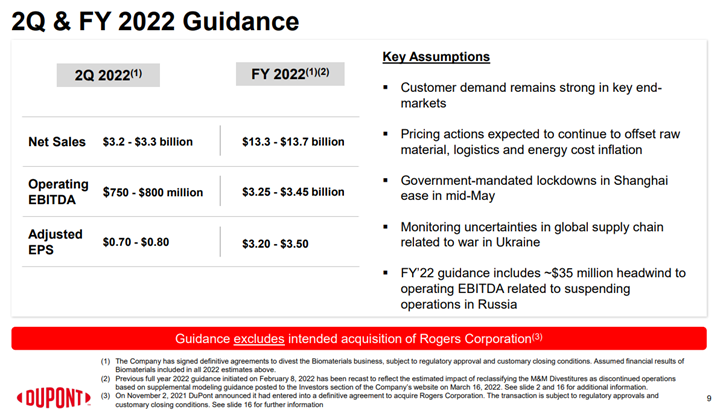

Like many of the European producers, DuPont has taken a risk in our view by holding guidance flat in the face of inflation, weakness in China, and a potential further economic slowdown in Europe and the US. We struggle with what an alternative approach should be for DuPont and others, given that it would be challenging to map out a credible downside scenario today. What we would note, however, is that when things turn negative for the materials industries they tend to fall quickly and sharply. For all of the base chemical and specialty chemical companies what might upset things for 2022 are largely outside of their control, and it is hard to second guess cutbacks in customer demand until they happen, especially in an environment where all are looking at volatile costs from energy and consumer spending uncertainty because of inflation. For more see today's daily report.

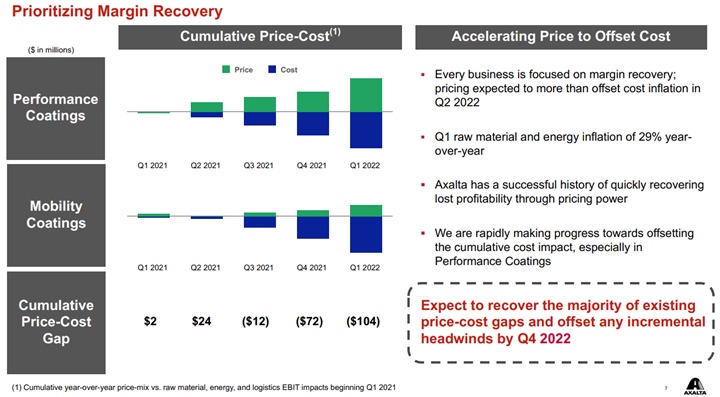

Axalta shows a helpful picture below of how pricing and costs are moving. All coatings producers are seeing the same cost inflation, some of it energy/hydrocarbon input related and some of it supply chain-related – either for inputs such as pigments or higher costs of getting products to markets. How pricing looks relative to costs is very customer dependent, as shown in the chart below. Auto OEM customers have long lead times on price adjustments and this is why Axalta is signaling the end of the year before prices will be aligned with costs. This of course assumes that costs do not rise again in 2H 2022 as they will also drive a lag in price increases and create a further gap as shown in the “Mobility” bar below. In the more consumer-facing coatings, it is easier to raise prices more quickly and Axalta and others have managed to keep pace with costs. We see the pricing versus costs issue as a much greater headwind for the specialty chemical companies than for the commodity companies and the industrial gas companies – the commodity chemical companies can raise prices more quickly and most industrial gas pricing is on a cost pass-through basis.

The linked China polyethylene headline highlights a possible risk for US producers, as we link much of what is happening in China to logistic challenges. China has high production costs in a high oil environment, which is driving some of the cutbacks, but a portion is likely driven by an inability to move product and a huge disincentive to build inventory at break-even or negative margins. If the current shipping challenges in China roll over more aggressively into the rest of the world and container and vessel availability fall again, the US may face more challenges exporting polymers. As warehouse space fills, especially on the Gulf Coast, we may see some need to cut back rates, even if all of the material in storage currently has an agreed home and an agreed price. The US can afford to build inventory, as production costs still remain attractive relative to international prices, but if the supply chain is full there could be nowhere to put more material. One of Union Pacific's issues highlighted last week was too much inventory in rail cars, snarling up the system.

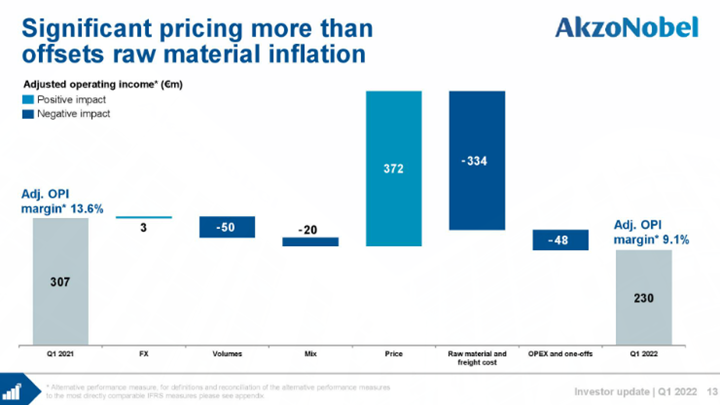

We have discussed in several recent reports the very mixed fortunes in the intermediate and specialty chemical sector related to whether companies have been able to move prices fast enough to cover costs. The two large blue bars in the AkzoNobel chart below show that Akzo was close, but did not make it. We expect other examples like this over the coming weeks but we also expect some companies to have done better – some of this depends on mix and contract terms, but a lot has to do with how early you acted on the rising cost trend and how aggressive you were willing to be with customers. Dow is another example of a company struggling to get pricing high enough to cover cost increases, although Dow and others have aggressive price increase announcements in the market for polyethylene for April and May that would make a significant difference to US margins if successful.

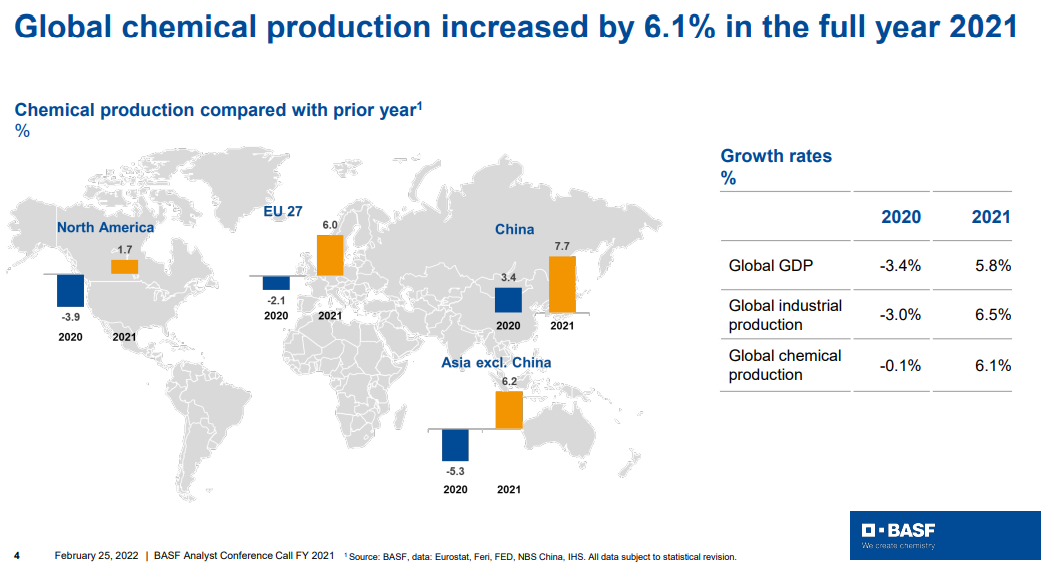

Fear of shortages is the one factor that is most supportive in terms of helping to push through pricing and the events in Europe and their associated impact on energy prices should be all the support that the chemical and polymer industry needs to push pricing through that will cover cost inflation. Buyers of raw materials and intermediate products will naturally look to buy a little more than they need in the near term, both to ensure that they get something ad to try to build a bigger inventory cushion. This will have the effect of pushing apparent demand higher, making the pricing initiatives easier. Few will push back on pricing if their primary concern is availability. Looking at the BASF results summarized in the chart below, demand is already very robust and this will lead to higher utilization rates and higher volumes for chemical producers as well as high pricing. The commodity producers are likely more interesting here as they can move prices much more quickly than the specialty companies who might see margins squeezed over the next couple of months. None of this is good for inflation. See more in today's daily report.

While it has been a long time coming, and it is unclear whether COVID hindered or helped, the DuPont materials exit is not a surprise and we noted after the IFF deal that we believed that Ed Breen was not done. During his time at Tyco, Mr. Breen showed a very clear ability to identify better owners for businesses that were lost in a conglomerate structure. We had always anticipated the same with DuPont and the business that is moving to Celanese is one we had expected to move and we had discussed previously. This should be a win for both companies as DuPont begins to look much more like a stable margin specialty chemical company with a portfolio that is becoming more ESG centric – see today's daily – while Celanese now has a large and comprehensive portfolio of polymers that are critical to the transport sector and should be able to drive both revenue and cost synergies if the company manages the integration well.

Akzo Nobel is somewhat unusual among the more specialty chemical (in this case paint) producers, as the company has managed to raise prices fast enough to offset costs and produced strong positive results for 4Q 2021. Not having auto OEM exposure will have helped Akzo and the company is well-positioned to manage pricing through its stores in many cases. It is a relatively safe environment to push up paint prices as all of the competitors have the same cost pressure and need to do the same, and demand remains strong – consumers are buying paint.

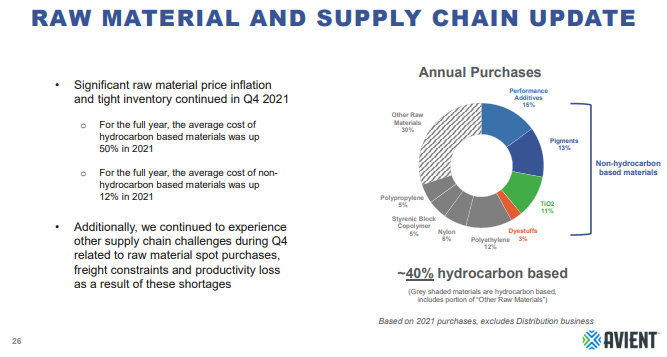

As Avient and the linked paint article remind us, there are sectors of the US chemical industry that rely on imported products – in these cases pigments, and the supply chain challenges and logistic delays have caused production problems in the US and price increases in 2021. The automotive segment of the paint industry has seen lower demand because of the auto OEM production slowdown, and pigment shortages and price spikes would likely have been worse if automakers had been running at full rates. There is no sense of impending relief in the logistic issues as we go through 4Q earnings reports and we could continue to see issues for a while. This should be good for US-based pigment suppliers, but while Chemours, Venator, and Tronox all have capacity in the US, they also have capacity outside the US which likely faces some supply chain challenges.

With the linked Ashland release, we see another example of a downstream chemical maker struggling with higher input costs and general logistic constraints, and an inability to push through pricing quickly enough to avoid a margin squeeze. The opaqueness that Ashland discusses concerning some of the planning metrics for the near-term is impacting forecasts and estimates for many more companies than just Ashland but given the costs and the supply chain challenges, all are encouraged to push through pricing aggressively, and this suggests that we are far from done with the materials inflationary pressures that we have discussed at length in prior reports and the higher costs of some of these specialty chemicals will start to impact customer margins through 2022. Almost all the earnings reports that we see discuss strong end-market demand and whether this is final customer pull-through or a need to address chain inventory or both, it should support further price initiatives. For more on our inflation views see Inflation (Especially Energy Costs) – Biggest 2022 Wildcard.

Following on from the core theme of today's daily report, demand could provide the lifeline that the US chemical industry needs to get through what looks like a potentially oversupplied 2022 – note the successful start-up of the ExxonMobil/SABIC facility in Texas, announced today. While we still think that the US market will be looser in 2022 than in 2021, barring any above-trend weather events, strong demand growth could offer some pricing protection for the industry – especially given the input inflationary pressures that we are seeing. If the customer base is looking for increases in deliveries, which we expect to be the case in 2022, it will be easier to defend pricing and gain pricing where costs are higher. Some of the momentum that we are seeing in the commodity stocks year to date is a function of a broader inflation trade, but some is likely in anticipation that 2022 will not be as bad as had been expected and on that basis, the sector looks particularly inexpensive – even today after the early year rally. It will be a little harder for the specialty and intermediate companies depending on how long they have to play a lagging catch-up game with costs. But if, and when, costs peak, they should see margin expansion as costs fall and will be able to keep some of the gains, especially if their demand is also growing.