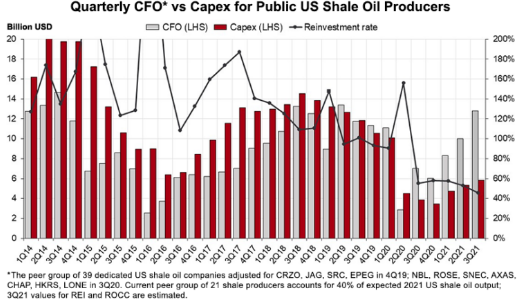

We should probably link the message in the exhibit below with the write-ups in both today's daily report and today's ESG and Climate report. The drop in E&P spending relative to cash flows and the shortage signals that are evident from the current oil and natural gas prices is likely to bump into rising hydrocarbon demand for the next several years, while the rate of renewable investment tires to catch up with energy growth before it can focus on energy substitution as meaningfully as the climate agenda would like. We also cannot look at the chart below and say that it does not matter because oil is less important in energy transition than natural gas. The oil-based investments in the Permian and Eagleford plays, in particular, have significant volumes of associated gas, and much of the natural gas supply growth in the US has come from these oil-centric investments. As they slow down, natural gas supply and NGL supply will be impacted, and while we are seeing increased rig counts in the natural gas biased regions, such as the Marcellus, the potential declines from the other fields will be hard to make up for.

Recent Posts

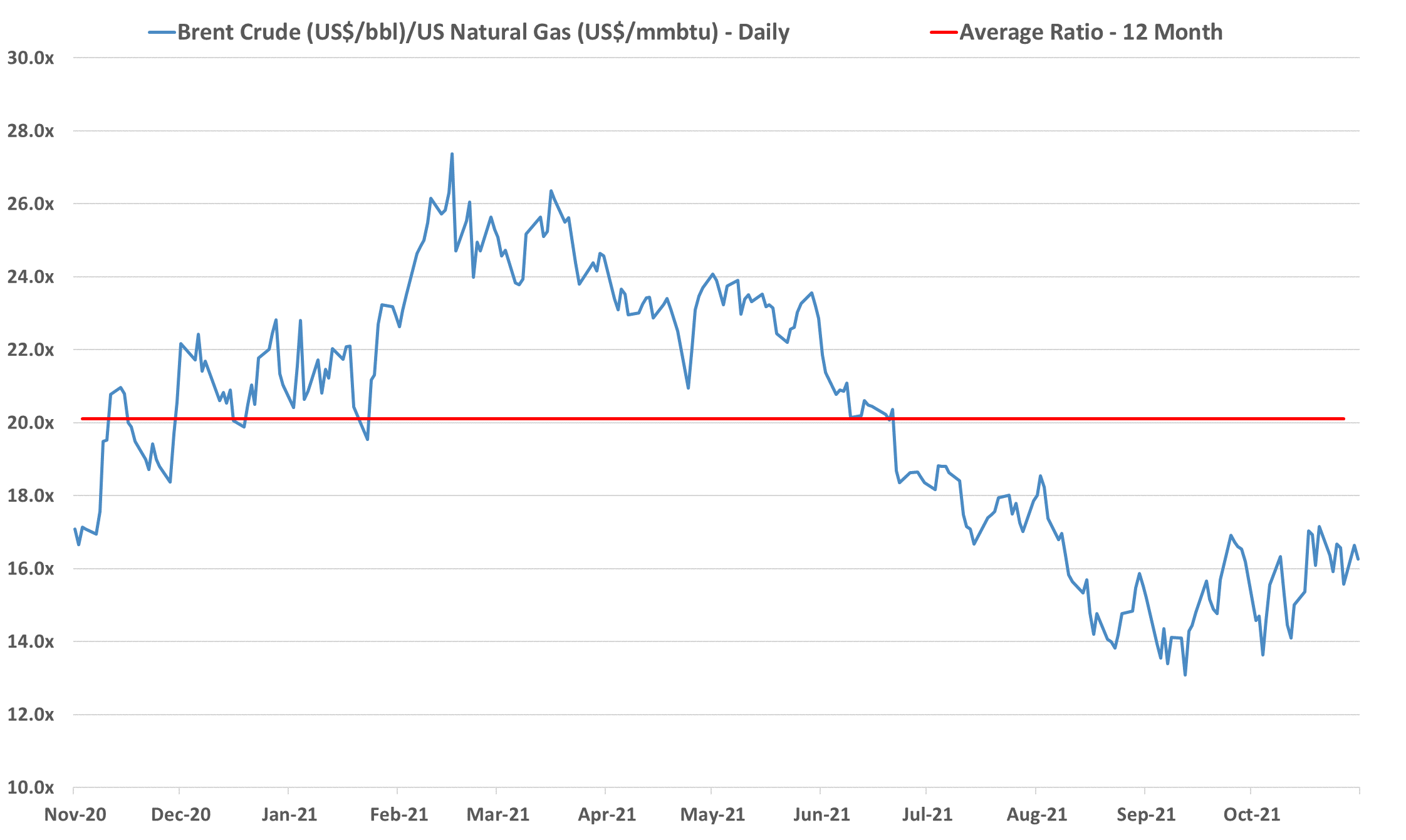

We remain concerned that natural gas E&P investment in the US remains too low to meet expected demand increases, especially for natural gas-fired power stations and LNG, but also possibly for NGLs, especially ethane, given new ethylene capacity and a fresh export market in Mexico. Near-term, natural gas prices are showing some easing relative to crude, albeit a very volatile trend – Exhibit below – but we see medium and longer-term shortages unless E&P spending increases. The new power facilities shown in the bottom Exhibit will all need incremental natural gas, and the international LNG market is so tight that as new capacity comes online in the US we would expect it to run as hard as is possible. This sets up for a market where the clearing price of natural gas in the US is at risk of being set by the marginal exporter. The price jump for domestic consumers would be dramatic and it would cause all sorts of headaches in Washington and probably intervention. We showed the incremental natural gas price in the Netherlands in our Daily Report on November 18th, and if the US price were to reflect the netback from this level, they would rise close to $30 per MMBTU. The natural gas industry needs some sort of global blessing to continue to operate as what will likely be the core transition fuel. It will be necessary to clean up the emissions footprint of natural gas, but the industry should be encouraged to invest on this basis. For those who doubt whether the US natural gas price can rise to $30/MMBTU – note that the Europeans did not think $30 was possible either.

Another Lesson From The Past: Costs Will Matter

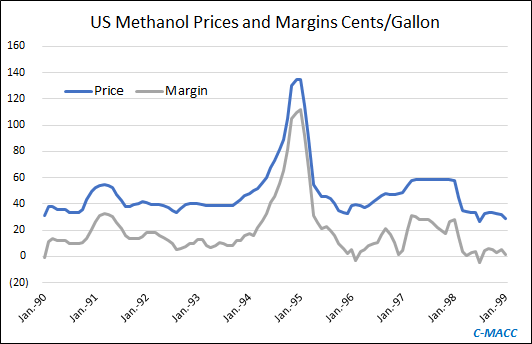

High prices are spurring behavioral changes throughout the supply chain. Per our analysis, it is causing buyers to look for alternatives and ways to use less material and increasing interest in new production, often without much thought about relative cost. In Exhibit 1 (from yesterday's report), we show the methanol peak of the mid-90s. This development resulted from supply shortages rather than high costs. It encouraged multiple projects to receive serious consideration – including methanol from wood chips – where costs looked good at the time but not on a historical basis, and as the chart shows, not on a forward basis. Most ideas never got past the planning stage. With sustainability driving a significant share of the growth investment decisions, we think several “renewable” ideas could encourage investment that rely on price premiums to keep returns attractive. While this setting might look supported today, it will likely look less tenable if traditional commodity prices retreat into a commodity trough or lower-cost competitive materials emerge.

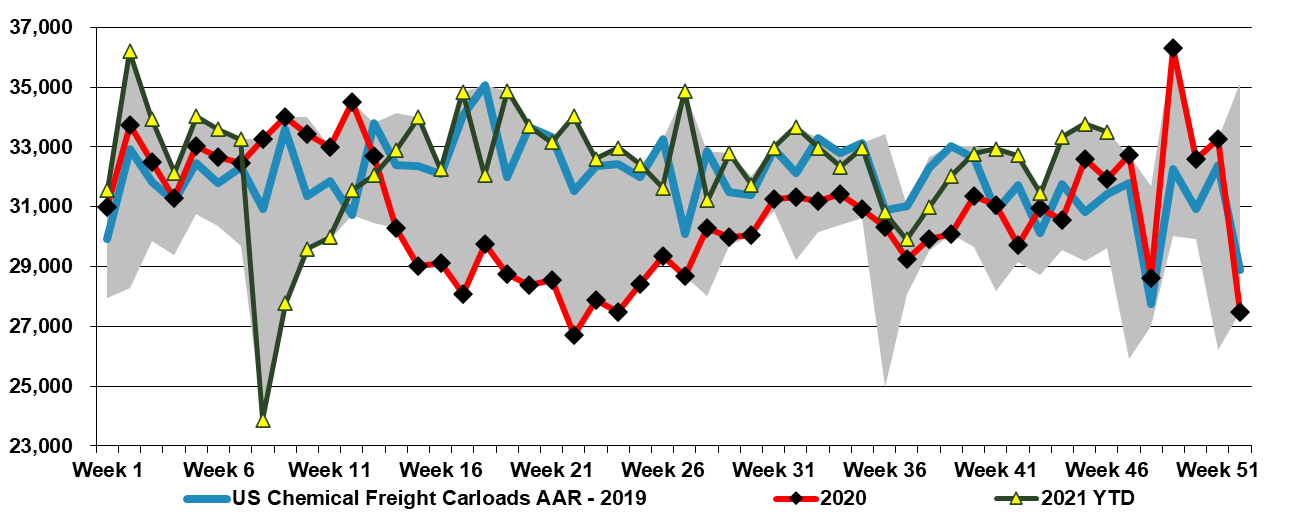

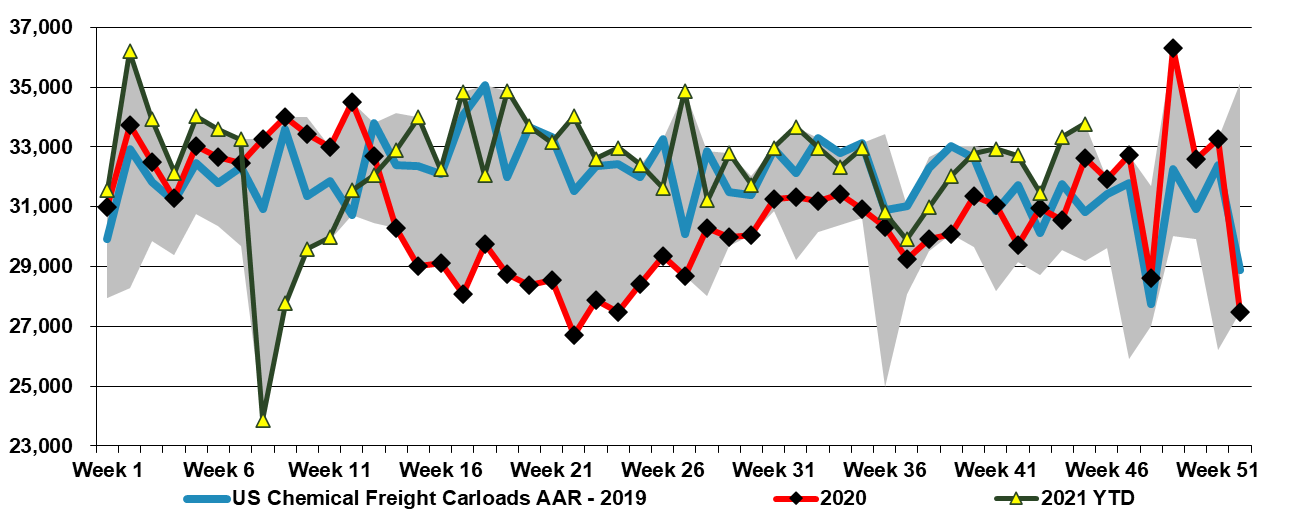

US rail data for chemicals remain at the 5-year highs and have been there for almost 2 months. This is working its way into the supply chain and we are seeing weakness in US polymer prices across the board, except for PVC. US spot polymer prices are in a bit of a “no man's land” right now as they would need to drop significantly to find incremental demand offshore, given US premiums to the rest of the world. We believe that most of the volume leaving the US is doing so within company-specific businesses – ExxonMobil supplying ExxonMobil customers, Dow supplying Dow customers, etc, and consequently, these shipments do not show up in the spot market.

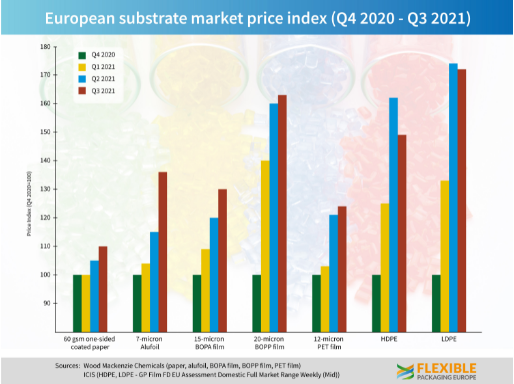

Focusing on a theme from our daily report today and our ESG report yesterday, the cost pressures in Europe are very real, and the more the power or natural gas component to your costs the more the pain and the more important it will be to raise prices. The industry and consumers, in general, have not had to deal with significant inflation for decades and it is very easy for customers to push back with a “this is transitory” argument, especially when many governments are telling that story. The supply chain is to blame to a degree, but it is largely a symptom of the underlying cause, which is that demand has outstripped supply. It is easy and more palatable to try and brush it off as temporary, but if the energy price issues persist in Europe and China and companies are not successful in passing on prices they will, at some point, choose not to operate. Alternatively, if power shortages are enough to cause interruptions, industrial users may have no choice but to close down. All this will impact product availability and buyers pushing back on price increases could find themselves without supply which is generally worse than paying more. The European packaging industry is right to raise the flag around higher prices, but their customers will pay the increases needed to ensure that they can keep operating, even if the discussions are more challenging than they have needed to be for the last 30 years.

The linked article looks at the chemical inflationary cycle of the 70s, which has some relevant indicators for what we are seeing today, but there were also some stark differences. Rising raw material prices is a common theme and while it is convenient to blame OPEC+ this time, the group is not nearly as much to blame today as it was in the 70s. Consumers were facing not just higher oil prices, but also genuine shortages because of the OPEC cutbacks and the multi-year lead times that it took non-OPEC producers to ramp up E&P and ultimately production. This time the oil is there and relatively easy to get to, especially in the US, but the capital spending decisions of the US oil producers – mostly because of ESG related pressure – are holding back the production.

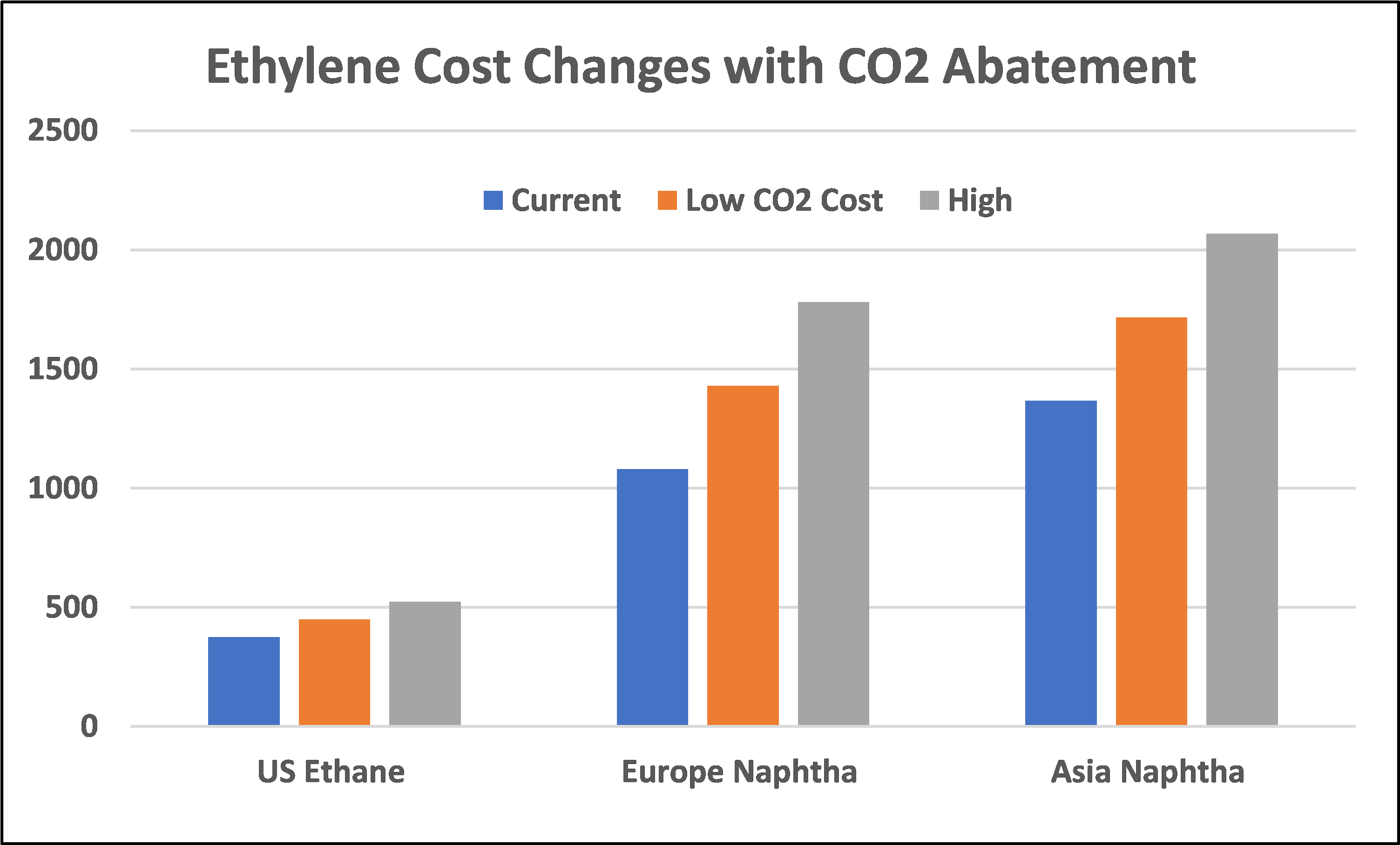

In an important, but inevitable, change in tone, it is worth noting that the Borouge ethylene expansion announcement includes the idea that the complex will explore the possibility of a major carbon capture facility that will take much of the CO2 from the existing complex as well as the new plant. We have stated previously that the mood has changed sufficiently such that large industrial investments without a carbon abatement plan will not get approval from stakeholders and this is a prime example of what we expect. Locations with low-cost CCS will see disproportionate investment in our view and Abu Dhabi already has CCS in place as Adnoc is selling blue ammonia already to Japan. As we noted in a recent Sunday Piece, we expect carbon abatement challenges to slow expansions in basic chemicals and, despite this announcement by Borealis, see a market shortage in 2024/25 as a consequence.

Our Sunday Thematic research a week ago (see linked report) discussed slowing growth investment in the traditional commodity chemical industry and suggested that ESG and climate pressures might slow investment even further. Yesterday, our Sunday Thematic made the argument that some of those dollars will target strategic M&A. We have recently seen an uptick in global chemicals sector M&A, and we find few items suggesting activity levels will slow in the near-to-medium term. In part, we think strategic M&A will be easier to get Board approval for than “new build” capacity additions, and it can be viewed as better use than holding cash or complementary to dividends and buybacks. Also, ESG and climate concerns could spur M&A activity, as companies look to separate bad emission assets from good ones – especially if the market values them very differently.

In the first Exhibit below we show a 5-year high in chemical rail-car movements. We have noted in research since early October that 4Q production in the US could be very high because of a combination of available capacity – following a year of weather-related delays – and very attractive margins and demand. We have been at the high end of rail car volumes for most of the quarter, and this may be part of the reason why we are seeing some price weakness for polymers in the US. Most of the polyethylene exported from the US moves from the manufacturing site to the export port via rail, so increased exports would also drive higher rail car numbers. As long as pricing and margins remain high and customer demand robust, we would expect these higher volumes to continue. This does not make us any less concerned that somewhere in the chain there is now an inventory build going on and that fortunes could reverse in 2022.

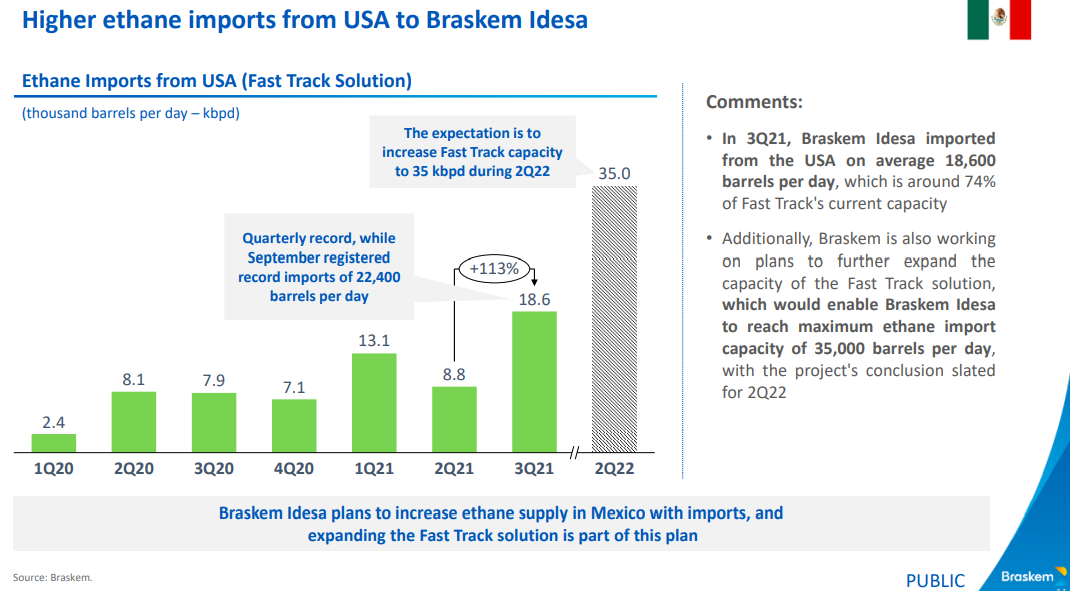

With ExxonMobil and Baystar’s ethylene plants in start-up and Shell expected to come online in Pennsylvania in 1H 2022, the news that Braskem wants to double its ethane imports from the US in 2022, adds to concern that the US may struggle to meet ethane needs at peak demand rates in 2022. We would be less concerned if we saw natural gas production rising, which is unclear for 2022, despite the expected new LNG capacity. Ethane is likely to follow any upward movement in natural gas pricing as there will be a need to bid the product away from heating alternatives. The increment suggested by Braskem in the Exhibit below is not larger in the overall scheme of US ethane demand, but every gallon may matter in 2022. See today's daily report for more.