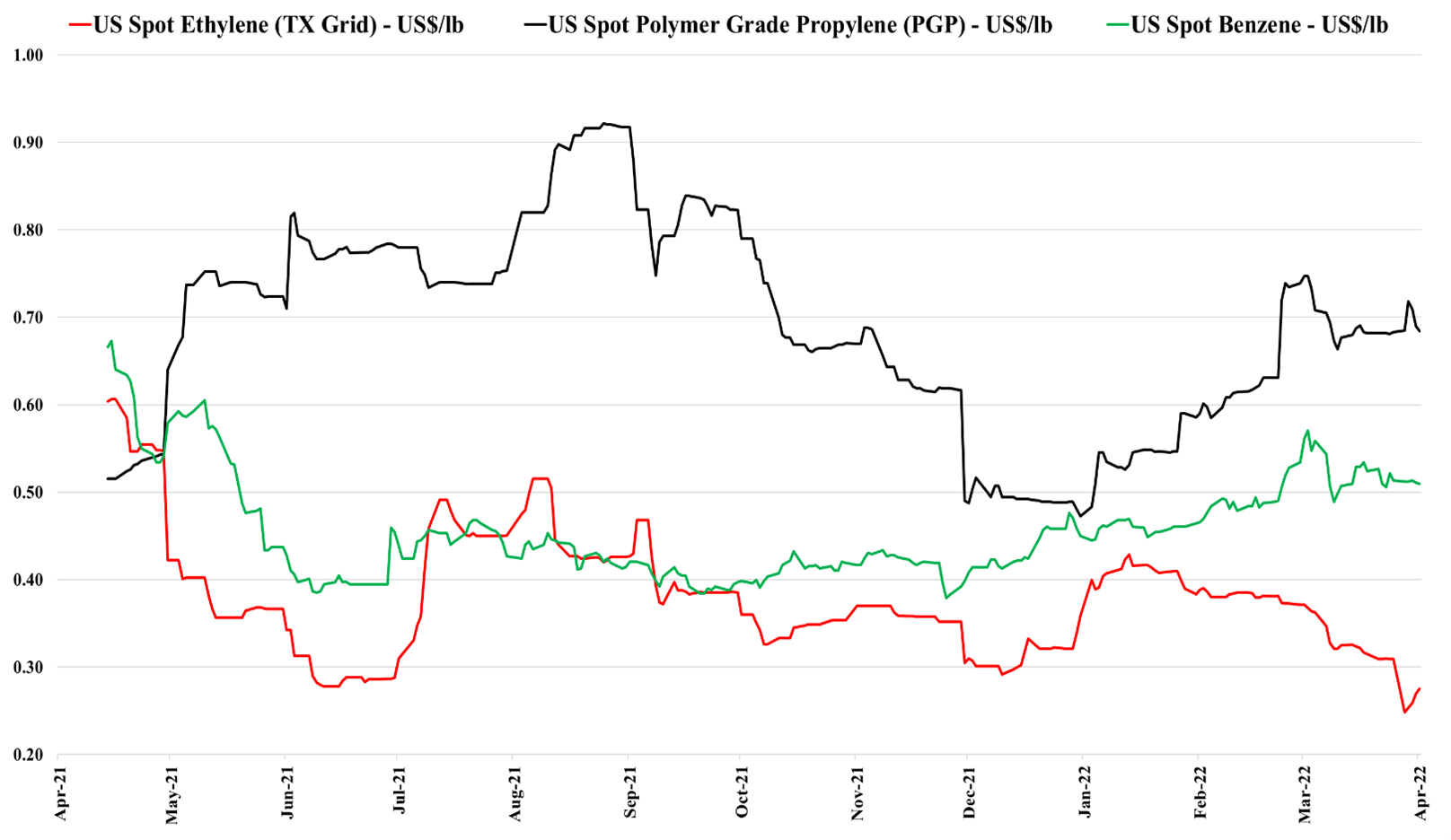

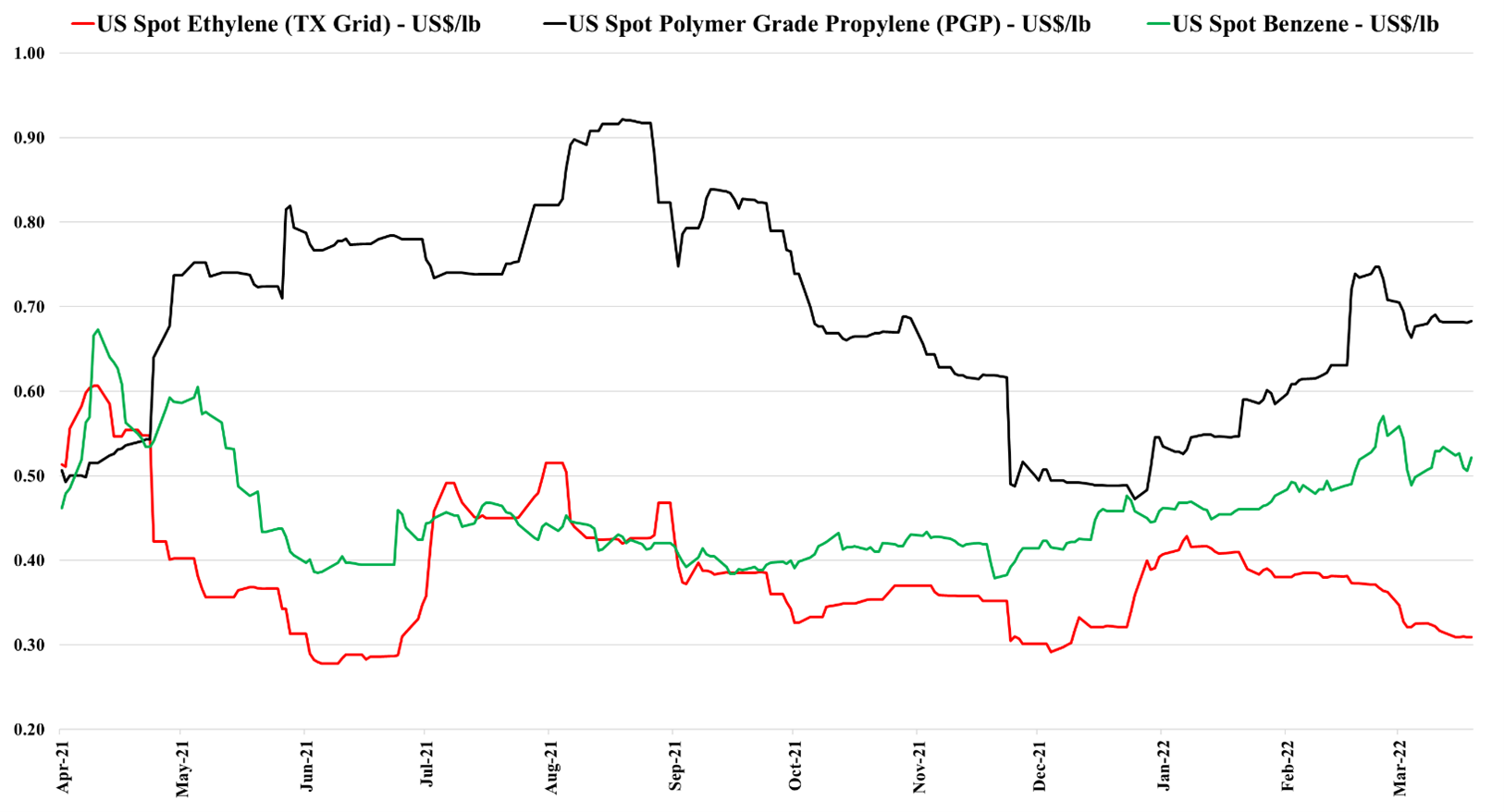

US ethylene prices have bounced off a low this week largely, in our view on the steep rise in natural gas and ethane. The drop in ethylene prices over the last couple of weeks signals an imbalance whereby production is more than enough to satisfy domestic demand and export demand. Export demand is limited by terminal capacity, and we have seen some domestic demand issues for polyethylene, not because of demand weakness, but because of export logistic bottlenecks, that are resulting in product (with homes to go to) backing up in the US ports. Given the timing of this build-up, we may see some higher end-quarter working capital from some of the chemical companies with sizeable export footprints for 1Q 2022. The sharp increase in US natural gas prices and the catch up that ethane has made to natural gas, should keep some upward pressure on spot ethylene prices if gas prices remain high. Propylene remains very supported by high propane prices.

Recent Posts

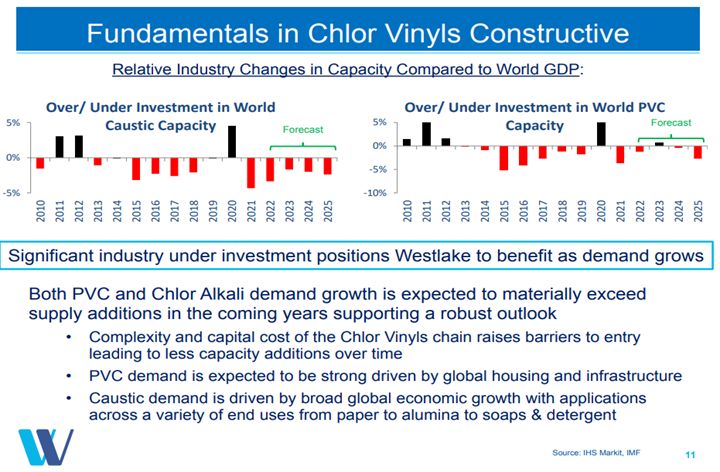

The margin weakness in PVC, as shown in Exhibit 1 from today's daily report, suggests that the market might be weakening, but higher prices would suggest that it is not. The integrated margin weakness is mostly the result of rising costs, and the US PVC market may be strong enough to allow producers to pass on these costs fully over time. We still see PVC as the least risky way to play the US polymers market as infrastructure and manufacturing investments should keep demand strong even if we see a decline in consumer durable related spending. The Westlake chart below highlights one of the primary drivers behind our mega-cycle view – no new capacity. The supply shortfalls that are implied in the chart will be mirrored in other basic chemicals in our view but PVC is likely the most acute example – creating what could be a prolonged period of strong margins for the industry.

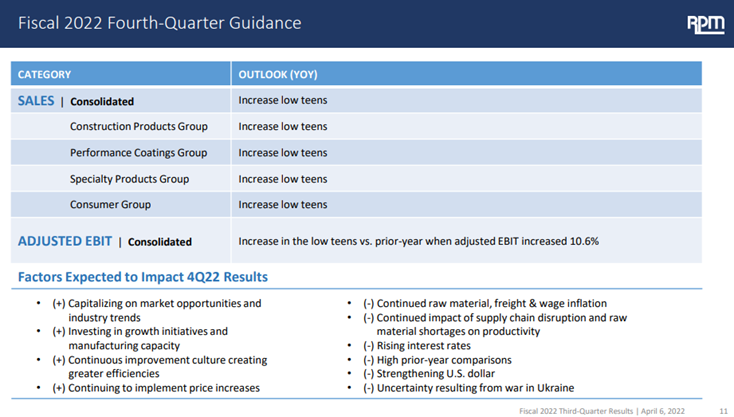

While we remain advocates of “stronger for longer” with respect to chemical demand and pricing in the US, the auto data does suggest that the US consumer may be cooling off a bit in reaction to higher prices and higher borrowing rates. Historically, the chemical industry has a habit of running headlong into a downturn while waving an “everything is great” flag, and the RPM results and outlook have a vague “deja vu” feel to them. We also note some surprise at the robustness of the MDI market in the chart below, and it would be wrong not to admit that our cautionary antennas are rising. The auto exposed products should still see some upside from higher auto production in the second half of the year, but otherwise, a possible consumer pullback to take the wind out of the sector sales, especially if the US is constrained moving out products because of container and shipping issues. The significant cost advantage remains in the US but the ethylene market over the last week is a reminder of what can happen when you struggle to find someone who can take the last pound. Given infrastructure, energy, and clean energy investment, as well as reshoring, many materials could see significant offsets to consumer spending pullbacks and our focus would remain on PVC and building products, as most of the hit would be in consumer durables. Metals demand should remain strong regardless. For more see today's daily report.

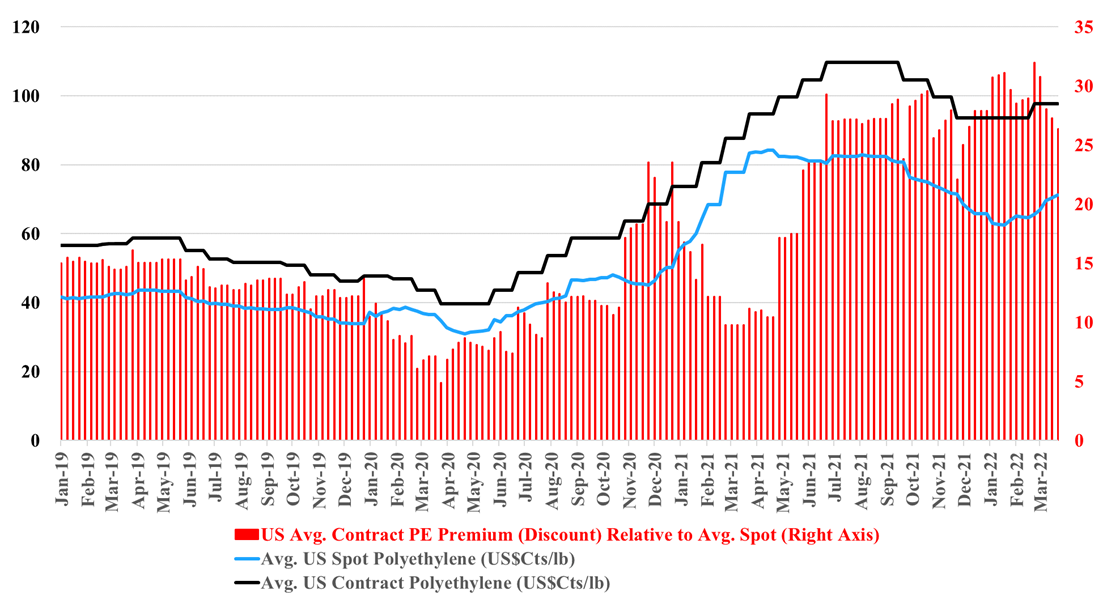

It's back to 2012/2013 for polyethylene, but with a potential twist. As we noted in today's daily report, international prices for polyethylene are being pushed up by oil prices, and even with higher prices in Asia, margins are still negative locally, which suggests that they will go higher. This margin umbrella is what generated windfall profits for US and Middle East producers in 2012, 2013, and half of 2014. The upward pressure remains high for international polyethylene prices because producers are not covering costs locally and in theory, the US should continue to benefit and we see domestic polyethylene prices rising again, both contract and spot. The risk for the US is local overcapacity of polyethylene and potential export challenges. The pricing arbitrage to export US polyethylene is huge and rising, but we are in a constrained trade world and we understand that export terminals are at capacity and warehouses are full. It is possible that the sharply lower US ethylene price is not just a function of new ethylene capacity, but also a function of integrated polyethylene producers choosing to limit production and looking for homes for the extra ethylene. If the polyethylene producers in the US try to push more volume domestically we could see local prices fall well below their export alternative – this is possible, but unlikely, in our view. Polypropylene does not have the same significant net export and the two plant closure in the US are likely enough to drive the price support that we are seeing this week.

The BASF commentary about the impact of gas cuts in Europe should not be read as specific to BASF, but as we move out of the winter in Europe it is less likely that countries will directly restrict industry in favor of retail customers should gas supplies become limited. While many European countries will try to protect retail customers from hyperinflation in energy costs, their ability to do that for the industry might be more limited as they cannot find the additional gas, and subsidizing everything would be fiscally irresponsible. We expect to see more basic chemicals and derivatives moving from the US and the Middle East to Europe to displace uneconomic local production, but we understand that all shipping capacity is now constrained – liquids, gases, and containers – limiting the volumes that can move. The high end of the cost curve that Europe has occupied for decades in chemicals means that exports from Europe have been very limited and reducing exports is not a balancing act tool that Europe has to play with. We continue to see significant upward pressure on prices in Europe and the jump in inflation in the region, reported today, was dramatic but could accelerate as there are very few corrective levers that Europe can pull right now.

We are seeing some monomer price weakness in the US, despite the rising costs. For ethylene, this is likely because of increased supplies (new capacity and turnarounds ending) and all capacity to consume running at full rates, including the export terminals. There is plenty of margin in exporting ethylene today and US prices are not falling because they need to find another buyer internationally. We could see some opportunistic buying for inventory at these prices, especially if you believe that the conflict in Ukraine is not ending soon and also if you are concerned about more extreme weather as we move through the summer in the south of the US.

We focus on the building products industry today and it is interesting to note the convergence of the S&P Building Products index and Westlake over the early part of this year, as Westlake has been recognized for its building products footprint, partly aided by the company’s re-segmenting with the last quarterly earnings. The company has reached an all-time high stock price over the last few weeks and has certainly been a great preferred pick for us over the last two years. As interest and mortgage rates rise, we may see a slowdown in home buying as there is generally a good correlation, but this often leads to more home projects as consumers choose not to move and improve what they have.

We noted in today's daily report the number of shutdowns that are taking place in Asia and in Europe as feedstock costs become unmanageable, and the assumption is that these units will restart when economics recover. This may not be the case as companies factor in the costs of operating smaller units in an emission-constrained world, and the decision to shut down for economic reasons today may be the final nail in the coffin for some older and generally less economic base chemical units. Many smaller facilities in China were built in the 80s and 90s and these might not come back online if there is no easy way to lower emissions, but the harder decisions will likely be in Europe.

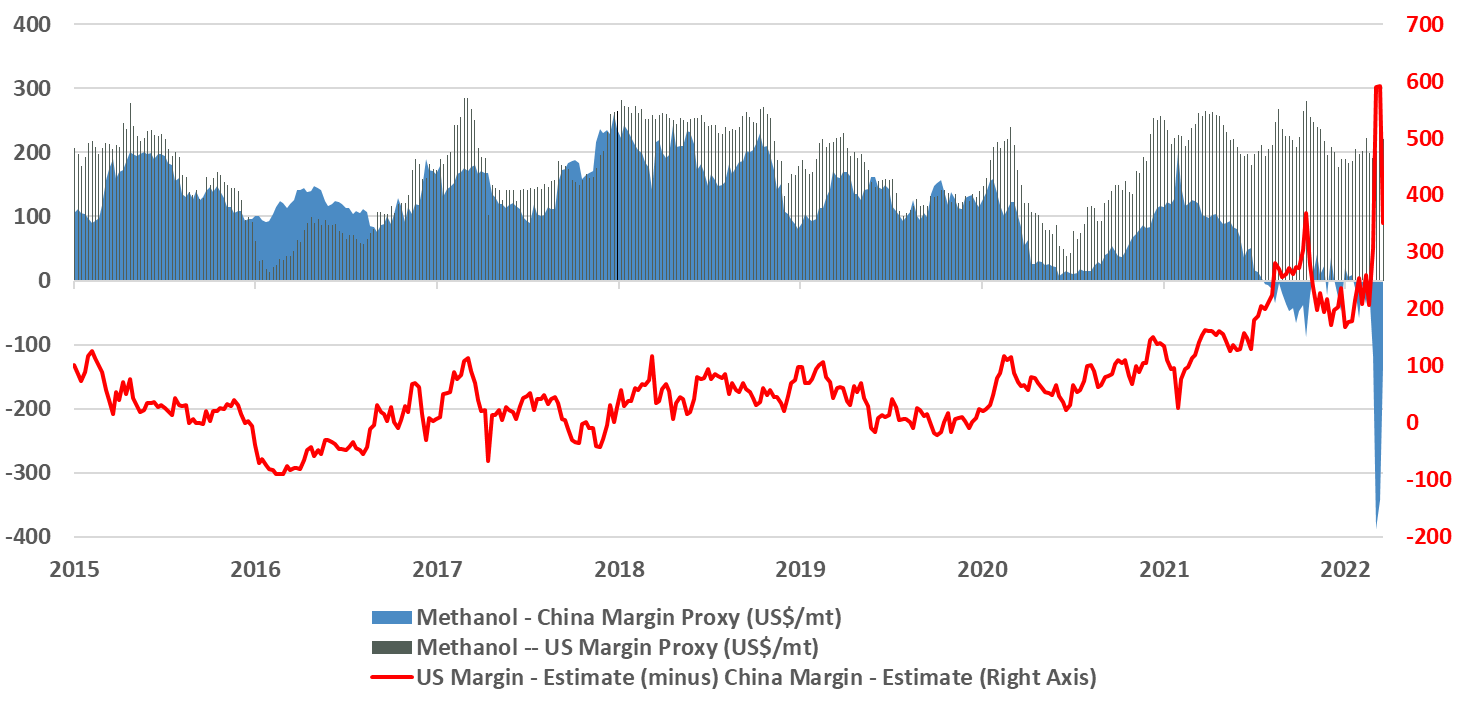

Methanol is one of a few chemicals that is directly impacted by the price of natural gas, and as the chart below shows, the pain in China (and in Europe) is extreme and it is unlikely that any facilities that require imported natural gas – or local gas with prices based on imports – are operating today. The volume and margin opportunities for those companies connected to low priced natural gas – the US, the Middle East, and other niche locations such as Trinidad, are as good as they have ever been and we are a little surprised that Methanex did not push a little harder with US pricing, given that export netbacks are likely surging. Urea and ammonia are in the same boat and prices are much higher, but the US is a net importer and international prices are directly impacting the US price.

The closure of the Russian oil pipeline and export terminal as well as the move to want payment in Roubles, are all likely tactics from Putin to cause more market chaos in an attempt to hit back over sanctions. While Russia likely needs the oil and gas revenues, sending oil higher is likely intended to see whether the West cracks, which seems unlikely. The Rouble payment is also meant to inconvenience the West but at the same time maybe support the Rouble as West Europe needs the gas and will need to buy Roubles to may payments.