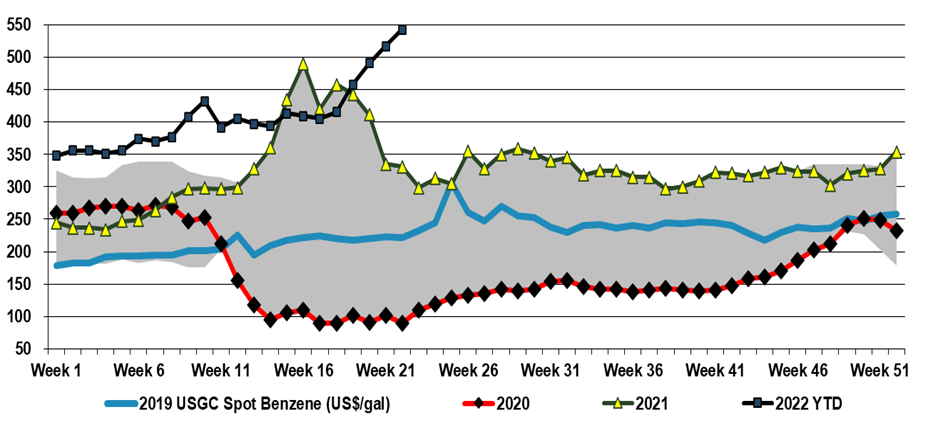

US benzene prices reflect both the net short market in the US but also the alternative value of reformate as a gasoline feed. While benzene is very limited in terms of how much can be left in fuel streams, its refinery-based feedstock, reformate, is a key component in gasoline – albeit low octane – prior to reforming and even during reforming the benzene conversion can be limited if the gasoline value is higher and volumes are constrained. In the US, as well as in many other parts of the world, we are facing gasoline shortages and today more than 13 US states have gasoline prices above $5 per gallon. While that may be shocking to Americans, the car ride from Heathrow yesterday was in a very popular make in the US that currently costs more than $200 to fill up in the UK! So benzene is getting squeezed – its feedstocks are more expensive and some of the alternatives to making benzene currently offer better netbacks. While we see all polymer costs rising in the US and elsewhere, this US benzene surge is not good for US polystyrene producers at a time when the industry is trying to justify polystyrene’s existence in a “circular” world, and it is also inflationary for the epoxy businesses, and other consumers of both styrene and phenol.

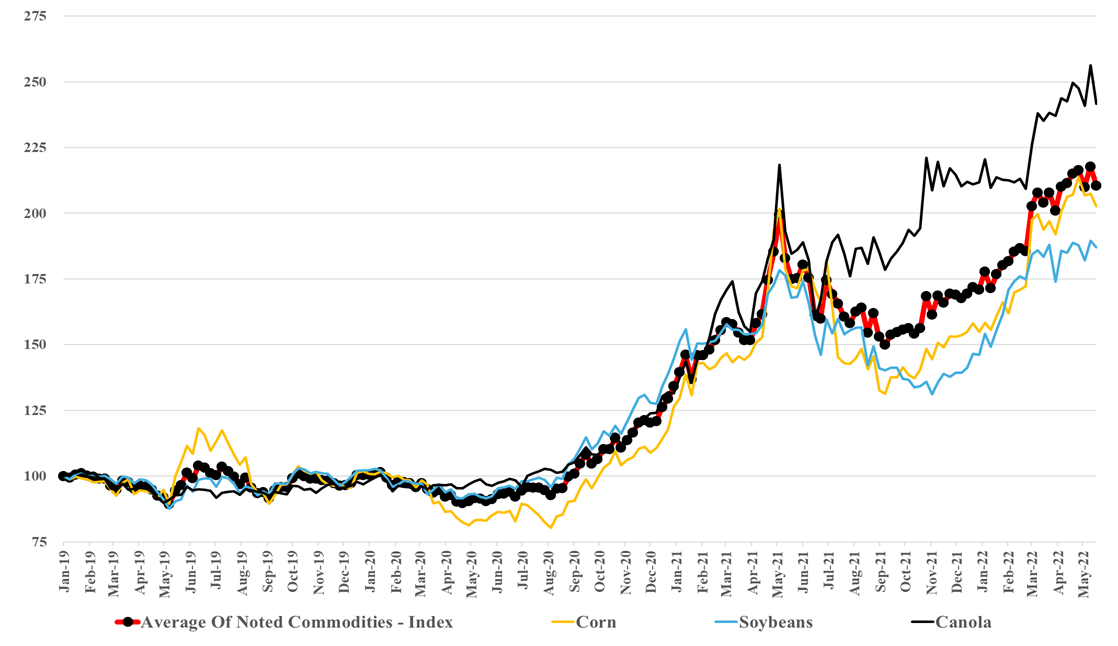

We have focused on agriculture this week with the ongoing announcements of new ammonia projects and the commodity crop prices and the overall index shown below are some of the key drivers of the activity in fertilizers but also are helping Ag equipment demand and we discuss the Deere results in today's daily report. We do not see how the trends in the chart below correct quickly and the profit through the farming, fertilizer, ag chemicals, and equipment chain should remain high in the US, at the expense of the consumer-facing high food prices (second chart below). We would need some coordinated medium-term policy to encourage moving more land in the US into agriculture, and this is especially necessary if we also intend to pursue bio-based fuels and materials. There has been much discussion around energy security over the last couple of months, but we think it is a much broader security discussion than just energy. Governments need to become much more accommodative around many aspects of production, food, energy, materials, etc. This accommodation can come with tighter emissions standards and emissions costs, but the primary objective should be to encourage more local production of many different things.

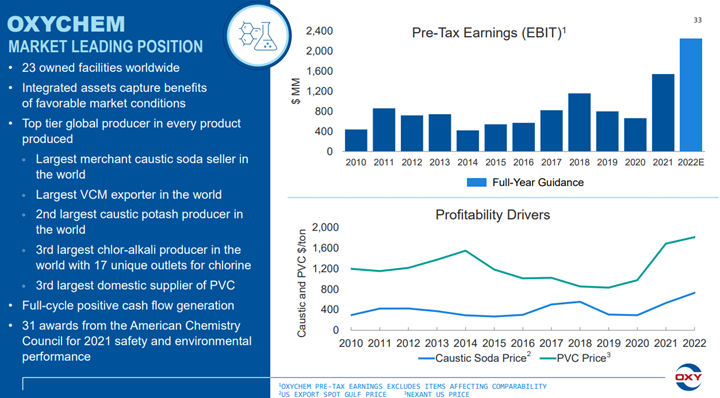

For those who are too young to remember, OxyChems’ 30-year comment is because the company owned ethylene capacity in the late 80s and early 90s and would have made more during that extreme ethylene peak. This is likely the most money that the stand-alone vinyls business has made. The strength in the PVC could see some reversal if the inflation pressure remains high and housing-related spending slows, but the strength in the caustic market could persist, regardless of economic growth because of structural shortages and the challenges with imports.

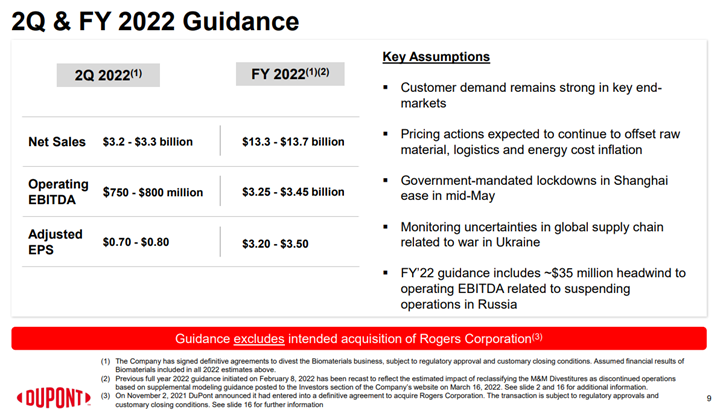

Like many of the European producers, DuPont has taken a risk in our view by holding guidance flat in the face of inflation, weakness in China, and a potential further economic slowdown in Europe and the US. We struggle with what an alternative approach should be for DuPont and others, given that it would be challenging to map out a credible downside scenario today. What we would note, however, is that when things turn negative for the materials industries they tend to fall quickly and sharply. For all of the base chemical and specialty chemical companies what might upset things for 2022 are largely outside of their control, and it is hard to second guess cutbacks in customer demand until they happen, especially in an environment where all are looking at volatile costs from energy and consumer spending uncertainty because of inflation. For more see today's daily report.

We see BASF taking a major risk by reaffirming its 2022 outlook today, as the uncertainty factors, especially in Europe, are rising. This week’s inflation and economic growth data in Europe, suggest an economy that is lowing quickly and the confidence levels in Europe are much lower, as we have discussed already this week. BASF and others will likely continue to push prices, but if consumer spending continues to slow, volumes will disappoint and at some point, there will be pushback on both volumes and pricing. Separately, as we mentioned above, we could see another leg up in energy prices as we approach next winter in Europe, especially if there is no resolution to the Ukraine conflict, which seems likely.

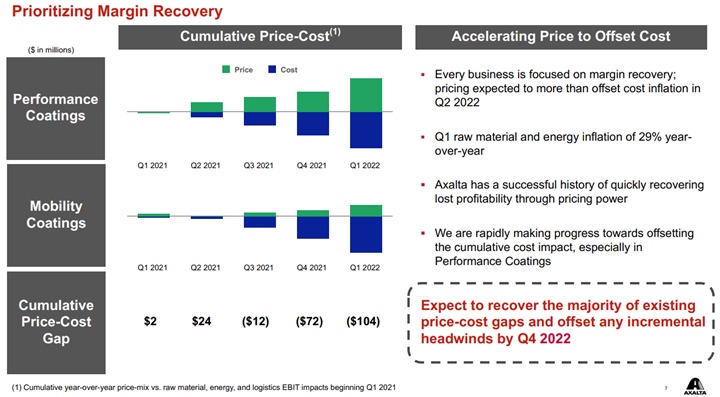

Axalta shows a helpful picture below of how pricing and costs are moving. All coatings producers are seeing the same cost inflation, some of it energy/hydrocarbon input related and some of it supply chain-related – either for inputs such as pigments or higher costs of getting products to markets. How pricing looks relative to costs is very customer dependent, as shown in the chart below. Auto OEM customers have long lead times on price adjustments and this is why Axalta is signaling the end of the year before prices will be aligned with costs. This of course assumes that costs do not rise again in 2H 2022 as they will also drive a lag in price increases and create a further gap as shown in the “Mobility” bar below. In the more consumer-facing coatings, it is easier to raise prices more quickly and Axalta and others have managed to keep pace with costs. We see the pricing versus costs issue as a much greater headwind for the specialty chemical companies than for the commodity companies and the industrial gas companies – the commodity chemical companies can raise prices more quickly and most industrial gas pricing is on a cost pass-through basis.

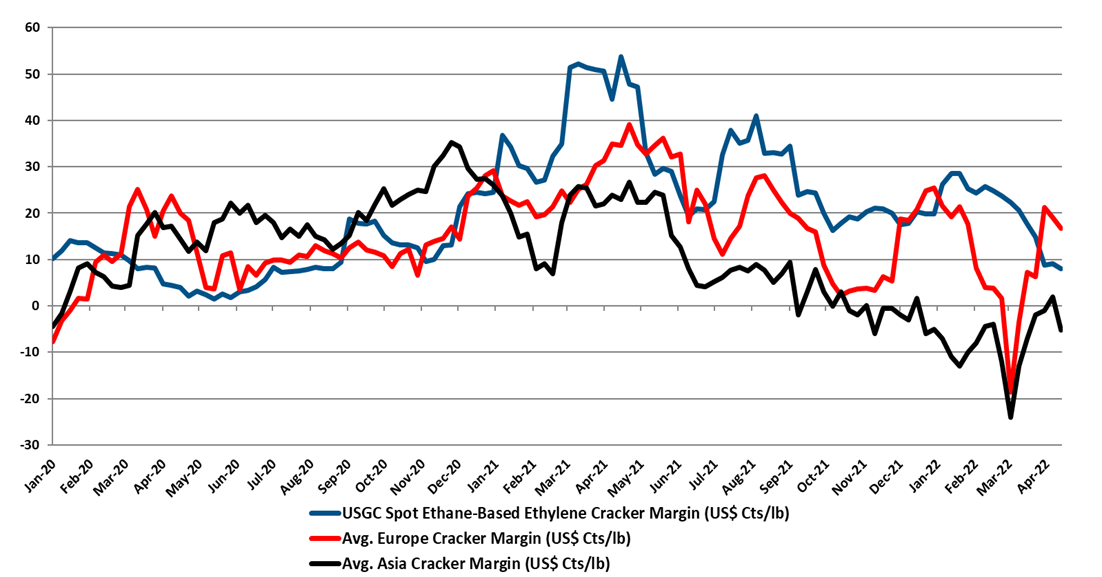

We note the polyethylene price nominations in the US, timed by some to coincide with earnings releases this week and next, and would remind clients that there is always price momentum in commodities, one way or another. In our view, the price increase moves aim to maintain directional momentum (upwards) while giving the polymer producers some cover should natural gas prices spike further. US ethane prices are now tracking natural gas more closely and have moved up meaningfully over the last few weeks, and US ethane-based ethylene margins have fallen around 80% since the start of the year, with at least half of that coming from cost increases. All polyethylene producers are integrated back to ethylene, and the price nominations will be attempts to recoup some of the cost increases. This is against a backdrop of still very strong polyethylene margins in the US, which although way off their 2021 highs remain much higher than in 2019 and 2020 and the longer-term average. This is covered in our Weekly Catalyst report each Monday. Ethylene margins are summarized in exhibit below and the chart shows the impact of higher costs in the US and falling spot ethylene prices as the US now has more surplus ethylene capacity and is looking for export homes for ethylene and easy to ship derivatives. As we have noted before, the jump in margins in Europe and Asia is because of extreme volatility in naphtha markets over the last couple of weeks. We would expect margins to be lower next week based on naphtha moves this week.

As we have been suggesting for some time, there are pockets of real strength in chemicals; identifying them is the hard part. It is not enough to have pricing strength in a market where raw material prices are volatile daily and we have seen plenty of examples of companies with very strong end demand dynamics missing earnings because of a cost squeeze. We continue to highlight the competitive strength in the US in basic chemicals because of the decoupled and relatively low natural gas price and this is likely a large piece of the Dow earnings strength – strong polyethylene demand against a backdrop of relatively stable and lower costs. While polypropylene (Braskem) remains extremely profitable in the US, it has seen more sequential weakness than polyethylene – as we show in Exhibit 1 of today's daily report. That said, both polyethylene and polypropylene margins in the US are significantly higher than was likely expected this year and certainly what has been reflected in stock valuations, even with the commodity chemicals rally. Dow is also seeing the benefit of a very strong silicones market – something that was covered in detail in Wacker’s release earlier this month.

With the rapid jump in international natural gas and oil prices, we would see very concerted efforts to raise basic chemicals and polymer prices in Europe and Asia and will have a positive knock-on effect for the US. In our weekly catalyst report on Monday, we showed that ethylene producers outside the US were all losing money, especially in Europe and Asia. Some European demand will already be lower, because of curtailed product exports to Russia and Ukraine, but producers will want to cover costs at a very minimum and consequently, will be trying to match price increases with cost increases and if possible do a bit better than that. All of this will create a greater margin umbrella for the US, and US exporters selling directly into international markets will see export margins step up and may see incremental opportunities to export more, assuming that the freight rates are not too onerous for incremental containers.

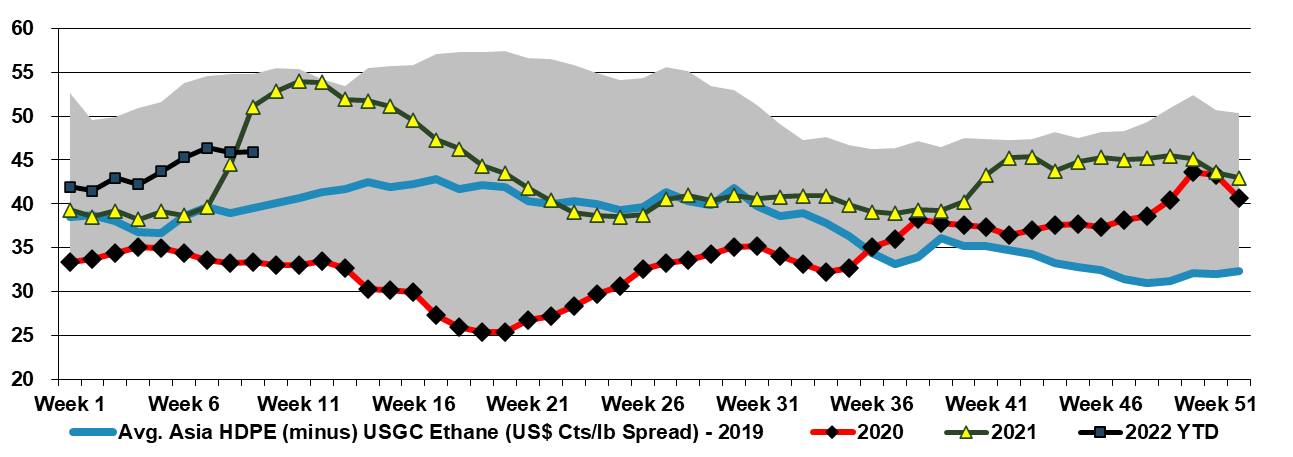

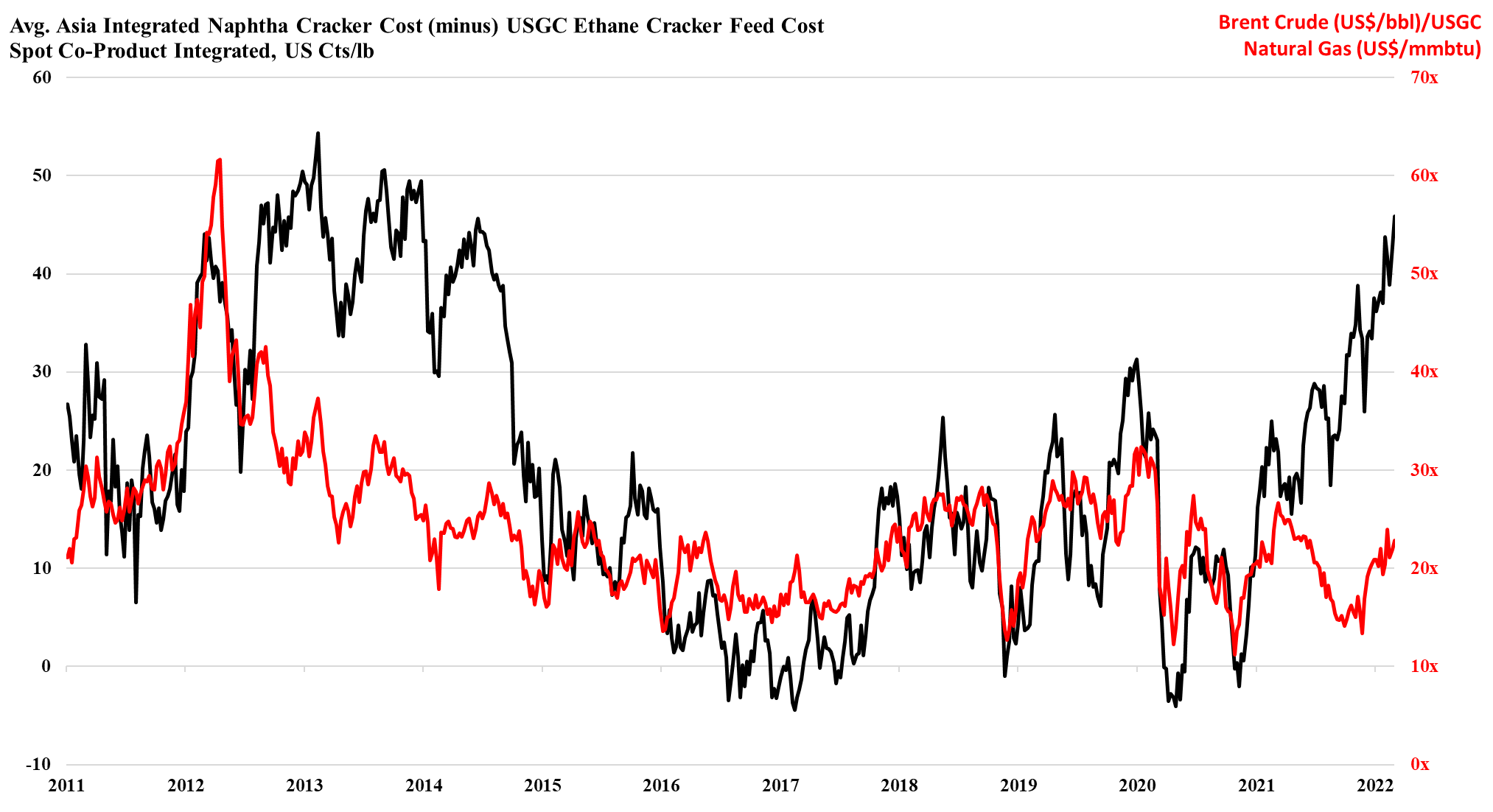

As the ratio of pricing between Brent crude and US natural gas rises, the US ethylene cost advantage is spiking, and as long as the US is producing enough natural gas to feed domestic demand and allow the LNG facilities to run at capacity, the advantage can remain. This gives the US a significant cost advantage and assuming that there is spare capacity the US industry can step up and support Europe if needed. However, it is not clear that there is much spare capacity, either in the production units or in the logistics to get the product to ports or across the Atlantic. There is a surplus of liquid and gas carriers today, but the container problems are global and the inflation and supply chain issues that we seem to be stuck with are likely to keep containers tied up in excess inventory that consumers will want to keep building as a cushion for a less certain supply outlook. The shipping issues are only part of the problem for Asia, as even with better opportunities to export, the region is seeing escalating production costs because of the movement in crude oil and naphtha pricing. We are in an unusual position where strong demand in the US is keeping domestic prices higher than in Asia, despite costs in the US that are low enough, especially for polyethylene to move material to Asia at costs well below the cost of manufacture in Asia. This dynamic can last for a lot longer in our view as long as oil prices remain elevated versus US natural gas. An abrupt turn will occur if US natural gas production falls below domestic demand and LNG demand – this would cause a spike in US natural gas prices. For more see today's daily report.