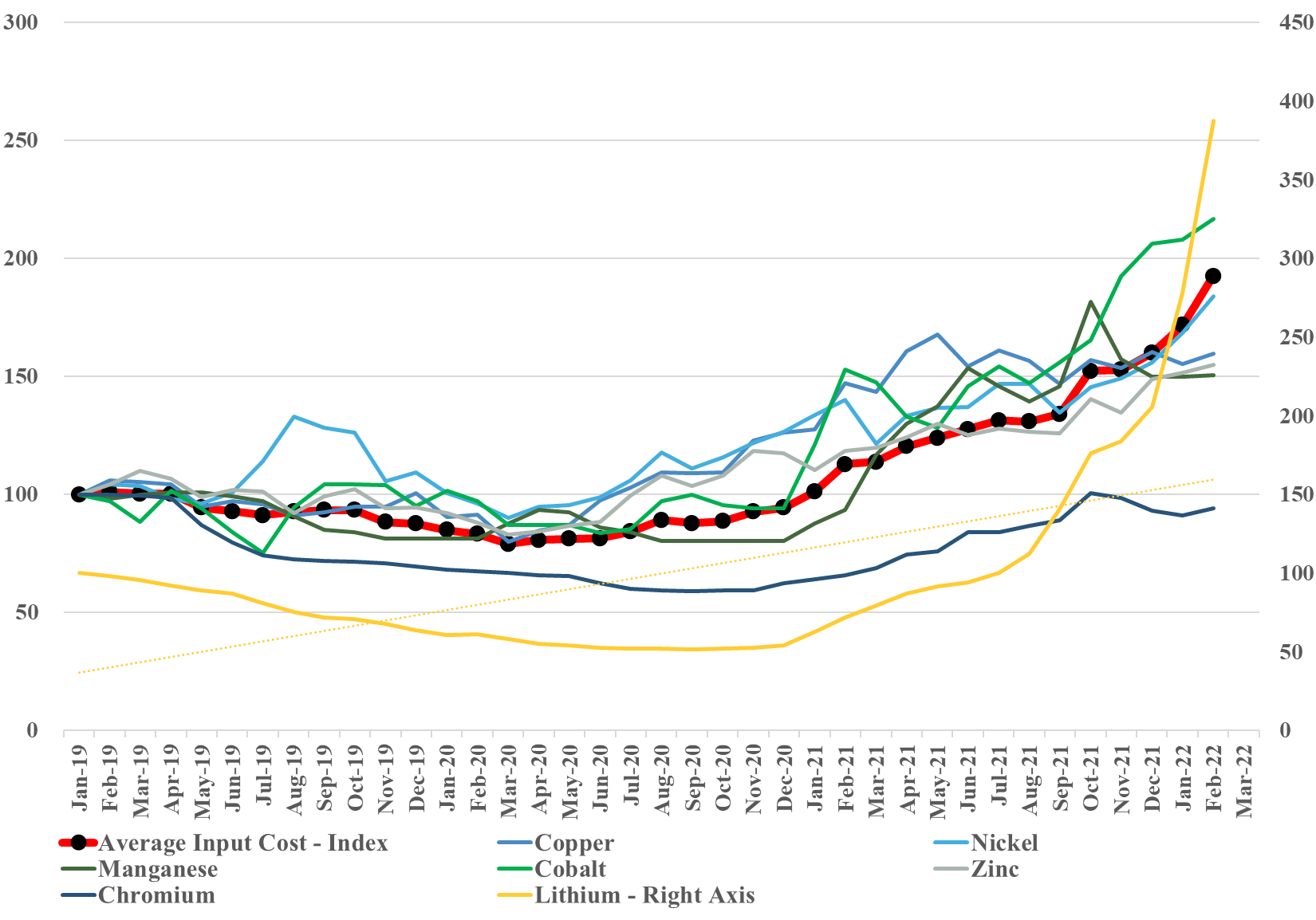

One of the key messages from the World Petrochemical Conference is that it is not an oil shortage, it is a commodity shortage, and we show our key metals index (updated through February) again in the chart below. We will update this again at the end of March (when consistent data is available) and given what has happened to both lithium and nickel prices we would expect a jump in the March index.

Recent Posts

We have talked at length in today's daily and recent Sunday recaps about our expectation for a mega-cycle in chemicals because of an unwillingness to deploy capital as uncertainty rises. The exception is likely to be large oil producers looking at long-term downstream integration plans, with the primary objective of consuming captive crude oil. The Aramco ambitions in China bear some similarities to the ExxonMobil investment announced for China last year. While the crude oil market may be tight and prices may be high today, few oil producers believe that demand will not ultimately be hurt by renewable penetration and EV and hydrogen growth as transport fuels. Looking for captive crude oil demand is a logical step for the major and it is likely that the Aramco ambitions include refining as well as chemicals in China.

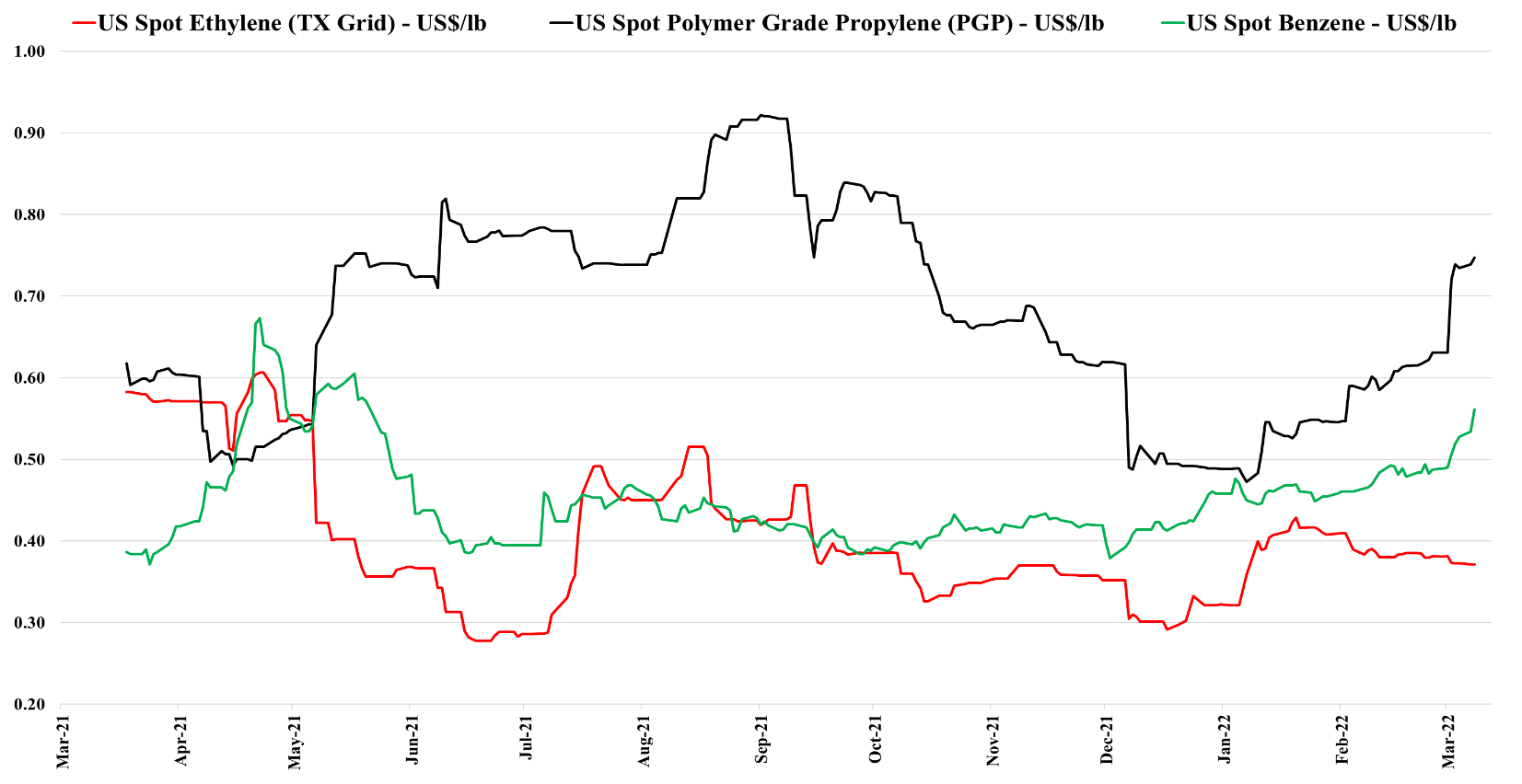

As we have been suggesting for some time, there are pockets of real strength in chemicals; identifying them is the hard part. It is not enough to have pricing strength in a market where raw material prices are volatile daily and we have seen plenty of examples of companies with very strong end demand dynamics missing earnings because of a cost squeeze. We continue to highlight the competitive strength in the US in basic chemicals because of the decoupled and relatively low natural gas price and this is likely a large piece of the Dow earnings strength – strong polyethylene demand against a backdrop of relatively stable and lower costs. While polypropylene (Braskem) remains extremely profitable in the US, it has seen more sequential weakness than polyethylene – as we show in Exhibit 1 of today's daily report. That said, both polyethylene and polypropylene margins in the US are significantly higher than was likely expected this year and certainly what has been reflected in stock valuations, even with the commodity chemicals rally. Dow is also seeing the benefit of a very strong silicones market – something that was covered in detail in Wacker’s release earlier this month.

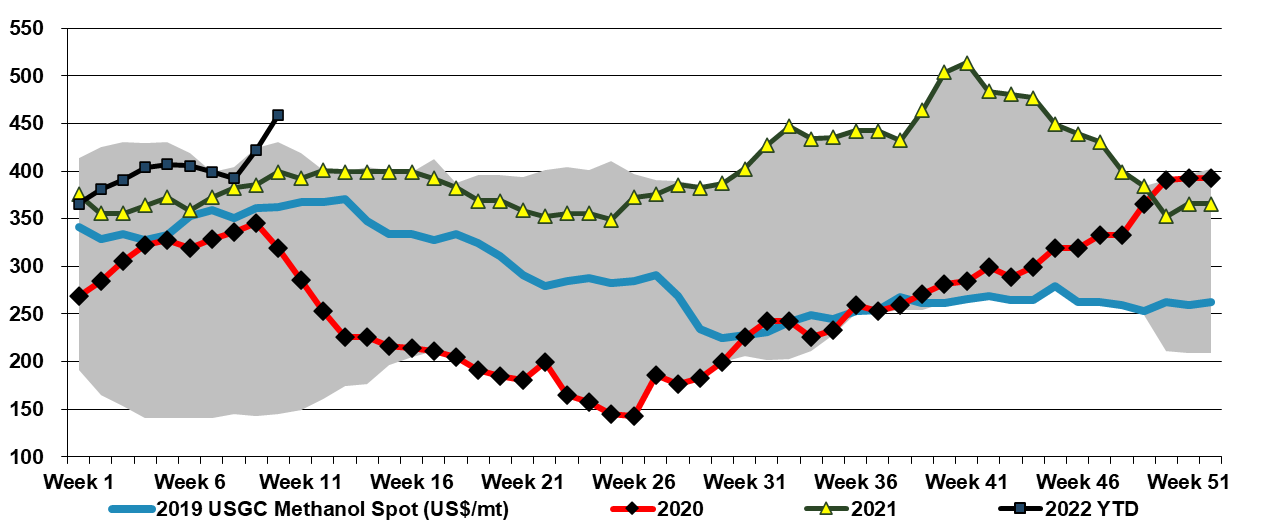

A couple of weeks ago we raised the idea that US methanol could be a significant beneficiary of the conflict in Central Europe, not just because it is very economically unattractive to make methanol in Europe, but because it might be possible for Europe to import methanol for its energy value - $40 per MMBTU natural gas can make all sort of alternates look attractive. The impetus behind the methanol spot price increase in the US may be in part rising local natural gas – or the fear of further increases – but export demand is likely the larger driving factor and this could continue or even increase further if potential European importers work out how to convert to use methanol as a fuel.

Could what we are seeing in metals happen in chemicals and polymers? Over the last few weeks, we have seen already high metals pricing spike even further, both because of production shortfalls and because of expectation of higher demand, especially in the renewables space, as conventional energy prices have spiked. We show a lithium example below, but note that after chaotic nickel trading last week and a halt to trading, the market has made some attempts to reopen this morning with renewed problems.

The very strong Wacker results and bullish outlook make sense for a company very exposed to the solar industry. The solar companies themselves may be struggling to make money, but their demand is very high and their thirst for raw materials equally high. In bp’s annual review of world energy, the company is forecasting a three-fold increase in the rate of annual renewable power investment and all of this will require more materials – setting up polysilicon suppliers like Wacker very well. The negative for Wacker, of course, is the high European footprint and the current increase in energy costs in Europe. Given the strong demand for polysilicon, Wacker should be able to raise prices – adding to the woes of the solar panel makers. See more in today's daily report.

The Lanxess guidance below is likely the right way to go for now. The medium-term effects of the Russia/Ukraine crisis are unknowable today and all companies can monitor is the immediate impact on their businesses. Most had entered 2022 seeing very strong demand growth and the promise of a much better year as COVID restrictions were lifted and economic activity picked up generally. Now all bets are off, as it is not just the primary impacts that matter – such as a companies’ direct exposure to Russia or Ukraine – note McDonald's is suggesting that pulling out of Russia will cost the company $50 million a month, for example – but also the secondary impacts of what the conflict is doing for supply-chains and pricing. Higher hydrocarbon pricing in Europe, for example, will impact the economics of all production, not just the products sold to Russia or Ukraine. There will also be some demand adjustments directly related to the conflict – disaster relief for example – more PPE – more spending on defense and defense-related materials – DuPont’s kevlar business should be seeing a benefit for example.

As noted in Exhibit 1 from today's daily report, the jump in oil prices has plunged the European polyethylene producers into the red and pushed Asian polyethylene producers further into the red. This will inevitably result in price increases as basic chemical and polymer producers will shut down at negative margins, and these price rises offer an opportunity for the US, Middle East, and select other producers.

With the rapid jump in international natural gas and oil prices, we would see very concerted efforts to raise basic chemicals and polymer prices in Europe and Asia and will have a positive knock-on effect for the US. In our weekly catalyst report on Monday, we showed that ethylene producers outside the US were all losing money, especially in Europe and Asia. Some European demand will already be lower, because of curtailed product exports to Russia and Ukraine, but producers will want to cover costs at a very minimum and consequently, will be trying to match price increases with cost increases and if possible do a bit better than that. All of this will create a greater margin umbrella for the US, and US exporters selling directly into international markets will see export margins step up and may see incremental opportunities to export more, assuming that the freight rates are not too onerous for incremental containers.

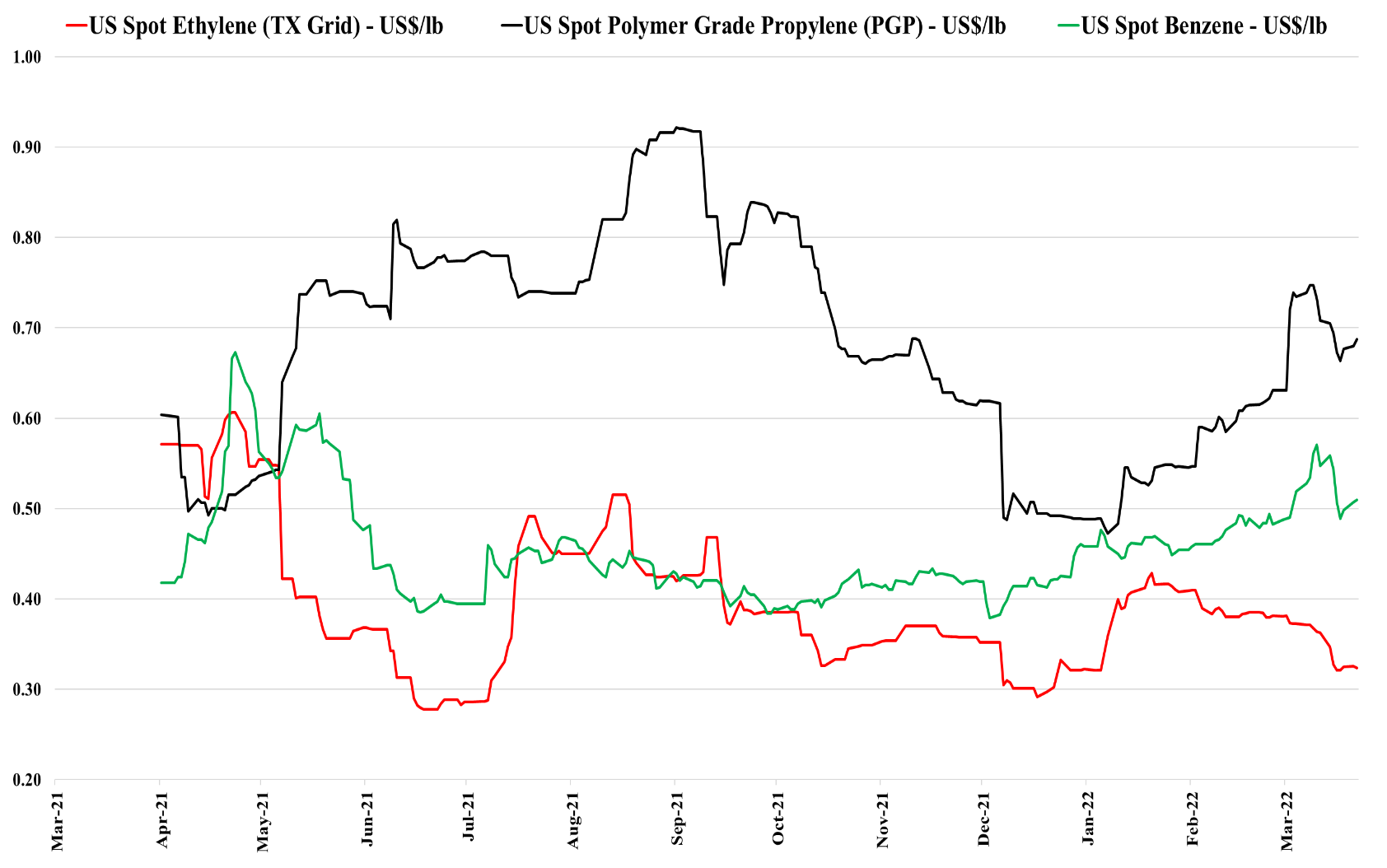

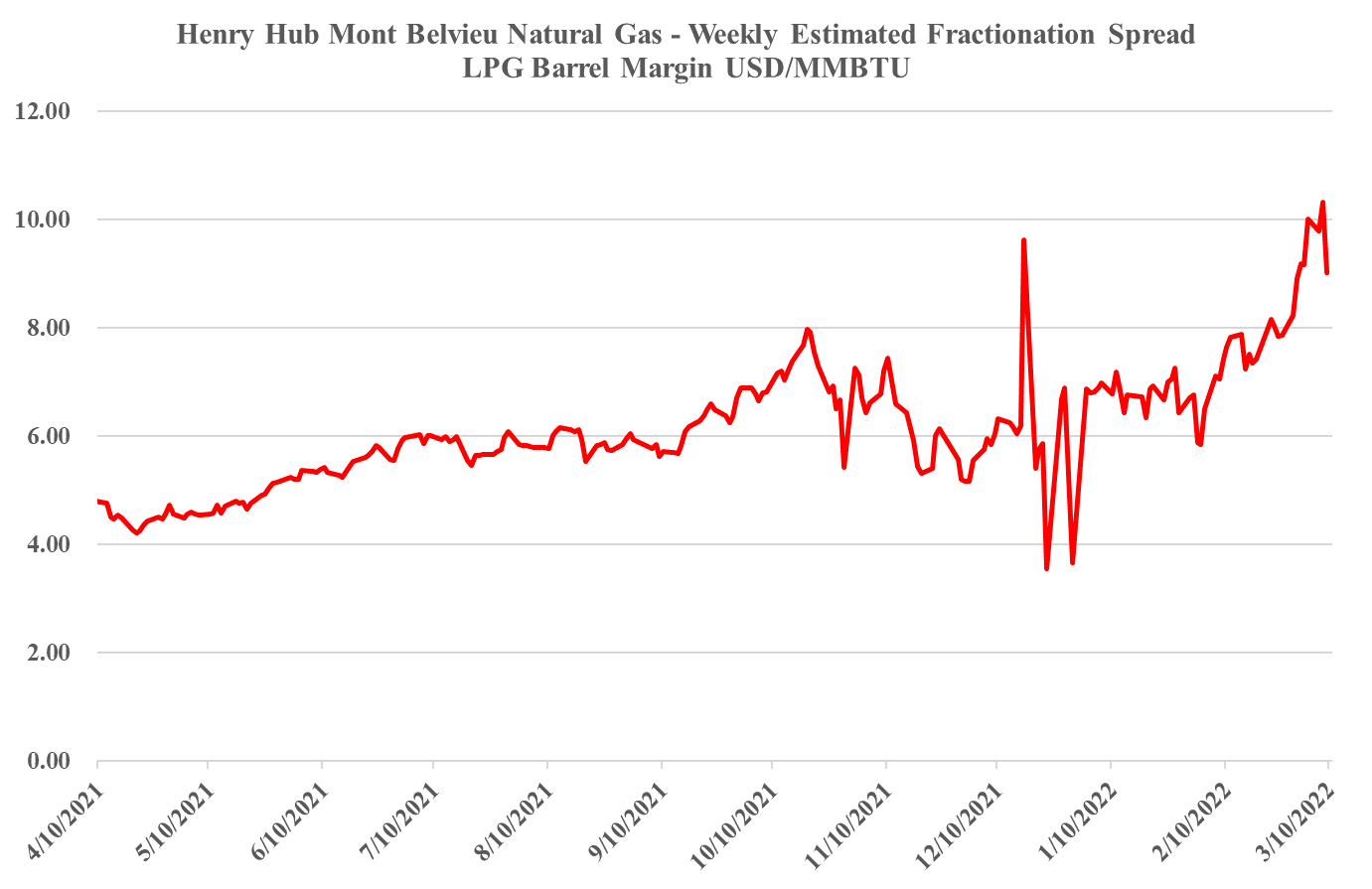

It is interesting to note the rapid rise in US propylene (and benzene) values as they follow propane and crude prices (propane is following crude because of its heating value and export opportunities). Ethylene is not moving as US natural gas is in surplus and is not following international natural gas prices. The US is surplus ethylene and derivatives, but we would expect to see ethylene and ethylene derivative prices jump up in the US if Europe is physically unable to make ethylene and derivatives or if the costs in Europe become so high that supplying incremental volumes from the US becomes even more compelling. For more see today's report titled "Into The Mystic – Ex-US Energy Price Surge Favors US Producers; Low Visibility Keeps Capex In Check".