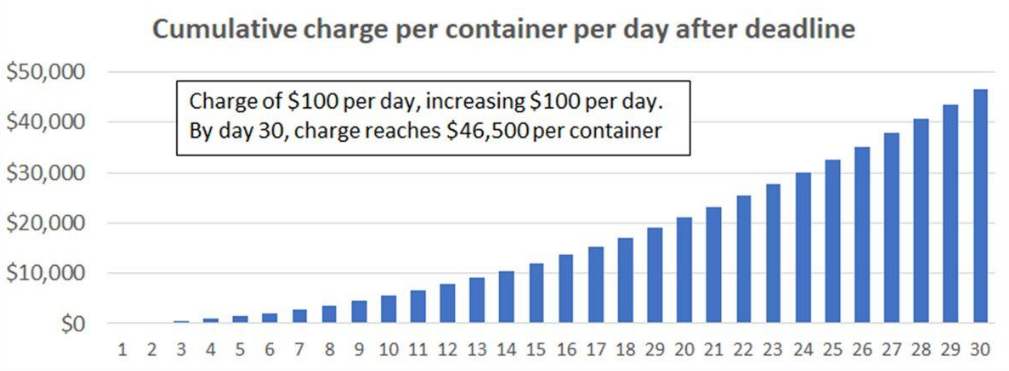

Shipping rates are falling steeply but we are not out of the logistic woods yet with the Ports of Los Angeles and Long Beach proposing very punitive charges for containers that are not collected quickly enough. The initiative is intended to decrease bottlenecks at the ports by clearing the docksides more quickly, but the reason why there are delays is often out of the shippers' and buyers’ hands as it is a lack of truck drivers and rail capacity that is at issue. The penalty rates proposed are steep and might discourage some shipments – especially of polymers and other low-value products. If it takes you an extra 20 days to offload a container from the port the cost of shipping polymers from Asia would double – very few importers would take that risk given the small margin opportunity that exists in the trade already. The penalties might encourage trucking companies to increase driver compensation to attract more drivers, but only if they can pass the potential penalty through to their customers. While this move proposed for containers may help drive down some of the port congestion times it is not a good sign for inflation as someone will have to pay – either pay the fines or pay up to improve resources to clear the containers more quickly.

Global commodity chemicals are often a relative rather than an absolute game, especially where there is significant international trade. The global price of natural gas has risen dramatically, especially in countries or regions where the marginal BTU is coming from imported LNG – see yesterday’s daily report for a comparative chart. The US may be seeing much higher natural gas prices but other parts of the world have it much worse, and with most of its methanol capacity in regions/areas with very competitive natural gas, it is not surprising that Methanex is upbeat. The higher natural gas price in the US is giving Methanex and other US producers the ammunition to raise prices and the higher costs outside the US mean that international volumes are going to find more attractive markets in many locations versus the US. While we have seen some moves to create low carbon polymers and low carbon ammonia, this has not come to methanol yet and methanol does have one of the largest CO2 footprints, per ton of product. While Methanex is currently talking about returning surplus cash to shareholders, there may come a time – sooner rather than later – when some of that cash gets redirected to carbon abatement.

There are lots of discussions around the durability of higher energy prices and energy inflation is a central topic on some earnings conference calls and in many of our discussions with clients, especially those at chemical companies with the unfortunate task of having to prepare a 2022 budget, which of course includes a forecast of costs. We see continuing strain on the US and global natural gas system and, behind what will inevitably be some seasonal weather-related price volatility, a stronger market that could endure for years. The rate of addition of renewable power does not seem to be able to keep up with demand growth and replacement needs caused by some fossil fuel-based power plant closures around the World. Natural gas (LNG) is the natural plug-in replacement, and we continue to see underinvestment, relative to natural gas prices, as a consequence of ESG related pressure around capital spending. We would advise all clients to look at a 2022 scenario with natural gas, and oil higher than current levels.

We are seeing some stability in ethylene and propylene pricing in the US to start the week, and with the steady rise in crude prices and the Monday jump in natural gas prices, this is not surprising. As we noted in yesterday’s Weekly Catalyst, there is enough incentive to export ethylene from the US to Asia – most likely Southeast Asia rather than North Asia, and this could offer support for those with surplus ethylene in the US today.

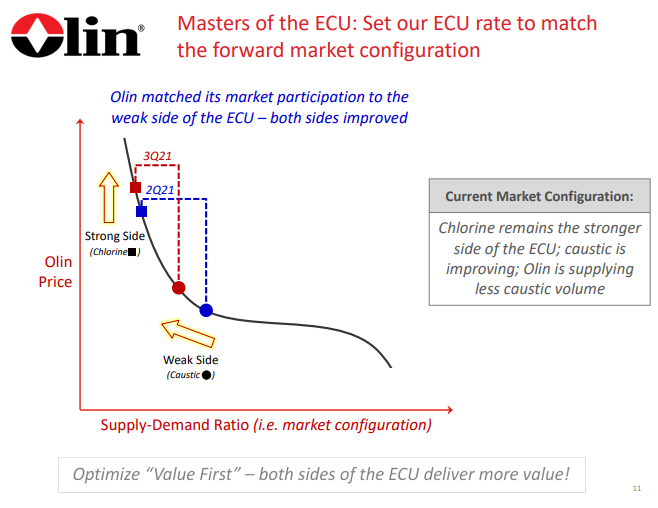

We will expand on the Olin results and some of the benefits and potential pitfalls of the revised strategy in our Sunday piece as we can draw some comparisons (some good and some bad) from other corporate examples over time. For now, it is working and few would have predicted a $50+ stock for Olin a year ago. Some market fundamentals are working in Olin’s favor, but much of the success is coming from a more radical approach to customer engagement and avoidance of customers generating minimal returns, regardless of what that means for production. So far this is a great first act from the new leadership of Scott Sutton – we will talk about what a second act may need to look like on Sunday.