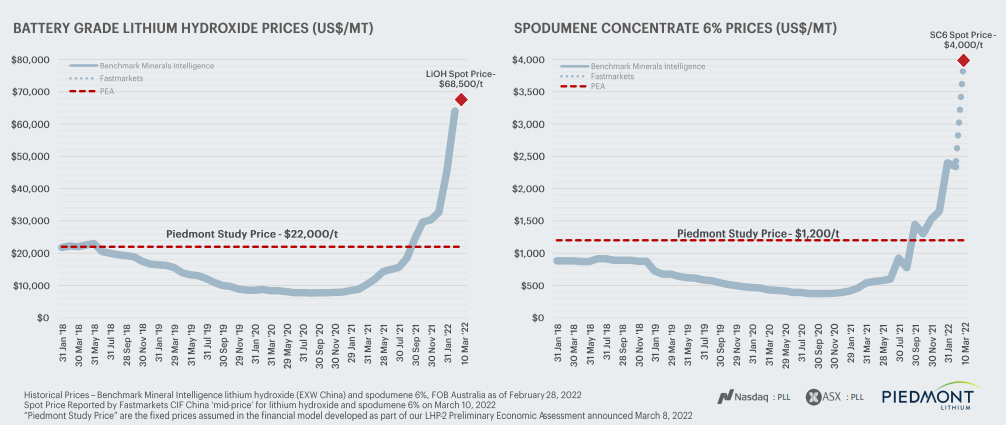

Could what we are seeing in metals happen in chemicals and polymers? Over the last few weeks, we have seen already high metals pricing spike even further, both because of production shortfalls and because of expectation of higher demand, especially in the renewables space, as conventional energy prices have spiked. We show a lithium example below, but note that after chaotic nickel trading last week and a halt to trading, the market has made some attempts to reopen this morning with renewed problems.

As noted in Exhibit 1 from today's daily report, the jump in oil prices has plunged the European polyethylene producers into the red and pushed Asian polyethylene producers further into the red. This will inevitably result in price increases as basic chemical and polymer producers will shut down at negative margins, and these price rises offer an opportunity for the US, Middle East, and select other producers.

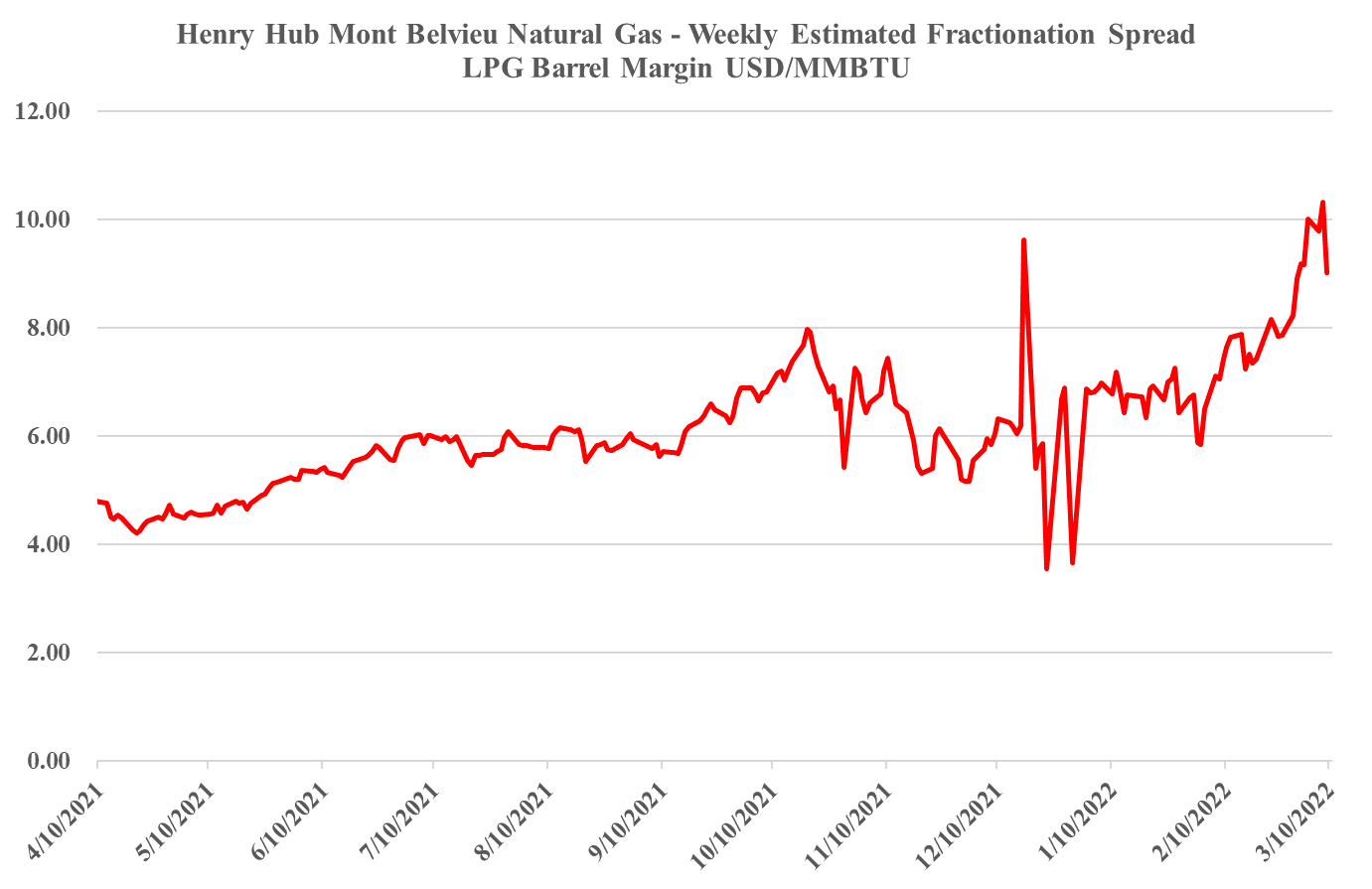

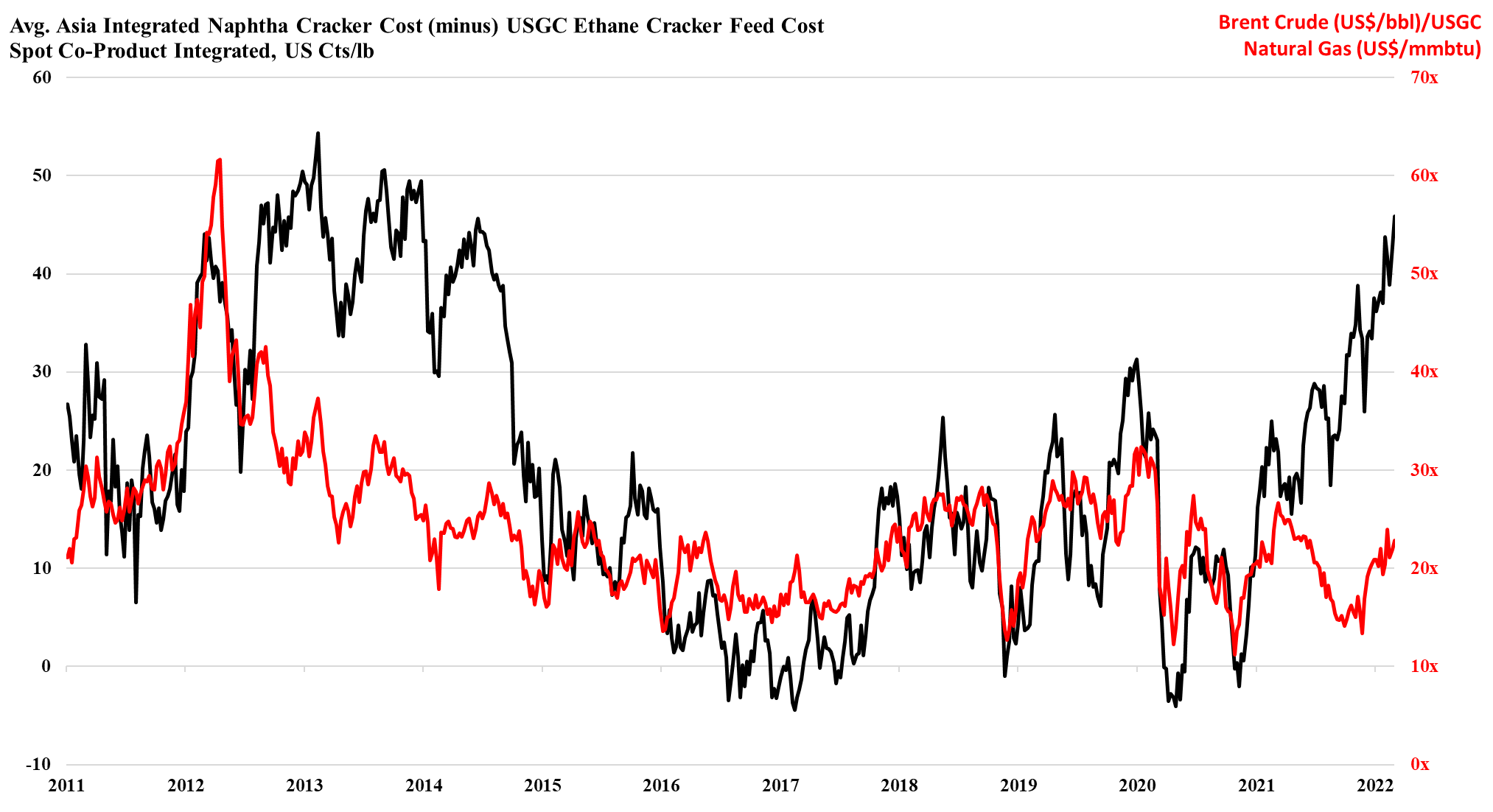

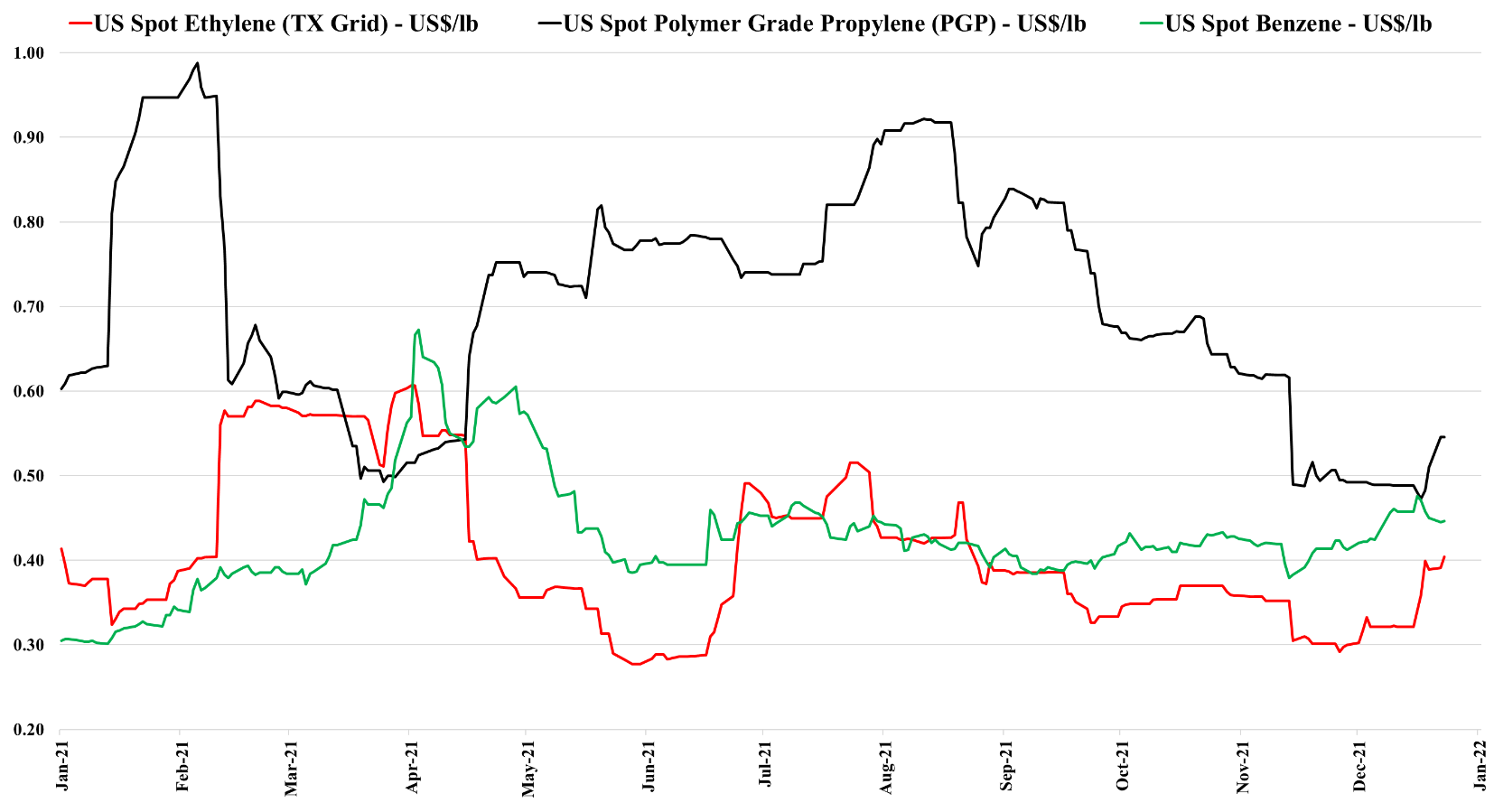

As the ratio of pricing between Brent crude and US natural gas rises, the US ethylene cost advantage is spiking, and as long as the US is producing enough natural gas to feed domestic demand and allow the LNG facilities to run at capacity, the advantage can remain. This gives the US a significant cost advantage and assuming that there is spare capacity the US industry can step up and support Europe if needed. However, it is not clear that there is much spare capacity, either in the production units or in the logistics to get the product to ports or across the Atlantic. There is a surplus of liquid and gas carriers today, but the container problems are global and the inflation and supply chain issues that we seem to be stuck with are likely to keep containers tied up in excess inventory that consumers will want to keep building as a cushion for a less certain supply outlook. The shipping issues are only part of the problem for Asia, as even with better opportunities to export, the region is seeing escalating production costs because of the movement in crude oil and naphtha pricing. We are in an unusual position where strong demand in the US is keeping domestic prices higher than in Asia, despite costs in the US that are low enough, especially for polyethylene to move material to Asia at costs well below the cost of manufacture in Asia. This dynamic can last for a lot longer in our view as long as oil prices remain elevated versus US natural gas. An abrupt turn will occur if US natural gas production falls below domestic demand and LNG demand – this would cause a spike in US natural gas prices. For more see today's daily report.

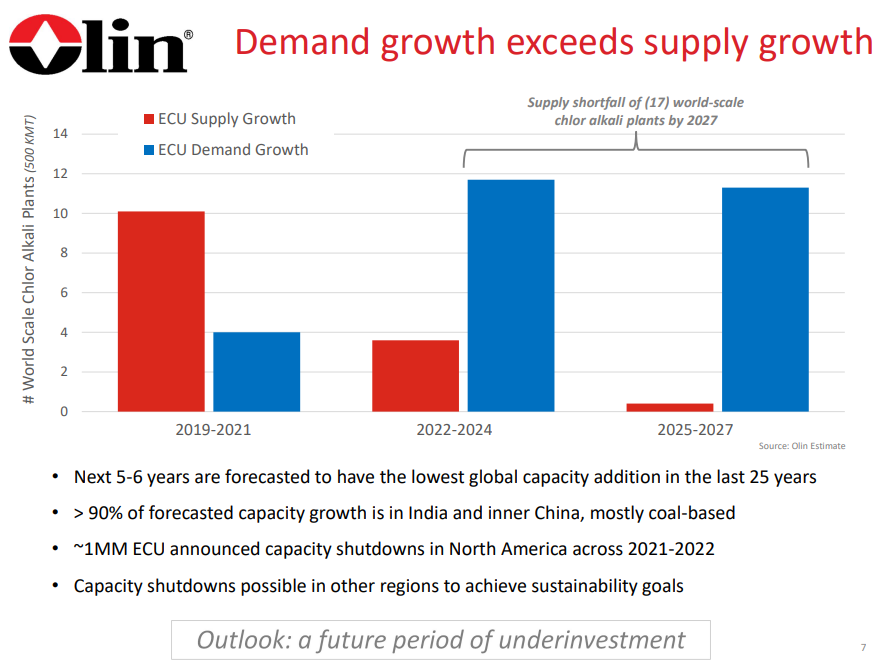

We are already seeing the impact of ESG-pressure related underinvestment in many commodities, and the picture that Olin paints around chlor-alkali is not dissimilar to some of the analyses that could be done around some metals today – especially those that are critically important to the EV, Solar, and Wind industries – this is a topic that we have covered at length. While chlor-alkali may be a pressing very near-term example of how underinvestment could impact chemicals, we suspect that the issue may be much broader, just not yet apparent in other sectors because of the wave of new investment from 2017 through 2022. The polyethylene equivalent chart to the one below would show more balanced supply/demand in the 22 – 24 period than for chlor-alkali but the same deficit thereafter. Many of the other base chemicals would look the same. This supports our expectation of an industry mega-cycle, possibly starting as early as 2023. Of course, there is time to add new capacity by 2025/26, but most companies are more focused today on how they comply with tighter environmental standards today than they are on their next expansion. Further hindering new expansion-driven capital investment decisions is the uncertainty around polymer demand (how much will be recycled, will there be more bans, will there be a substitution from other materials). Our view is that base polymer demand will continue to grow and that we will run short as a consequence of underinvestment. See our report titled - Waiting For The Big One – Is A Chemical Mega-Cycle Ahead?

We are seeing pockets of real demand strength in some areas of chemicals, such as building products, and this is allowing producers to push through price increases to reflect higher costs and most likely add some margin. In other areas where the fundamentals might not be quite as supportive, we are still seeing attempts to pass on higher costs. Sika has supported what we have heard from many over the last few weeks, which is that the building products chain remains tight, as demand is strong, capacity is running hard and logistic issues continue to cause problems in some cases from a raw materials perspective and in others from getting finished products to market. Where there is limited ability to increase supply, those selling into the building products space are likely to make more money as they should have strong pricing power – in the US chemical space, we would favor Westlake as a potential big winner from this trend, but Huntsman should also be on the list.

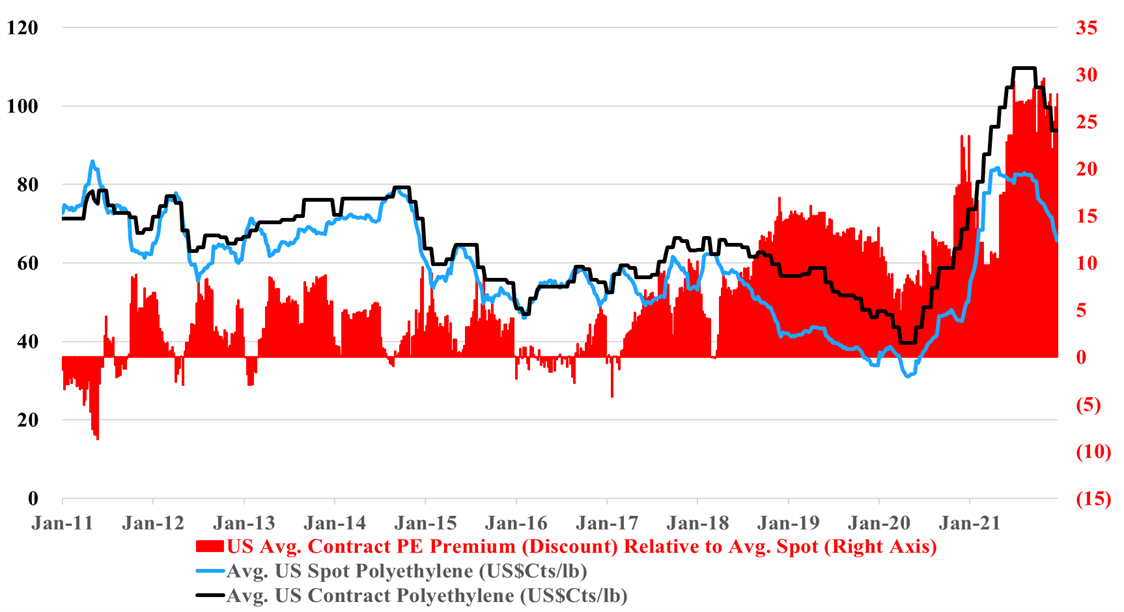

The negative momentum in US polymers prices is overwhelming all other factors in the eyes of public shareholders, with Dow and LyondellBasell share prices both down 6% since October 1st, underperforming the S&P500 by 16%. The data in our Daily Report and the exhibit below show that current industry profitability is very high and much higher than it was in 2019 when share prices were roughly where they are now. Our expectation is for profits to fall in 2022, but not to the levels seen in 2019 unless there is a significant increase in US natural gas and NGL pricing relative to crude oil (which is possible). But while these stocks look very attractive based on historic relationships to cash flow, we cannot ignore years of experience covering this sector which says that no one gets interested until the earnings revisions bottom out - so not yet, and likely not in 1H 2022. Complicating the story is the lack of clarity around what sort of EGS penalty is implied in current valuations and whether it could get worse as ESG funds grow, which they surely will in 2022. In our ESG and Climate report tomorrow we will look at some chemical stocks that could benefit from the rise in energy transition and infrastructure spending in 2022 and are less exposed to commodity polymer global oversupply.

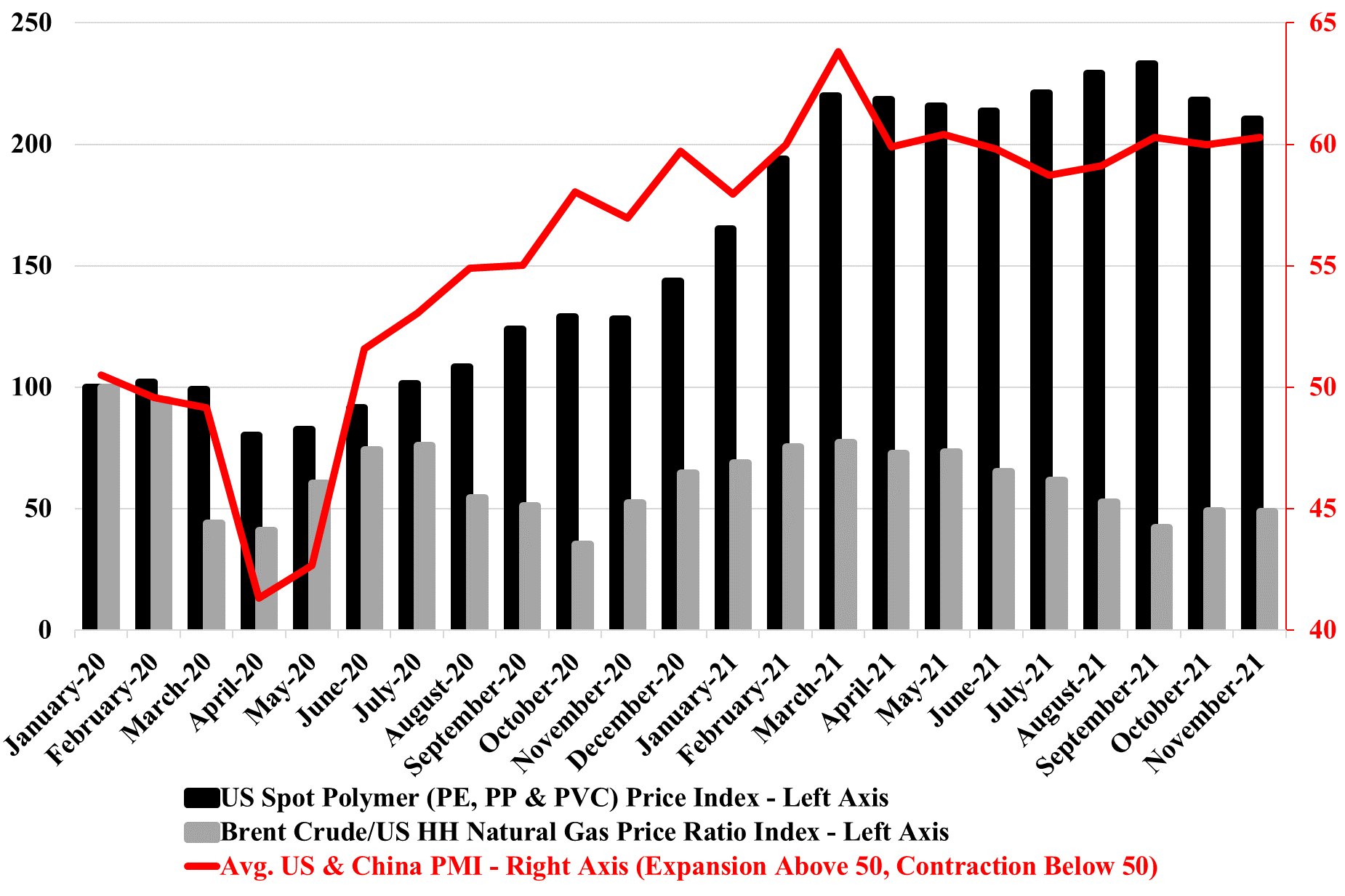

We have been asked a couple of times in the last week how US polymer (polyethylene in particular) pricing can remain so robust in a market where there is an inventory build going on. The PMI numbers are part of the answer. While we may be in the seasonally weaker part of the year, customers are still looking for more material than a year ago, and this makes the “we need a lower price” argument much harder, especially when the memory of 1H 2021 acute shortages is still fresh in the memory and when, more than likely, they are getting signals from their customers of a further step up in demand in 2022. We have done some traveling recently and the incremental demand for packaging polymers is very evident in the travel and leisure business, even if the number of travelers is still down. There is more packaging on airline and airport food and hotels are offering pre-packaged food for breakfast that would previously have not been individually packed. The reasons are obvious – safety and hygiene from the consumers' end and costs from the providers' end, as prepackaged food, can be bought in bulk and more cost-effectively and they likely have a longer shelf life.

Following on from the LyondellBasell commentary in today's daily report, we would make one further, but very important point. With its refinery (granted the company is exploring opportunities to exit) and its huge commodity polyethylene, polypropylene, and propylene oxide business, any attempt to pursue a “specialty” strategy that encompasses the whole portfolio will be seen (crudely) as trying to put some lipstick on a pig! This rarely works in the chemical sector and the real transformation stories involve wholesale portfolio shifts, many of which have taken notable periods of time to develop. We still believe that the right path for LyondellBasell is to spin off the good piece – recycling, licensing, and compounding, or even better, find someone they can sell the business to through a Reverse Morris Trust. This strategy would likely allow the company to pay down (or shift) a significant amount of debt. The commodity business can then focus on the best strategy for a commodity polymer business in the face of energy transition, which might involve taking the business private or merging with another.

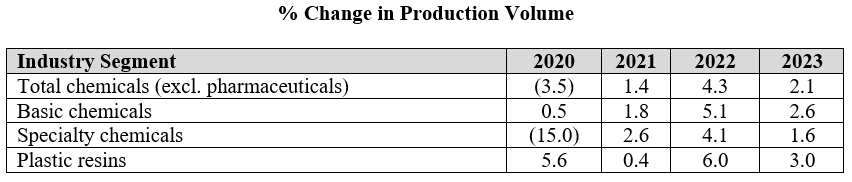

The ACC forecasts below leave us a little confused as the implication for specialty chemicals is that production declines in the US by an average of 2.0% per annum from 2019 to 2023. Given the demand that we are seeing for US manufacturing, as covered in our most recent Sunday Report, we would expect demand for all inputs to rise and it is unlikely that the gap would be filled by a swing in net imports. The lower demand from the Auto industry in 2020 and 2021 and broader manufacturing shutdowns in 2020 explains the 2020 and 2021 numbers to a degree, but it is not clear why there would not be a rebound as auto rates increase. We would also expect to see a stronger rebound in polymer production in 2022, assuming weather events are less impactful than in 2021, given substantial new capacity for polyethylene from ExxonMobil/SABIC, BayStar, and Shell.

The recent Dow guidance is worth some further comment as it is being heralded in the stock market as an earnings miss, or at least that is what is implied in the stock performance, even though the signals around margin squeezes in 4Q have been in place for weeks and have been covered extensively in our work. Some elements of modeling chemical company earnings are complex, but rising energy (and therefore feedstock) prices is not one of them. We have commented several times over the last couple of years about the lack of almost any effort being made by the sell-side to rethink estimates mid-quarter, choosing instead to take or interpret company guidance (generally in the first month of a quarter) and then wait until earnings are reported. This does a disservice to both the institutional investors and the chemical companies, as the investors quickly conclude that estimates are likely too high – simply looking broadly at what sectors get hurt by rising energy – but generally do not have a good measure of by how much earnings will be impacted, so they sit on the sidelines, expecting the surprise. That said, there are so many algorithms working today that the alternative of gradual negative revisions to a more reasonable target for the quarter is also likely to hurt stock performance.